The Instruction Is Not the Payment

When Customer A initiates a Rs.5,00,000 transfer from SBI to HDFC Bank, the money does not move at that moment. An instruction moves. What follows is a structured, sequenced process involving message exchange, obligation calculation, and accounting entries that end in one moment: finality. That moment is when the transfer is irrevocable, counterparty risk is eliminated, and the payment is legally complete.

This gap between instruction and finality is where clearing and settlement live. It is also where most misunderstandings in payments originate. Junior analysts assume the payment is done when the instruction is sent. Experienced practitioners sometimes conflate clearing with settlement. And in cross-border payments where there is no central clearing infrastructure between the banks, the same process happens inside the banks themselves , invisible to most participants, and frequently misunderstood even by the people building those systems.

Every settlement method in this series answers the same question differently: how do we get from instruction to finality, at what speed, at what cost, and with what risk control? DNS, RTGS, Instant Payments, Correspondent Banking, Fintech ; each is a design choice with tradeoffs. Before comparing methods, we need to own the infrastructure.

The Infrastructure: Who Sits Where and What Each Does

Set up the players first. Once you understand who each participant is and what their function is, the entire process becomes logical. This is the domestic clearing and settlement infrastructure for India.

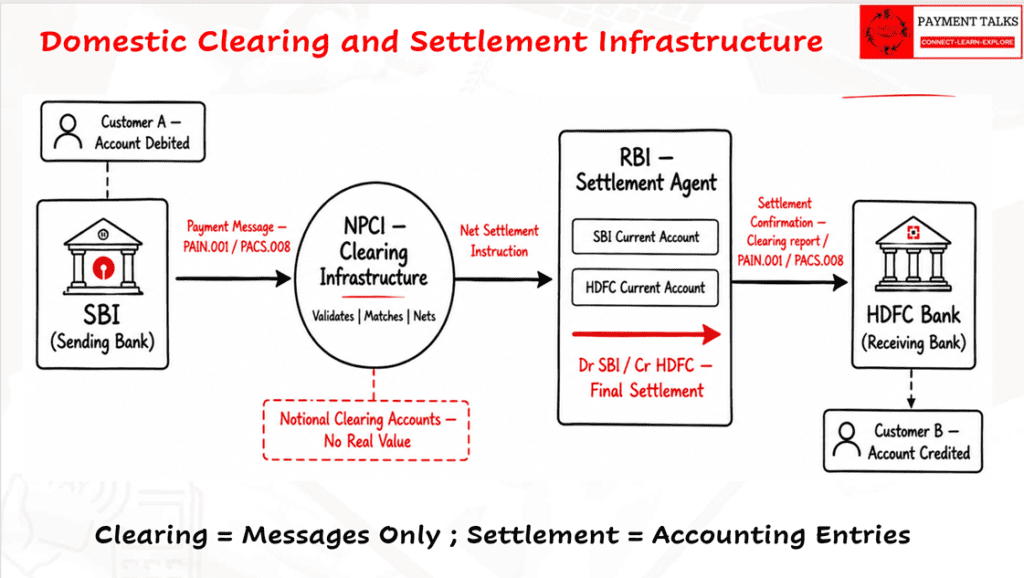

Figure 1: Four-participant domestic infrastructure. SBI submits payment messages to NPCI (clearing). NPCI validates, nets, and passes settlement instructions to RBI. RBI posts final entries. HDFC credits Customer B on RBI confirmation only.

SBI — Debtor Bank (Sending Bank)

SBI is the bank Customer A holds an account at. SBI initiates the payment by ring-fencing Customer A’s funds internally and submitting a payment message to NPCI. SBI holds a current account at RBI , the settlement account, which is debited when settlement occurs.

NPCI — Clearing Infrastructure

NPCI operates as the clearing house for domestic retail payments in India. It receives payment messages from all participating banks, validates them, matches obligations, and calculates net positions. NPCI tracks these obligations in notional clearing accounts or obligation-tracking ledgers, not real value accounts. No money resides at NPCI. NPCI passes net settlement instructions to RBI.

RBI — Settlement Agent (Central Bank)

RBI is where settlement happens. Every bank in the clearing system holds a current account at RBI. When RBI debits SBI’s current account and credits HDFC’s current account and that is settlement. That is finality. Nothing before that moment constitutes a final payment.

