The Problem That Has Persisted for Fifty Years

A company in the United Arab Emirates wins a contract with a buyer in China. The UAE company ships the goods. Now it needs to receive payment — $4 million USD equivalent, routed from a Chinese bank to a UAE bank.

What happens next is not elegant. A SWIFT message leaves China. It passes through one or more correspondent banks, typically routing through a US dollar clearing bank. Each correspondent charges a fee. The FX conversion happens somewhere in the chain, often at a rate the UAE company never explicitly agreed to. The funds arrive — sometimes in one day, sometimes in three — minus accumulated fees that the UAE company only discovers after the fact.

This is not a niche problem. Cross-border payments between Asia, the Middle East, and beyond move trillions of dollars annually through exactly this friction-filled correspondent banking model. The infrastructure was largely designed in the 1970s. It has not fundamentally changed.

mBridge is the most serious attempt by central banks to change it — not by building another layer on top of the existing system, but by replacing the settlement layer entirely with a shared, multi-central-bank digital currency platform.

This article covers everything: what mBridge is, how it works at a technical and operational level, who is involved, what has actually been transacted on it, how it compares to existing SWIFT infrastructure, and what it means for payments professionals — from a fresher learning the landscape to a solution architect planning the next decade of infrastructure.

Section 1: What Is mBridge?

“mBridge (short for Multiple Central Bank Digital Currency Bridge) is a shared distributed ledger platform that enables real-time, peer-to-peer cross-border payments and foreign exchange settlements directly between commercial banks, using wholesale Central Bank Digital Currencies (CBDCs) — digital forms of sovereign money issued by participating central banks.”

Every word in that definition matters. Let us unpack it.

Shared distributed ledger platform: mBridge is not a messaging network like SWIFT. It is not a payment switch like Fedwire. It is a blockchain — a shared ledger maintained by multiple participating nodes — where the participants include central banks and their supervised commercial banks. Every transaction is recorded on this shared ledger, visible to all participants, and settled with finality at the moment it executes.

Real-time, peer-to-peer: Payments on mBridge settle directly between the originating commercial bank and the receiving commercial bank, with no correspondent bank intermediary. The settlement is immediate and final — not end-of-day, not next-day, not “subject to correspondent processing.” It is Seconds.

Wholesale CBDCs: The assets being transferred on mBridge are not SWIFT messages instructing a bank to move money. They are tokenised central bank money — digital currencies issued directly onto the mBridge ledger by each participating central bank. When the Hong Kong Monetary Authority issues HKD CBDC onto the platform and the Central Bank of UAE issues AED CBDC, and those two tokens are swapped in a trade settlement, both the payment and the FX conversion happen atomically — at the same instant, with zero counterparty risk.

Who initiated it: mBridge was conceived and developed by the BIS Innovation Hub (Bank for International Settlements Innovation Hub) in collaboration with the four founding central bank participants. The BIS — often described as “the central bank of central banks” — provides the research, coordination, and governance backbone. That institutional backing gives mBridge a credibility that private blockchain payment projects simply cannot match.

Section 2: The Origin Story — Why mBridge Was Built

To understand why mBridge matters, you need to understand what it was built to replace — and why that existing infrastructure falls so badly short.

