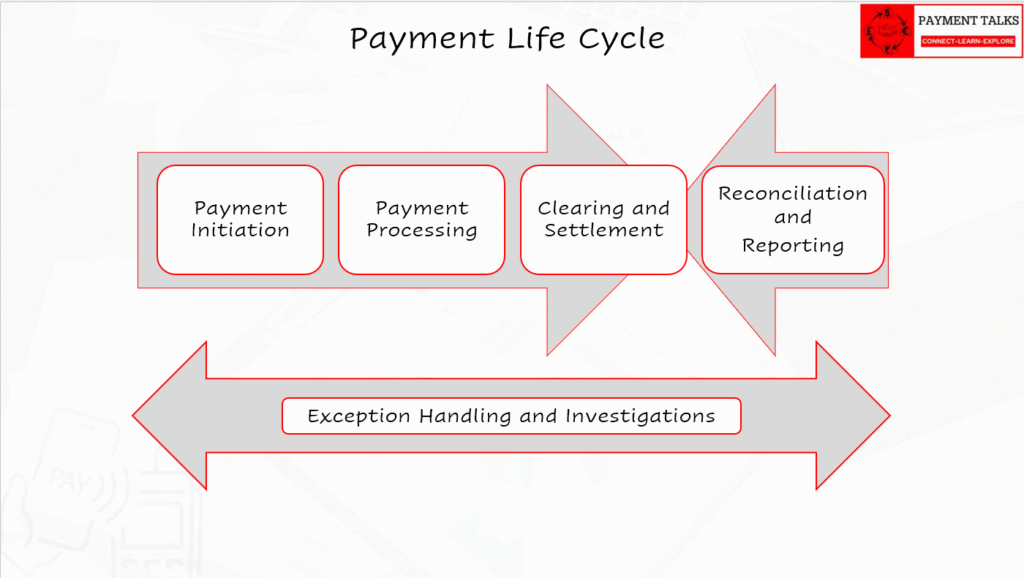

[VISUAL 1: Payment Life Cycle: 5-stage overview from Initiation through Exception Handling]

What Is the Payment Life Cycle?

Payment life cycle is not that complex if you really understand these 5 fundamental steps.

Every payment, regardless of channel, amount, or destination, goes through the same pipeline: Initiation, Processing, Clearing and Settlement, Reconciliation and Reporting, and Exception Handling. Five stages. The complexity you see in any specific payment system is usually one stage failing to interface cleanly with the next.

This article walks all five stages in sequence, covering what happens at each step, which systems are involved, which messages flow, and what breaks when something goes wrong. Part 1 covers Initiation and Processing. Part 2 covers Clearing, Settlement, Reconciliation, and Exception Handling. Video walkthroughs for both parts are embedded at the right stage break points.

Before going deeper into any single topic, whether that is PAIN.001 payment initiation, correspondent banking, or ISO 20022 message standards, understanding this end-to-end map first will save you significant time.

Stage 1: How Does a Payment Start? (Payment Initiation)

Payment Initiation is the customer-facing starting point. This is where the payer, whether an individual, a corporate, or an automated system, creates the instruction that tells the bank: move funds from this account to that one.

What Channels Can Initiate a Payment?

Retail channels: mobile banking app, internet banking, branch teller, ATM, phone banking.

Corporate channels: host-to-host connections via SFTP or API, bulk file uploads such as PAIN.001 ISO 20022 files, treasury management portals, and ERP system integrations.

Alternate rails: card networks, direct debits, standing orders, and instant payment apps. Note that card authorisation and settlement follow a different flow from bank transfer initiation.

What Data Does a Payment Instruction Carry?

Every payment instruction, regardless of channel, captures the same core data:

- Debtor (payer): account number or IBAN, account currency

- Creditor (beneficiary): account number or IBAN, bank identifier such as BIC, LEI, or local bank code

- Payment details: amount and currency, value date or requested execution date

- Charge bearer: OUR, SHA, or BEN — determines who absorbs the transaction fees. See Charge Codes in SWIFT: OUR / BEN / SHA for a full breakdown.