HDFC Bank — Creditor Bank (Receiving Bank)

HDFC receives settlement confirmation from RBI and credits Customer B’s account. The key sequencing point: HDFC credits Customer B after RBI confirms settlement, not after receiving NPCI’s clearing message. A bank that credits customers before RBI’s confirmation carries settlement risk on its own books. (Some banks do this based on customer’s relationship)

Customer A and Customer B

The ultimate sender and receiver. Neither sees the infrastructure. Customer A sees an account debit. Customer B sees an account credit. The infrastructure exists to make that invisible process reliable, final, and risk-controlled.

| Series Note: This is the domestic India infrastructure. In cross-border payments, this structure changes fundamentally. There may be no NPCI equivalent between two banks. That is where the complexity begins and it is exactly what later Parts address. |

What Is Clearing? Message Exchange, Obligation Tracking, No Money Moves

| Core Definition: Clearing is the process in which payment messages are exchanged, obligations are matched, validated, and netted. No accounting entries happen in clearing. No real money moves. |

This is the single most important definition in this series. Clearing is a message process. The clearing house receives payment instructions, validates them, and calculates what each bank owes to every other bank. Three functions define it:

Matching

The clearing house verifies both sides of the obligation are aligned. SBI’s instruction to pay Rs.5,00,000 to HDFC is matched against a valid HDFC receiving participant entry. No payment advances without a valid match.

Validation

The message is checked for format compliance, AML and sanctions screening, and routing accuracy. ISO 20022 messages (PACS.008) and SWIFT messages (MT103) are referenced at this stage and these are the message formats in play. Validation failure returns a rejection notice to the sending bank (PACS.002 / MT199 / Ack-Nack).

Netting

If multiple payments flow between the same banks within a clearing cycle, the clearing house calculates net positions. If SBI sends Rs.5,00,000 to HDFC and HDFC sends Rs.2,00,000 to SBI in the same cycle, the net settlement obligation is Rs.3,00,000 and not Rs.7,00,000 gross. This netting mechanic is the core of Deferred Net Settlement, covered in depth in Part 2.

Notional Clearing Accounts — Obligation Tracking, Not Value Storage

The clearing house maintains notional clearing accounts to track these obligations. These are not bank accounts where value resides. They are obligation-tracking ledgers. NPCI knows, at any point in the clearing cycle, that SBI has a net payable of Rs.X and HDFC has a net receivable of Rs.X. That information is precise and binding. But no value has transferred. NPCI passes the net obligation as a settlement instruction to RBI.

| Practitioner Point: “In clearing” does not mean “payment done.” It means the message has been submitted, obligation is being calculated, and settlement has not yet occurred. The risk between clearing and settlement sits entirely with the participating banks. |

What Is Settlement? Accounting Entries, Value Movement, Finality Achieved

| Core Definition: Settlement is the process where accounting entries are posted, value moves, and finality is achieved. |

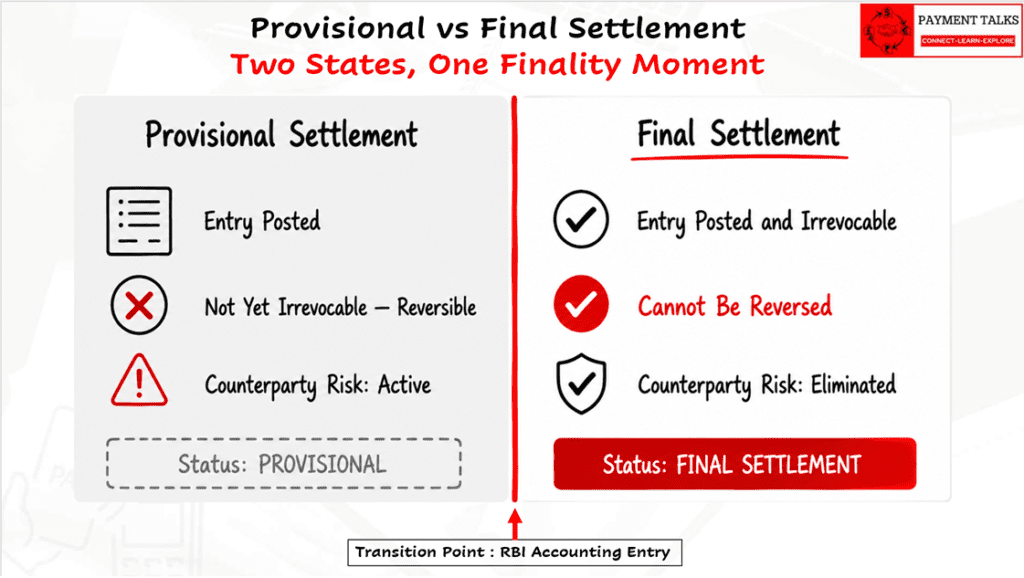

Where clearing is about messages, settlement is about accounting. This is the moment the obligation becomes irrevocable. Settlement operates in two states:

Provisional Settlement

An accounting entry has been recorded but is not yet final. It is reversible. The value appears to have moved but counterparty risk has not been eliminated. Some systems — particularly in correspondent banking — operate in provisional states for hours or days. A bank that treats provisional settlement as final carries unacknowledged settlement risk. This distinction matters enormously in operational risk management.

Final Settlement

The accounting entry is irrevocable and unconditional. No party can reverse it. Counterparty risk is eliminated. This is finality. In India’s domestic context, finality occurs when RBI posts the accounting entries. Not when the instruction is sent. Not when NPCI processes the message. At RBI.