The Correspondent Banking Problem at the Wholesale Level

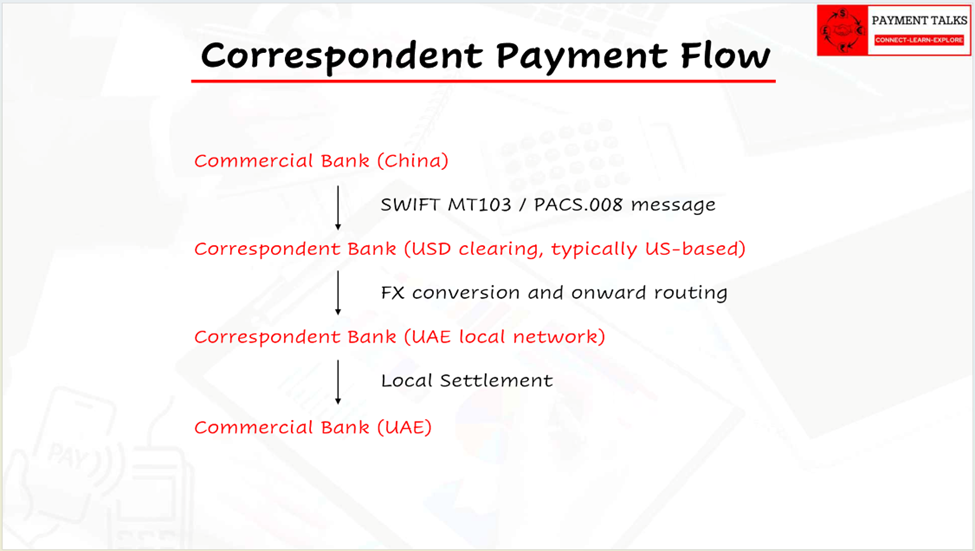

When Bank A in China needs to pay Bank B in the UAE, neither bank likely has a direct account relationship with the other. They rely on correspondent banks — typically US banks with broad global networks — to intermediate the transaction.

The flow looks like this:

Each hop introduces:

- A fee (typically $5–$25 per correspondent hop)

- A delay (cut-off times, processing windows, time zone gaps)

- An FX margin (embedded in the conversion rate, not separately disclosed)

- A loss of transparency (the originating bank cannot track the payment in real time once it leaves their correspondent)

For a $4 million trade settlement, these inefficiencies are irritating but manageable. For the aggregate of global trade finance — which the BIS estimates requires banks to hold trillions of dollars in pre-funded nostro accounts (accounts that banks maintain at foreign correspondent banks to facilitate payments) — the cost is staggering.

The Nostro Account Problem

The correspondent banking model requires banks to pre-fund currency positions. If Bank A in Hong Kong wants to be able to process USD payments for its clients, it must maintain a balance in a USD nostro account at a US correspondent — money sitting idle, earning minimal return, just to be available as a liquidity buffer for client payments.

The BIS has estimated that the global banking system holds approximately $10 trillion in pre-funded nostro/vostro account balances at any given time. That is capital tied up doing nothing — not lending, not earning return, not productive — simply waiting to be used to facilitate international payments.

mBridge, by enabling atomic real-time settlement in central bank money, dramatically reduces or eliminates the need for pre-funded nostro positions in the corridors it covers. A bank could, in principle, source liquidity just-in-time from the mBridge platform rather than holding weeks of idle pre-funded balances.

The Geopolitical Dimension

There is a dimension to mBridge that goes beyond pure payment efficiency — and payments professionals need to be aware of it.

The global correspondent banking system is dominated by US dollar clearing. SWIFT, while technically a Belgian cooperative, processes the vast majority of international financial messages. The US has demonstrated willingness to use this infrastructure as a foreign policy tool — most dramatically in 2022, when Russia was excluded from SWIFT following the invasion of Ukraine, effectively cutting Russian banks off from the global dollar payment system.

For central banks in Asia, the Middle East, and beyond, this creates a strategic vulnerability. A payment infrastructure that does not route through US correspondent banks or SWIFT reduces that exposure. mBridge, by enabling direct central-bank-to-central-bank settlement in the parties’ own currencies, offers an alternative settlement pathway.

The BIS has been careful to frame mBridge as a technical efficiency project, not a geopolitical one. But the participation of China’s People’s Bank of China, and the interest from Global South economies, reflects a broader strategic interest in payment infrastructure that is not dependent on US dollar clearing.

Section 3: The Participants

mBridge launched as a collaboration between four founding central bank participants and the BIS Innovation Hub. As of 2024–2025, the platform has expanded.

Founding Central Bank Participants

Bank for International Settlements (BIS) Innovation Hub — Hong Kong Centre The BIS provides governance, research leadership, and technology coordination. The BIS Innovation Hub’s Hong Kong Centre hosts the primary technical development. The BIS does not issue currency on mBridge — its role is convener, researcher, and platform steward.