- Other metadata: remittance information such as invoice references, instruction flags for urgent, bulk or batch, and purpose codes

For a full view of all agents and parties involved in a payment message, see All Agents and Parties in an ISO Payment Message.

How Are Customers Authenticated and Authorised?

Retail: Strong Customer Authentication (SCA) using OTP, biometrics, or hardware tokens.

Corporate: multi-signatory flows with maker-checker controls, approval workflows in treasury systems, and delegated authorisation.

Cards: card and merchant flows include pre-authorisations and holds. This authorisation step is distinct from bank transfer authorisation.

What Preliminary Checks Run at Initiation?

Before the instruction reaches the processing engine, the front-end systems run:

- Syntax and format validation: IBAN structure, field lengths, mandatory fields

- Funds availability check — some systems place a temporary hold at this point

- Basic fraud indicators: velocity checks, unusual payee patterns

- KYC and account status checks: is the account active, dormant, or blocked?

What Does the Bank Do with the Instruction Next?

If validation passes, the instruction is accepted and queued for the payment processing engine. If validation fails, it returns to the originator with an error code.

For bulk corporate files, the bank runs additional checks: file schema validation, cryptographic or signatory verification, and per-transaction row validation before accepting the full batch.

Example: a CFO uploads a bulk PAIN.001 file for USD payments. The bank’s front-end validates the file format, checks the signatories, and confirms debit account balances. The file then proceeds to the payment processing engine.

Stage 2: What Happens Inside the Bank? (Payment Processing)

Payment Processing is where the bank’s internal engine takes the instruction and turns it into a settled movement of value. It decomposes into two clear phases: Pre-Processing and Payment Execution.

What Is Payment Pre-Processing?

Pre-Processing covers all validation, enrichment, and compliance checks that the payment instruction must pass before the processing engine accepts it for routing and settlement. Think of it as the quality gate. Nothing enters the execution phase unless it clears this gate.

- Business rules and data validation: account status, currency permissions, IBAN and BIC verification, daily and per-transaction limits.

- Sanctions and AML screening: name and transaction screening against watchlists and behavioural models. Hits route for compliance investigation.

- Fraud scoring: device fingerprinting, velocity checks, and anomaly detection.

- Enrichment: appending Standard Settlement Instructions (SSIs), BIC lookups, correspondent banking chain data, and additional remittance details so the payment becomes routable with minimal manual intervention.

Pre-Processing bridges Payment Initiation and Payment Execution. What enters the processing engine must be accurate, compliant, and ready for settlement.

How Does Payment Execution Work?

Once the payment clears pre-processing, execution covers routing, authorisation, FX, accounting, and message preparation.

Routing

Routing determines the optimal path to the beneficiary bank. Key factors:

- Payment scheme availability: ACH, RTGS, instant rail, cross-border SWIFT, or proprietary networks.

- Cut-off times: ensure same-day or priority deadlines are met.

- Cost vs speed: banks prefer lower-cost ACH for non-urgent payments and RTGS for high-value or time-critical ones.

- Correspondent banking chain: for cross-border payments, select the intermediary bank with valid currency nostro accounts. See Understanding Correspondent Banking for how these chains are structured.

- Network and compliance rules: routing must comply with scheme-specific rules such as TARGET2 in Europe, Fedwire in the US, or SARIE in Saudi Arabia.

Routing engines use decision trees, rules-based logic, or AI-driven optimisers. For how the bank determines which parties to debit and credit at each hop, see Debit-Credit Party Derivation (DPD/CPD).

Authorisation and Workflow

Retail: final SCA confirmation. Corporate: multi-level approvals, maker-checker, exception escalation. High-value or flagged payments require operations or compliance sign-off.