Figure 2: Left — provisional state: entry posted, reversible, counterparty risk active. Right — final state: entry irrevocable, counterparty risk eliminated. Transition arrow marks the finality moment at RBI settlement.

| Finality Defined: The moment at which a transfer of funds becomes irrevocable and unconditional — counterparty risk is eliminated, and the payment is legally and operationally complete. |

The Complete Transaction Journey: Rs.5,00,000 from SBI to HDFC

Trace a single payment from instruction to finality. Every participant, every accounting entry, every message end to end. The T-accounts are where the difference between clearing and settlement becomes unmistakable.

Participants

| Participant | Role | Detail |

| Customer A | Sender | Account holder at SBI, Mumbai |

| SBI | Debtor Agent — Sending Bank | Initiates payment; holds current account at RBI; maintains SBI Clearing Nostro for internal clearing postings |

| NPCI | Clearing Infrastructure | Validates, matches, nets; passes net settlement instruction to RBI; issues Clearing Reconciliation Report to banks |

| RBI | Settlement Agent — Central Bank | Posts final accounting entries — debits SBI current account, credits HDFC current account; sends end-of-day net position statement |

| HDFC Bank | Creditor Agent — Receiving Bank | Receives PACS.008 from NPCI during clearing; receives RBI net position statement post-settlement; reconciles via NPCI Clearing Recon Report; credits Customer B. |

| Customer B | Receiver | Account holder at HDFC, Delhi |

| Amount / Currency | Payment Value | Rs.5,00,000 | INR | Domestic |

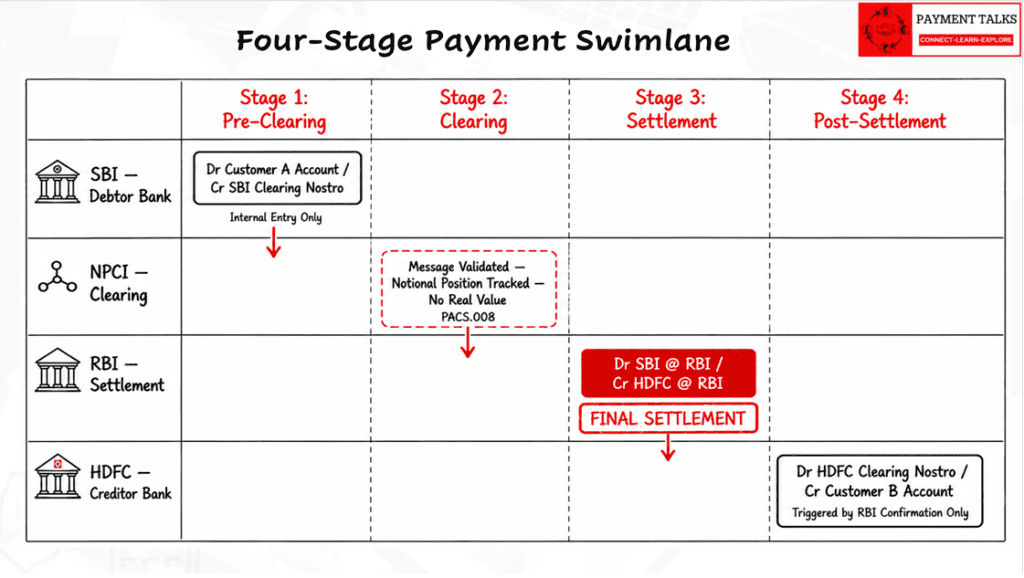

Figure 3: Swimlane diagram — pre-clearing (SBI internal), clearing (NPCI message processing and notional tracking), settlement (RBI accounting entries), post-settlement (HDFC internal credit). Finality marked at RBI entry.

Stage 1 — Pre-Clearing: SBI Internal Accounting

Customer A instructs SBI to transfer Rs.5,00,000. Before SBI sends any message to NPCI, it ring-fences the funds internally by debiting Customer A’s account and crediting its own SBI Clearing Nostro account. No money has left SBI at this point.

| SBI | Pre-Clearing — Internal | INR | ||

| Account / Description | Debit (Dr) | Credit (Cr) |

| Customer A Current Account | Rs.5,00,000 | — |

| SBI Clearing Nostro | — | Rs.5,00,000 |

| Note: SBI debits Customer A immediately , funds are ring-fenced internally. SBI Clearing Nostro holds the obligation until RBI settles. SBI then generates PACS.008 and submits to NPCI. This is an internal bank entry only, no money has left SBI. | ||

Stage 2 — Clearing: NPCI Message Processing and Obligation Tracking

NPCI receives SBI’s PACS.008. What follows is a message process, not an accounting process. NPCI validates, matches, appends a Clearing System Reference ID (CSID), and forwards the same PACS.008 to HDFC. NPCI also tracks the obligation in its notional clearing accounts.