Hong Kong Monetary Authority (HKMA) Hong Kong’s de facto central bank. Issues HKD CBDC on the mBridge platform. Hong Kong’s role as a major financial centre and gateway between China and global capital markets makes it a critical participant. The HKMA has been one of the most technically advanced CBDC development authorities globally.

People’s Bank of China (PBoC) China’s central bank. Issues e-CNY (digital yuan) on the mBridge platform. China’s participation is the most significant single factor in mBridge’s geopolitical importance. The PBoC has the most advanced retail CBDC in the world (e-CNY, with billions in transactions live). Its wholesale CBDC capabilities feed directly into mBridge.

Central Bank of the UAE (CBUAE) Issues AED CBDC on the mBridge platform. The UAE’s position as a major trade and financial hub — particularly for Asia-Middle East trade flows — makes it a high-value corridor participant. The CBUAE has been among the most forward-thinking Gulf central banks on CBDC development.

Bank of Thailand (BOT) Issues THB CBDC on the mBridge platform. Thailand is a significant trade partner for both China and the UAE, with substantial cross-border payment flows in both directions.

Expanded Participation (2024 Onwards)

In June 2024, mBridge announced the addition of Saudi Arabia’s central bank (SAMA — Saudi Central Bank) as a full participant. Saudi Arabia joining is significant — it is the largest economy in the Arab world and a major oil exporter to Asia. Cross-border payments between Saudi Arabia and China are among the highest-value flows in the Gulf-Asia corridor.

As of 2025, mBridge has also invited additional central banks to participate as observer members — jurisdictions that can access the platform and run pilots without full membership. This includes central banks from Southeast Asia, the Middle East, and Africa.

The expanding participation reflects a key design principle: mBridge is built to be multi-jurisdictional by architecture, not a bilateral arrangement. New central banks can onboard without restructuring the platform.

Section 4: The Technology — How mBridge Actually Works

This is where mBridge separates itself from everything that came before it. The technology is not a patch on existing infrastructure — it is a ground-up redesign of how cross-border settlement works.

The mBridge Ledger (mBL) — Purpose-Built Blockchain

mBridge runs on its own purpose-built blockchain: the mBridge Ledger (mBL). This is not Ethereum, not Hyperledger Fabric, not Corda. It was designed specifically for central bank requirements — high throughput, deterministic finality, privacy controls, and governance mechanisms appropriate for sovereign institutions.

The mBL is a permissioned distributed ledger — not an open public blockchain. Only authorised nodes can participate in transaction validation. The nodes are operated by:

- The participating central banks (each runs one or more validation nodes)

- The BIS Innovation Hub (technical coordination node)

- Potentially licensed commercial banks (as observer or transacting nodes, depending on their authorisation level)

This permissioned structure gives the platform the control and governance that central banks require, while still delivering the core DLT benefits: shared visibility, tamper-evident records, and the ability to execute smart contracts for atomic settlement.

Consensus Mechanism

The mBL uses a BFT (Byzantine Fault Tolerant) consensus mechanism — specifically designed for environments where participants are known and regulated, but the system must be resilient to any single node failing or acting incorrectly.

BFT consensus delivers deterministic finality — when a transaction is confirmed on the mBL, it is final. Not probabilistically final (like Bitcoin, where reversal becomes increasingly improbable with each block). Definitively, irreversibly final. This is a non-negotiable requirement for central bank settlement infrastructure.

How CBDC Is Issued on mBridge

Each participating central bank issues its own CBDC onto the mBridge ledger. This issuance process is critical to understand — it is what makes mBridge fundamentally different from a private stablecoin or messaging-only network.

Step 1 — Central bank creates CBDC tokens on mBL When the HKMA wants to make HKD liquidity available for mBridge transactions, it instructs the mBL to mint HKD CBDC tokens. These tokens represent direct claims on the HKMA — they are the digital equivalent of Hong Kong Dollar reserves.

Step 2 — Commercial banks fund their mBridge wallets A commercial bank in Hong Kong (say, HSBC Hong Kong) that wants to transact on mBridge deposits HKD with the HKMA. The HKMA issues an equivalent amount of HKD CBDC tokens to HSBC’s wallet on the mBL. HSBC now holds HKD CBDC on the mBridge platform.