Pricing and FX

Charge calculation applies flat, percentage, or tiered fees. The charge bearer (OUR, SHA, or BEN) determines who absorbs them. If the payment crosses currency, the bank applies an exchange rate, books the FX gain or loss, and displays the rate to the customer where required.

Accounting and Booking

At this point the bank posts double-entry ledger entries for both the customer debit and the bank’s settlement movement. Two common fee scenarios:

Case 1 — OUR (debtor bears full fee):

- Debit: Customer deposit account — $1,005 (payment $1,000 + fee $5)

- Credit: Settlement/Nostro funding account — $1,000

- Credit: Fee income — $5

Case 2 — Fee deducted from payment proceeds:

- Debit: Customer deposit account — $1,000

- Credit: Settlement/Nostro funding account — $995 (amount sent onward)

- Credit: Fee income — $5

Always verify your bank’s posting conventions. Some banks use suspense or clearing accounts during processing.

Message Transformation and STP

The payment’s internal format is converted to an interbank message format: ISO 20022 PACS.008 (customer credit transfer) or PACS.009 (financial institution transfer), or an equivalent MT message. Straight-through processing (STP) rate measures the percentage of payments completing this step without manual intervention.

Payments may be queued until the bank’s cut-off for the relevant rail (for ACH batches) or sent immediately for RTGS or instant rails. For cross-border SWIFT payments, the SWIFT GPI Tracker is updated at this stage.

What Exceptions Occur During Processing?

- Sanctions hit: payment held and escalated to compliance.

- Insufficient funds: rejected or queued depending on the product.

- Data errors: returned to originator with an error code and remediation guidance.

Key Metrics for Payment Processing

- STP rate: percentage of payments auto-processed end-to-end

- Routing success rate: payments delivered via the first-choice path

- Processing latency: time from initiation to outbound send

- Exception volume: manual interventions per 1,000 transactions

► Watch on YouTube: Part 1: Initiation and Processing

https://www.youtube.com/watch?v=EcNgTrm5Vig

Prefer video? Watch the full walkthrough on the PaymentTalks YouTube channel.

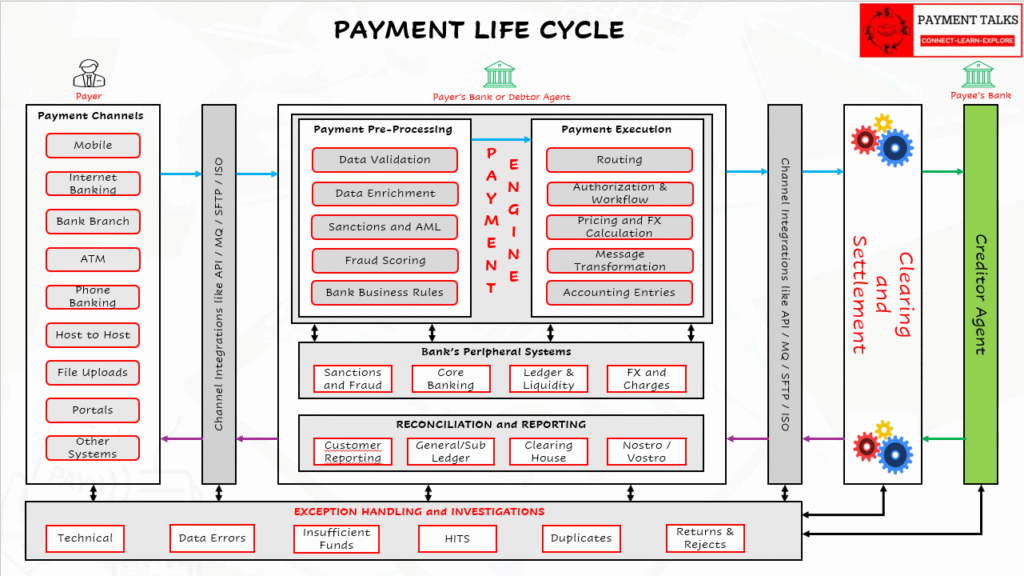

[VISUAL 2: Payment Life Cycle: 5-stage overview from Initiation through Exception Handling]

Stage 3: When Does Value Actually Move Between Banks? (Clearing and Settlement)

Clearing and Settlement is where interbank value transfer actually happens. This stage determines when funds movement becomes final between institutions.