NPCI Forwards PACS.008 to HDFC (Real-Time, During Clearing)

NPCI takes the original PACS.008 received from SBI, appends the Clearing System Reference ID, and forwards it to HDFC. This is not a new message , it is the same PACS.008 with NPCI’s reference added. This happens in real time during the clearing process.

| NPCI | Clearing — Notional Obligation Tracking Only | INR — No Real Value Transfer | ||

| Account / Description | Debit (Dr) | Credit (Cr) |

| NOTIONAL TRACKING ONLY — No real accounting entries. No value transfer. | ||

| SBI Net Obligation (Payable Position) | Rs.5,00,000 (notional) | — |

| HDFC Net Entitlement (Receivable Position) | — | Rs.5,00,000 (notional) |

| Note: These are obligation-tracking positions only and not real value accounts. If multiple payments flow between SBI and HDFC in the same clearing cycle, NPCI nets them before passing the instruction to RBI. PACS.002 acknowledgment sent to SBI. Net settlement instruction forwarded to RBI at end of cycle. | ||

Note: In rare cases where HDFC has a high-trust relationship with Customer B, it may credit the account on PACS.008 receipt carrying the settlement risk itself until RBI confirms.

Stage 3 — Settlement: RBI Accounting Entries — Money Moves, Finality Achieved

At end of the clearing cycle, NPCI passes the net settlement instruction to RBI. RBI posts the actual accounting entries. This is the only moment that constitutes settlement , the only moment finality is achieved.

| RBI — Settlement Agent | Settlement | INR | ||

| Account / Description | Debit (Dr) | Credit (Cr) |

| SBI Current Account at RBI | Rs.5,00,000 | — |

| HDFC Current Account at RBI | — | Rs.5,00,000 |

| [ FINAL SETTLEMENT ] | Irrevocable | Unconditional |

| Note: At this moment and only at this moment, the money has moved. SBI’s account at RBI is irrevocably debited. HDFC’s account at RBI is irrevocably credited. This cannot be reversed. Finality is achieved. RBI then sends its end-of-day Net Position Statement to both SBI and HDFC, confirming the net amounts posted. This confirms money movement at the gross/net level but is not the primary reconciliation tool for individual payments. | ||

Stage 4 — Post-Settlement: HDFC Internal Accounting and Reconciliation

After RBI settlement, HDFC reconciles its position using the NPCI Clearing Reconciliation Report , the primary instrument for payment-level reconciliation. The RBI Net Position Statement confirms money movement. The Clearing Recon Report confirms which individual payments were included.

| HDFC | Post-Settlement — Internal | INR | ||

| Account / Description | Debit (Dr) | Credit (Cr) |

| HDFC Clearing Nostro | Rs.5,00,000 | — |

| Customer B Account | — | Rs.5,00,000 |

| Note: HDFC credits Customer B after reconciling against the NPCI Clearing Reconciliation Report, which confirms each individual payment that settled in the cycle. The RBI Net Position Statement confirms the total net debit/credit to HDFC’s RBI current account. Both are used but the Clearing Recon Report is the payment-level source of truth for back-office reconciliation. | ||

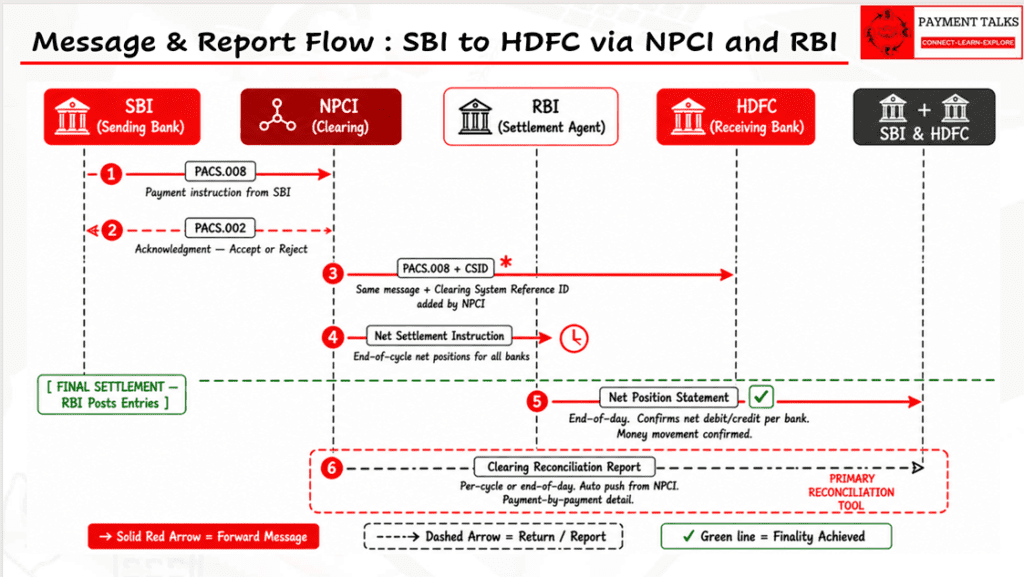

Message and Report Flow — Complete Sequence

Every message and report in the clearing and settlement process, from SBI’s instruction to HDFC’s reconciliation.