Step 3 — Transaction execution HSBC Hong Kong can now transact in real time on the mBL. It can send HKD CBDC to a UAE commercial bank in exchange for AED CBDC — the FX swap and settlement happening simultaneously on the platform.

Step 4 — Redemption When a commercial bank wants to convert its mBridge CBDC back to fiat, it redeems the tokens with the issuing central bank. The central bank burns the tokens on the mBL and credits the commercial bank’s reserve account in the traditional RTGS system.

This issuance-redemption cycle mirrors the mint-burn lifecycle of private stablecoins — but with one critical difference: the token is issued by a central bank, not a private company. It is sovereign money from issuance to redemption.

The Atomic Swap — The Core Settlement Innovation

The most technically significant feature of mBridge is its atomic swap capability for cross-currency settlement.

An atomic swap is a transaction where two legs — the payment of Currency A and the receipt of Currency B — execute simultaneously and indivisibly. Either both legs succeed, or neither does. There is no window of time where one party has paid and the other has not yet received. Counterparty risk — the risk that the party on the other side defaults between the initiation and completion of settlement — is eliminated at the protocol level.

To understand why this matters, consider what happens today in a cross-border FX settlement:

Traditional settlement:

- Bank A sends USD to Bank B (Leg 1) — this settles

- Several hours (or a day) later, Bank B sends EUR to Bank A (Leg 2) — this settles

Between Step 1 and Step 2, there is a window of risk. If Bank B defaults after receiving USD but before paying EUR, Bank A loses its USD. This is called Herstatt risk — named after Bankhaus Herstatt, a German bank that collapsed in 1974 mid-way through FX settlement, leaving counterparties holding their side of the trade with nothing in return. Herstatt risk is why the global banking system operates extensive FX settlement risk mitigation infrastructure (CLS Bank settles approximately $6.5 trillion daily specifically to manage this risk).

mBridge atomic swap: Both legs — HKD CBDC debit from Bank A’s wallet and AED CBDC credit to Bank A’s wallet, simultaneously with AED CBDC debit from Bank B’s wallet and HKD CBDC credit to Bank B’s wallet — execute in a single transaction on the mBL. If any element fails, nothing settles. Herstatt risk does not exist.

This is not a marginal improvement. It is the elimination of a category of risk that has required an entire global infrastructure (CLS Bank) to manage for decades.

Section 5: The Transaction Flow — A Complete Walk-Through

Let us trace a real transaction on mBridge end to end, using a concrete scenario.