What Is the Difference Between Clearing and Settlement?

Clearing: the exchange and sometimes netting of payment instructions between institutions or through a clearing house.

Settlement: the actual transfer of value — debiting and crediting settlement accounts held in central bank money, correspondent nostro accounts, or settlement engines.

The distinction matters. A payment can be cleared but not yet settled. Until settlement is complete and final, counterparty risk remains.

What Settlement Models Do Banks Use?

ACH — Deferred Net Settlement (DNS)

Low-value retail payments are batched and netted. Settlement runs at one or more defined times per day between participating banks. Lower liquidity footprint, but participants carry intraday risk between batch windows. For a full breakdown of domestic settlement models, see Domestic Payment Processing Methods.

RTGS — Real-Time Gross Settlement

Each payment settles individually and immediately in central bank money. Used for high-value and time-critical payments. Provides legal finality and eliminates intraday credit risk.

Instant and Faster Payment Systems

Near real-time rails with immediate customer credit. Requires 24×7 processing capability and always-on fraud controls.

Cross-Border and Correspondent Banking

There is no single global RTGS for retail cross-border payments. Banks route through correspondent and nostro chains. The sending bank debits a local nostro account held at a correspondent, which credits the beneficiary bank or the next intermediary. Multiple hops mean more FX conversions, more failure points, and longer settlement windows.

For a complete guide to how nostro, vostro, and loro accounts work in these chains, see Nostro, Mirror Nostro, Vostro, and Loro Accounts.

What Messages Are Exchanged During Clearing?

- The sending bank transmits an interbank payment message — typically ISO 20022 PACS.008 (customer credit transfer) or PACS.009 (financial institution transfer) — to the receiving bank or clearing house.

- The clearing or settlement operator, or the receiving bank, returns status messages and settlement confirmations via PACS.002 or equivalent system-level messages.

- If the beneficiary bank identifies a problem such as a wrong account, closed account, or regulatory block, it generates a payment return message via PACS.004 or equivalent, with a standardised reason code.

What Is Settlement Finality and Why Does It Matter?

Finality means the settlement cannot be reversed or unwound. RTGS and most instant payment systems provide legal finality once settled. ACH settlements may be reversed within defined windows.

Banks must maintain sufficient intraday liquidity to fund settlement positions, using central bank facilities, repo lines, or intraday overdrafts. Failed or stuck settlements require active intraday monitoring and sometimes manual funding intervention.

How Do Domestic vs Cross-Border Settlements Differ?

Domestic ACH: Bank A batches customer debits at 16:00. The clearing house nets all positions and instructs the central bank to settle at 17:30. Once Bank A’s net debit is posted, beneficiary banks can credit their customers.

Cross-border: Bank A sends the instruction to Correspondent Bank X via its nostro. Correspondent Bank X debits Bank A’s nostro account and credits Bank B, possibly through further intermediaries. Confirmation flows back to Bank A. Settlement may be same-day or T+1 to T+2 depending on the corridor.

KPIs for Clearing and Settlement

- Settlement finality rate: successful settlements versus total attempts

- Liquidity utilisation: intraday liquidity shortfall events

- Time to settlement by corridor: instant versus same-day versus T+1

Stage 4: How Do Banks Verify That Everything Balanced? (Reconciliation and Reporting)

Reconciliation is post-settlement verification. The goal: confirm that every ledger entry, settlement message, and third-party report matches, then produce the customer and regulatory reports that close the loop.