Figure 5: Swimlane diagram showing six numbered steps across five participants — SBI, NPCI, RBI, HDFC, and joint SBI-HDFC. Steps 1–4 cover clearing: PACS.008 from SBI to NPCI, PACS.002 acknowledgment back to SBI, same PACS.008 with CSID forwarded to HDFC, and net settlement instruction from NPCI to RBI. Green finality line marks the moment RBI posts accounting entries. Steps 5–6 cover post-settlement: RBI’s end-of-day net position statement confirming money movement, and NPCI’s Clearing Reconciliation Report — the primary instrument banks use to reconcile individual payments against their Clearing Nostro accounts.

| From | To | Message / Report | What It Does |

| SBI | → NPCI | PACS.008 | Payment instruction from SBI. Contains full payment details. |

| NPCI | → SBI | PACS.002 | Acknowledgment — acceptance or rejection of the payment instruction. |

| NPCI | → HDFC | PACS.008 + CSID | Same PACS.008 received from SBI, forwarded to HDFC with Clearing System Reference ID (CSID) appended by NPCI. Not a new message — same message with NPCI reference added. |

| NPCI | → RBI | Net Settlement Instruction | End-of-batch/cycle net positions for all banks. Triggers RBI accounting entries. |

| RBI | → SBI + HDFC | Net Position Statement | End-of-day statement confirming net debit/credit amounts posted to each bank’s RBI current account. Confirms money movement at gross level. |

| NPCI | → SBI + HDFC | Clearing Reconciliation Report | Per-cycle or end-of-day report (per NPCI–bank agreement). Automated push from NPCI. Contains individual payment details — the primary instrument banks use to reconcile entries in their Clearing Nostro accounts and confirm which payments settled in each cycle. |

Key Distinction: RBI’s Net Position Statement confirms the money movement (net amounts settled per bank). NPCI’s Clearing Reconciliation Report confirms the individual payments that comprised that net position , the payment-level source of truth for back-office reconciliation. Banks use both: RBI statement for cash/liquidity reconciliation, NPCI Clearing Recon Report for payment-by-payment reconciliation against their Clearing Nostro accounts.

Complete T-Account Map — All Participants, All Stages

End-to-end accounting journey.

| Stage | Participant | Debit (Dr) | Credit (Cr) | Status |

| Pre-Clearing | Customer A (at SBI) | Rs.5,00,000 | — | Internal — SBI only |

| Pre-Clearing | SBI Clearing Nostro | — | Rs.5,00,000 | Internal — SBI only |

| Clearing | NPCI Notional A/c — SBI Obligation | Rs.5,00,000 (notional) | — | No real value — obligation tracking |

| Clearing | NPCI Notional A/c — HDFC Entitlement | — | Rs.5,00,000 (notional) | No real value — obligation tracking |

| Settlement | SBI Current A/c @ RBI | Rs.5,00,000 | — | FINAL SETTLEMENT |

| Settlement | HDFC Current A/c @ RBI | — | Rs.5,00,000 | FINAL SETTLEMENT |

| Post-Settlement | HDFC Clearing Nostro (if not credited earlier) | Rs.5,00,000 | — | Internal — HDFC only |

| Post-Settlement | Customer B (if not credited earlier) | — | Rs.5,00,000 | Internal — HDFC only |

Finality Moment: When RBI debits SBI’s current account and credits HDFC’s current account and that is the moment the payment is irrevocable, counterparty risk is eliminated, and the transfer is legally complete. Not when Customer A sends the instruction. Not when NPCI processes the message. Not when HDFC receives the PACS.008. At RBI and nowhere earlier.