What Types of Reconciliation Run After Settlement?

- Nostro and vostro reconciliation: match internal expected postings against correspondent bank statements in formats such as CAMT.053 or MT940.

- Clearing house reconciliation: verify participation reports and net positions provided by the ACH or RTGS operator.

- GL and sub-ledger reconciliation: ensure the general ledger, cash position, and sub-ledgers reconcile to the posted payments.

- Transaction-level match: match settlement references, amounts, and timestamps between internal records and external confirmations.

What Happens to Unmatched Items?

Unmatched or partially matched items move into suspense accounts and are investigated by operations teams. Common causes: reference mismatches, rounding differences, intermediary fees deducted in transit, or timing differences between internal booking and external settlement.

How Do Banks Report to Customers?

Real-time notifications via push alerts, SMS, webhooks, or email confirm successful or failed payments.

Statements and advice messages: CAMT.053 (bank statement), CAMT.054 (debit/credit advice), and legacy MT940 provide customers with periodic transaction detail. Corporates frequently use CAMT messages for automated straight-through reconciliation in their ERP systems.

What Regulatory Reporting Is Required?

AML and suspicious activity reporting: transactions flagged by behavioural rules or threshold monitoring are escalated to compliance and, where required, reported to the relevant authority.

Central bank and prudential reporting: payment statistics, liquidity reports, and audit trails maintained for supervisory review.

KPIs and Controls for Reconciliation

- Reconciliation lag: time to clear all outstanding mismatches — target typically same-day or T+1

- Nostro matching accuracy

- STP rate for reconciliation: auto-matched versus manual touch

- Timeliness of customer notifications

Stage 5: What Happens When a Payment Fails? (Exception Handling and Investigation)

Exception handling covers the detection, investigation, remediation, and closure of anything that goes wrong at any stage of the payment life cycle. Every payment operation has exceptions. How quickly and cleanly you handle them defines your operational quality.

What Types of Exceptions Occur in the Payment Life Cycle?

- Technical failures: network outages, message format errors, failed MT-to-MX translation.

- Data errors: wrong account number, malformed IBAN, missing mandatory fields.

- Insufficient funds: rejected or queued depending on the product.

- Sanctions and compliance hits: payment held pending investigation, potential mandatory regulatory reporting.

- Returns and recalls: beneficiary bank returns funds due to a closed account or wrong beneficiary, or the originator requests a recall.

- Duplicate payments: duplicate instruction detection and remediation.

How Does an Exception Investigation Work?

- Detection and alerting: automated monitoring flags the exception — failed settlement, returned message, compliance alert.

- Triage: systems classify severity by fraud risk, financial exposure, and customer impact.

- Root cause analysis: operations, compliance, or technology teams trace message flows, timestamps, intermediary legs, and audit logs.

- Correction and remediation: repair data and repost, initiate a return or re-issue, reimburse the customer where required.

- Communication: notify affected customers and counterparties with clear reason codes and next steps.

- Escalation and reporting: escalate high-risk incidents to compliance or legal, file regulatory reports where required.

What Message Codes Are Used in Exception Handling?

ISO 20022 return messages such as PACS.004 carry standardised reason codes that identify whether a return is due to account closure, incorrect details, or a regulatory block. Using standardised codes significantly reduces investigation time because both sending and receiving banks work from the same code set. For a deeper look at ISO 20022 message standards and building blocks.

How Are Exceptions Accounted For?

Reversal entries, suspense postings, and adjustments are posted depending on root cause.

Example: if a payment is returned after it has already been booked, the bank posts reversing entries to restore the customer balance and correct the settlement account. If fees were charged incorrectly, the bank credits or debits fee income and the customer account accordingly.

What Are the SLAs and Timelines for Exception Resolution?

Define SLAs at three points: initial response, investigation completion, and customer remediation. A typical high-severity target is initial triage within one business hour. Full resolution windows range from same-day to T+2 depending on regulation, product, and corridor.

How Do Banks Prevent Exceptions?

- Strengthen STP and data validation at initiation — catch errors before they enter the pipeline

- Robust sanctions screening and case management reduce compliance exceptions

- Real-time intraday liquidity monitoring prevents settlement fails

- Automated duplicate detection and reconciliation catches issues earlier and reduces manual workload

KPIs for Exception Handling

- Settlement fail rate: number and value of failed settlements

- Exception rate: manual interventions per 1,000 payments

- Mean time to resolution (MTTR)

- Compliance case closure time

- Percentage of exceptions prevented by pre-validation or automated rules

► Watch on YouTube: Part 2: Clearing, Settlement, Reconciliation and Exception Handling

https://www.youtube.com/watch?v=NUo7q0jMUp8

Prefer video? Watch the full walkthrough on the PaymentTalks YouTube channel.

What Makes a Payment Operation Genuinely Efficient?

Five stages. One pipeline. The principle is straightforward — the implementation rarely is.

High-performing payment operations share the same fundamentals: strong STP at initiation and processing, well-defined correspondent banking chains with clean SSIs, active intraday liquidity management, and a reconciliation process that closes daily without carry-forward exceptions.

Exception handling is not a separate discipline. It feeds directly back into the design of every stage before it. The exception rate is a diagnostic of how well the first three stages are engineered.

For cross-border flows, add another layer of design thinking: expect more intermediaries, longer settlement timelines, and additional FX and compliance touchpoints. The correspondent banking chain decisions you make at the start of a project determine the operational complexity you manage every day after go-live.

The five stages do not change. What changes is how well each one is engineered.

Frequently Asked Questions

What are the five stages of the payment life cycle in banking?

The five stages are: Payment Initiation, Payment Processing, Clearing and Settlement, Reconciliation and Reporting, and Exception Handling and Investigation. Every banking payment, regardless of channel or geography, passes through all five stages in this sequence.

What is the difference between payment clearing and settlement?

Clearing is the exchange and netting of payment instructions between institutions. Settlement is the actual transfer of value — funds moving between accounts at a central bank or correspondent. A payment can be cleared but not yet settled. Until settlement is final, counterparty risk remains.

What is payment pre-processing in banking?

Pre-processing covers validation, enrichment, and compliance checks — including AML screening, fraud scoring, and IBAN/BIC verification — that a payment must pass before the processing engine routes it for settlement. It is the quality gate before execution.

What is STP (straight-through processing) in payments?

STP is the automated end-to-end processing of a payment without any manual intervention. A high STP rate indicates a well-designed initiation, validation, and routing pipeline. Banks track STP rate as a core operational KPI.

What is settlement finality and why does it matter?

Settlement finality means a transfer cannot be reversed once completed. RTGS systems and most instant payment rails provide legal finality. ACH settlements may be reversed within defined windows. Finality determines when counterparty risk ends for both the sending and receiving institutions.

What happens to a payment that fails during processing?

Depending on the failure type, the payment is rejected and returned to the originator with an error code, held for compliance investigation in the case of a sanctions hit, or queued pending resolution for insufficient funds. ISO 20022 return messages carry standardised reason codes to speed up investigation.

How does cross-border payment settlement differ from domestic?

Domestic payments settle through a single clearing house in defined batch windows (ACH) or immediately via RTGS. Cross-border payments route through correspondent banking chains, may involve multiple intermediaries and FX conversions, and settle in T+1 to T+2 windows depending on the corridor. Each additional hop adds complexity, cost, and potential failure points.

What is nostro reconciliation in banking?

Nostro reconciliation is matching a bank’s internal expected postings against the statements received from its correspondent bank, typically in CAMT.053 or MT940 format. Unmatched items move to suspense accounts for investigation. Clean daily nostro reconciliation is a core indicator of payment operations health.