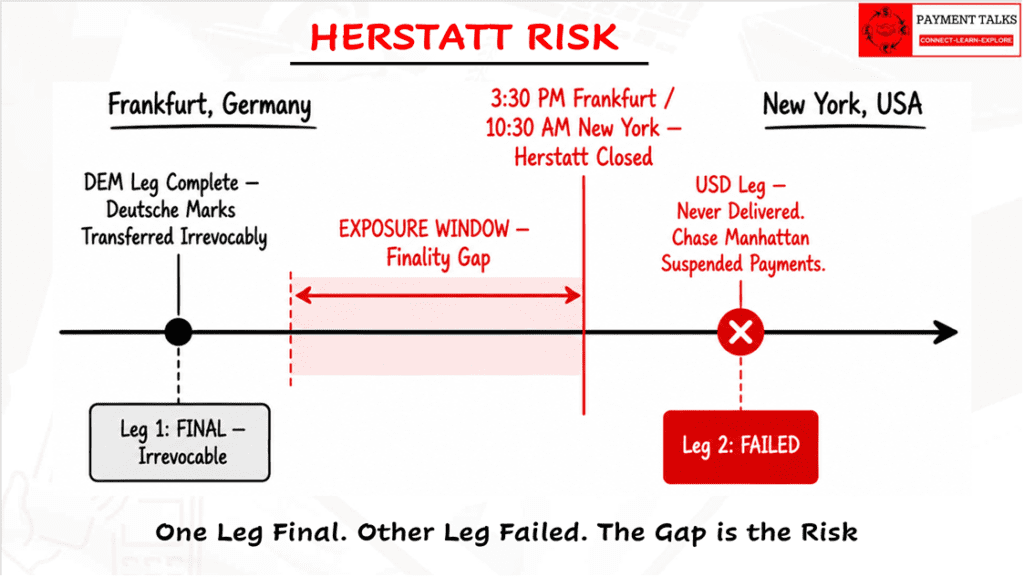

The Herstatt Collapse: Why Finality Timing Is Non-Negotiable

On 26 June 1974, German regulators closed Bankhaus Herstatt at 3:30 PM Frankfurt time. The timing of that closure exposed a structural flaw in global payments that the industry spent five decades systematically addressing.

What Happened

Multiple counterparty banks had irrevocably transferred Deutsche Marks to Herstatt earlier that day — their leg of the foreign exchange settlement was complete and final in Germany. In return, Herstatt was required to deliver US Dollars to those counterparties through its New York correspondent, Chase Manhattan Bank.

When German regulators closed Herstatt at 3:30 PM Frankfurt time, it was 10:30 AM in New York. The New York banking day was still open. Chase Manhattan suspended all outgoing payments from Herstatt’s account. The counterparty banks had already paid — irrevocably. They never received their dollars.

Figure 4: Timeline showing DEM leg completed (Frankfurt, morning) and USD leg suspended (New York, afternoon). Red zone marks the finality gap ,the window in which one leg was complete and the other failed. This gap defines Herstatt Risk.

What It Proved

Settlement happened in two legs, in two systems, across two time zones, with a gap between them. The first leg was final. The second leg never happened. In that gap between one leg’s finality and the other leg’s initiation is where Herstatt failed.

This is Herstatt Risk: the risk that one leg of a payment transaction achieves finality while the counterpart leg fails, because finality occurs at different times in different systems.

The structural flaw is not unique to cross-border FX. It is present in any payment system where finality is not simultaneous and clearly defined. In the domestic clearing example: if SBI treats NPCI’s message acceptance as settlement and it is not. If HDFC credits Customer B before RBI settles and HDFC carries the same exposure at a domestic scale. The gap between clearing and settlement is where this risk lives regardless of geography.

The Regulatory Response

Post-Herstatt, central banks and international bodies moved systematically to address the finality gap:

- Define settlement finality in law — legally binding and operationally enforceable, not assumed

- Mandate RTGS for high-value payments — each transaction settles immediately, gap eliminated

- Drive Payment versus Payment (PvP) for FX — simultaneous finality on both legs

- Mandate central counterparties (CCPs) for clearing risk absorption in critical systems

Every settlement method in this series is a direct engineering and regulatory response to the finality timing problem Herstatt forced the industry to confront:

| Settlement Method | Response to the Finality Timing Problem |

| DNS (Part 2) | Manages the gap through netting and mandatory participation rules — gap still exists within the clearing cycle |

| RTGS (Part 3) | Eliminates the gap entirely — each transaction settles in real time, immediately and irrevocably |

| Instant Payments (Part 4) | Consumer-facing real-time finality — 24/7, seconds, built on a prefunded infrastructure |

| Cross-Border Correspondent Banking (Part 5) | Bilateral settlement across time zones and systems — finality gap exists between legs; INDA, INGA, and COVE are structural variations that each address the gap differently through netting, multi-corridor efficiency, and simultaneous cover payment mechanics |

| Key Question to Apply to Every Settlement Method: Where is finality, and what risk exposure exists in the gap before it? That question is Herstatt’s lasting contribution to payments design. |

How Does Risk Persist Between Instruction and Finality?

Three risks exist between payment initiation and final settlement. Each one disappears at the moment finality is achieved at RBI.

| Risk Type | Definition | In This Example | Eliminated At |

| Settlement Risk | One party fails to deliver after the other has already performed | SBI’s settlement instruction reaches RBI; HDFC’s account is insufficient or HDFC fails before credit | RBI final accounting entry |

| Liquidity Risk | Insufficient funds in SBI’s RBI account at the moment settlement instruction arrives | SBI’s net payable to HDFC exceeds SBI’s RBI current account balance at settlement time | RBI confirms settlement complete |

| Counterparty Risk | Counterparty defaults before settlement occurs | HDFC fails in the window between NPCI clearing and RBI settlement | RBI final accounting entry |

- Settlement risk is Herstatt’s direct legacy.

- Liquidity risk is the operational cost of settlement speed — RTGS systems require banks to hold larger intraday liquidity buffers than DNS systems, because gross settlement on every transaction demand more immediate funding than netted settlement does.

- Counterparty risk is why finality is a legal concept, not just an operational one. Regulators define finality in legislation because the point at which counterparty risk transfers must be enforceable in court, not just agreed between banks.

How Long Is the Gap? The Clearing-Settlement Timeline

Settlement does not always happen immediately after clearing. Different methods handle the clearing-to-settlement gap differently. That gap is the single most important variable distinguishing each method in this series.

| Settlement Method | Settlement Timing | Key Characteristic | Covered In |

| DNS — Deferred Net Settlement | T+0 (batch: intraday or end-of-day) | Netting compresses liquidity requirement significantly | Part 2 |

| RTGS — Real-Time Gross Settlement | T+0 (real-time, per transaction) | No netting — each transaction settles immediately, irrevocably | Part 3 |

| Instant Payments (UPI) | T+0 (seconds, 24/7) | Consumer real-time, round-the-clock, prefunded rails | Part 4 |

| Correspondent Banking | T+1 to T+2 | Cross-border bilateral — no central clearing house | Part 5 |

The regulatory direction globally has consistently been toward shorter gaps from T+2 to T+1, T+1 to T+0, batch to real-time because compressing the gap compresses the risk window. Speed of finality is a risk management outcome as much as a customer experience improvement.

| Critical Practitioner Point: Domestic settlement is not one model. The method used depends on payment type, amount threshold, and time of day. A high-value corporate payment uses RTGS. A retail batch uses DNS. A consumer transfer at 2 AM uses Instant. For a cross-border incoming payment that needs to settle via local clearing infrastructure, routing to the right rail based on amount and time is a critical design decision, not a default. Getting it wrong means payment failure or unintended delay. |

Three Misconceptions That Persist in Real Implementations

Misconception 1: Clearing and Settlement Are One Step — It All Happens at the Central Bank

This is the most common conflation in the payments industry, including among experienced practitioners. Clearing and settlement are distinct processes with different participants, different functions, and different risk implications.

Clearing happens at the clearing house at NPCI in this example. It is a message process. No money moves. Settlement happens at the central bank i.e., RBI. That is where accounting entries are posted and finality is achieved. The central bank is the settlement agent, not the clearing agent.

Conflating the two creates a dangerous gap: it obscures where risk lives between the two stages, who holds exposure, and when finality actually occurs. A bank that treats clearing confirmation as final settlement is carrying unacknowledged settlement risk on its balance sheet and may not even know it.

Misconception 2: Domestic Settlement Is Always the Same

It is not. Domestic settlement operates across three fundamentally different models depending on payment type, amount threshold, and time of day and the routing decision between them is a real design choice with consequences.

A high-value corporate payment at 2 PM routes to RTGS: real-time, gross, per-transaction finality, no netting, higher liquidity requirement. A batch retail payment cycles through DNS: netting across all banks, periodic settlement windows, significantly lower liquidity requirement. A consumer payment at midnight goes through Instant Payments: real-time finality on prefunded, 24/7 rails with hard position limits.

For a cross-border incoming payment that needs to settle through local clearing, the routing engine must evaluate amount thresholds, time windows, and system availability to select the correct rail. RTGS has cut-off times. DNS has batch windows. Instant has value limits. Sending a high-value payment to a DNS batch at the wrong time, or attempting an RTGS submission after cut-off, produces a failed or delayed settlement and not just a suboptimal one.

Misconception 3: Cross-Border Payments Without Central Clearing Infrastructure Are a Different Process

They use the same fundamental process. The infrastructure changes. This distinction matters enormously for understanding correspondent banking.

In domestic payments, NPCI sits between SBI and HDFC as a central clearing intermediary where matching, validating, netting happen, then passing net obligations to RBI for settlement. The process is centralised, standardised, efficient.

In cross-border payments where no central clearing house exists between two banks, the same clearing and settlement process still operates. It is just internalised inside or between the banks themselves. When an Indian bank and a US bank settle bilaterally through their correspondent relationship, they perform their own bilateral clearing , reconciling obligations through nostro and vostro accounts and settle directly without a third-party intermediary.

| From Practice: When designing cross-border payment rails without external clearing infrastructure, the clearing and settlement logic must be built directly into the bank-to-bank relationship. There is no NPCI. No SWIFT clearing house. The obligation tracking, bilateral netting, and settlement confirmation flows are embedded in the correspondent account management itself. The clearing still happens. The infrastructure that houses it is the banks. |

This is not simpler than domestic clearing. It is more complex, more expensive, less standardised, and carries greater bilateral counterparty risk. The clearing and settlement still happen and the infrastructure is absorbed into the banking relationship. This is exactly why INDA, INGA, and COVE (Part 5) exist: they are bilateral efficiency mechanisms that bring netting and settlement structure to corridors without centralised clearing infrastructure.

The beauty of payments is that the same fundamental two-stage process ,clearing and then settlement operates universally. The complexity is in who performs it, where the risk sits when there is no central counterparty, and what exposure lives in the gap between the two stages.

| ▶ Watch the Full Walkthrough on YouTube Prefer video? Full walkthrough on the PaymentTalks YouTube channel. Link above. |

Frequently Asked Questions

What is the difference between clearing and settlement in payments?

Clearing is the process of exchanging payment messages, matching obligations, and calculating net positions between banks. No money moves in clearing. Settlement is the process where accounting entries are posted at the central bank and value transfers — the moment finality is achieved. Clearing identifies what is owed. Settlement delivers it. Treating them as one step is the most common source of settlement risk misidentification in real implementations.

When exactly does a payment become final and irrevocable?

Finality occurs when the settlement agent, typically the central bank, posts the accounting entries debiting the sending bank’s account and crediting the receiving bank’s account. In India’s domestic clearing, finality occurs when RBI posts entries to SBI’s and HDFC’s current accounts at RBI. Not when Customer A sends the instruction. Not when NPCI processes the message. At RBI and nowhere earlier.

What is Herstatt Risk and why does it still matter?

Herstatt Risk is the risk that one leg of a payment transaction achieves finality while the counterpart leg fails, because settlement occurs at different times in different systems. Named after Bankhaus Herstatt, which collapsed in 1974 after counterparties had irrevocably paid Deutsche Marks but before Herstatt delivered US Dollars in New York. It remains the foundational risk concept behind RTGS design, PvP settlement, and finality legislation globally. Every settlement method architecture is, directly or indirectly, a response to the problem Herstatt exposed.

Does NPCI actually move money during clearing?

No. NPCI operates as the clearing infrastructure processing messages, validating, matching, and tracking net obligations in notional clearing accounts. No real value resides at NPCI. NPCI passes net settlement instructions to RBI. RBI moves the money by debiting and crediting bank current accounts. NPCI’s notional accounts are obligation-tracking ledgers, not value-holding accounts.

What are the three domestic settlement methods and when does each apply?

DNS (Deferred Net Settlement) applies to batched retail payments where netting reduces liquidity requirements. RTGS (Real-Time Gross Settlement) applies to high-value, time-critical payments requiring immediate gross finality. Instant Payments (IMPS in India) applies to consumer payments 24/7 where round-the-clock real-time finality is required on prefunded rails. The routing decision between the three depends on payment type, amount threshold, time of day, and system availability ; not a single default.

How does cross-border payment clearing and settlement work without a central clearing house?

The same two-stage process clearing then settlement still occurs. Without a central clearing house, the clearing function is internalised into the bilateral banking relationship. Banks use nostro and vostro accounts to track and reconcile obligations (bilateral clearing) and settle directly or through correspondent banks. There is no central counterparty absorbing risk, which is why cross-border bilateral settlement carries more counterparty risk, more cost, and less transparency than domestic centralised clearing.

What is the difference between provisional and final settlement?

Provisional settlement is an accounting entry that has been recorded but is not yet irrevocable and it can be reversed. Counterparty risk has not been eliminated. Final settlement is irrevocable and unconditional and no reversal is possible, counterparty risk ends, and the payment is legally complete. Banks that treat provisional entries as final are carrying settlement risk they may not be accounting for. The distinction between these two states is particularly important in correspondent banking, where value movements may pass through provisional states for hours before final settlement occurs.

Why did regulators mandate RTGS for high-value payments?

Because Herstatt demonstrated that a gap between clearing and settlement is systemic risk, not operational inconvenience. DNS systems accumulate obligations through the day before settling in batch and every obligation in that batch is at settlement risk until finality. For high-value payments, the exposure in that gap is too large to accept. RTGS eliminates the gap by settling each transaction immediately and irrevocably. The higher liquidity cost of gross settlement is the price of eliminating settlement risk entirely for high-value flows.

Three Things to Carry Into Every Part That Follows

Every part in this series traces the same journey: instruction, clearing, settlement, finality. The settlement method changes. The framework does not.

- Clearing is message exchange. No money moves. The clearing house validates, matches, and nets obligations in notional tracking accounts. Nothing has settled until the central bank posts accounting entries. “In clearing” is not “payment done.”

- Settlement is accounting. Money moves. Finality is achieved. The moment RBI debits one bank’s account and credits another and that is the moment that matters. Everything before it is provisional. Everything after is irrevocable.

- Finality timing is systemic risk and not a technicality. Herstatt proved it in 1974. Every settlement method in this series is a regulatory and engineering response to that lesson: DNS manages the gap, RTGS eliminates it, Instant Payments extends real-time finality to consumers, INDA, INGA and COVE addresses it in cross-border flows.

In Part 2, Deferred Net Settlement, the same infrastructure runs across multiple banks with real netting calculations. The clearing-to-settlement gap is examined in full, with the liquidity mechanics that make DNS the workhorse of domestic payment systems globally.

The framework is set. The mechanics begin.

PaymentTalks | Clearing and Settlement Methods Masterclass | Part 1 of 6