The Scenario

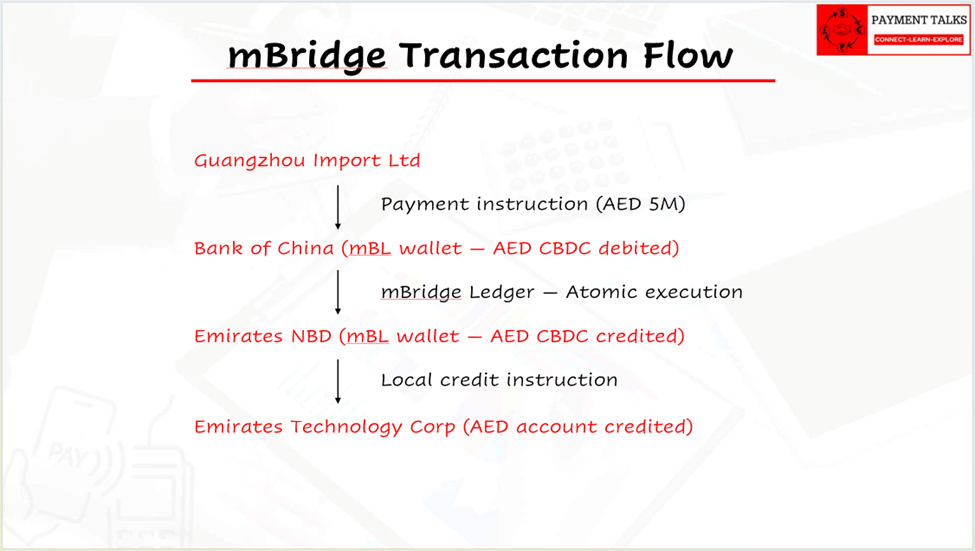

Debtor: Guangzhou Import Ltd — a Chinese manufacturing company importing electronic components. Creditor: Emirates Technology Corp — a UAE technology supplier. Amount: AED 5,000,000 (approximately USD 1.36 million). Debtor’s Bank: Bank of China (BOC) — a participant on mBridge. Creditor’s Bank: Emirates NBD — a participant on mBridge.

Step-by-Step Flow

Step 1 — Guangzhou Import Ltd initiates the payment

Guangzhou Import Ltd instructs Bank of China to make an AED 5,000,000 payment to Emirates Technology Corp. The payment instruction includes all required information: Creditor name, account details, payment purpose, remittance information. This looks like a standard corporate payment instruction.

Step 2 — Bank of China prepares the mBridge transaction

Bank of China checks its AED CBDC balance on the mBL. If it holds sufficient AED CBDC, it proceeds. If not, it arranges an FX swap on the mBridge platform to acquire AED CBDC from its CNY CBDC holdings. (In practice, commercial banks maintain pre-positioned CBDC balances in the currencies their clients frequently transact in.)

Step 3 — The payment instruction is submitted to the mBL

Bank of China submits the payment transaction to the mBridge ledger — specifying the AED CBDC amount, the destination wallet (Emirates NBD’s mBL wallet), and the associated payment reference data.

Step 4 — Central bank validation (if required by protocol)

Depending on the transaction size and type, the mBL protocol may route the transaction through a central bank validation step — a confirmation from the PBoC and/or CBUAE that the transaction is compliant with applicable regulations. This step is designed to give central banks the supervisory oversight they require over large transactions.

Step 5 — Settlement executes on the mBL

The mBL executes the transaction. Bank of China’s AED CBDC wallet is debited by AED 5,000,000. Emirates NBD’s AED CBDC wallet is credited by AED 5,000,000. The transaction is recorded permanently on the mBridge ledger. Settlement is final.

Step 6 — Emirates NBD credits Emirates Technology Corp

Emirates NBD receives the AED CBDC credit on mBL. It then credits Emirates Technology Corp’s AED account in its core banking system via a local instruction. Emirates Technology Corp sees the funds in their account.

Step 7 — Reporting and reconciliation

Both Bank of China and Emirates NBD generate payment confirmations. The mBL transaction hash serves as the settlement reference. Both banks can provide their corporate clients with confirmation of settled payment — referencing on-ledger settlement data.

Total elapsed time: Under 10 seconds for Steps 3–6. The entire settlement — from payment submission on mBridge to Emirates NBD receiving final funds — is measured in seconds, not days.

No US correspondent. No SWIFT correspondent chain. No FX margin hidden in a multi-hop conversion. No 1–3 day wait.

Section 6: The Pilot Milestones — What Has Actually Happened on mBridge

mBridge is not a white paper. It has progressed through defined development stages with real transaction volumes. This track record is what distinguishes mBridge from dozens of other blockchain payment projects that never left the pilot phase.

Phase 1 — Proof of Concept (2021)

The initial Proof of Concept demonstrated that the core technical premise was feasible: multiple central banks could issue digital currencies onto a shared platform and conduct cross-currency transactions. No live currency. No real value at risk. A technical demonstration.

Key finding: The mBL could achieve transaction throughput and finality characteristics suitable for interbank settlement use cases.

Phase 2 — Pilot (2022)

The pilot phase brought in real value for the first time. Over six weeks, 20 commercial banks from Hong Kong, China, UAE, and Thailand participated. Real-value transactions were executed on the platform.

Published results:

- Over 160 transactions executed

- Over HKD 22 million in total value settled across the participating currencies (HKD, CNY, AED, THB)

- Transaction types included: cross-border payments, FX spot transactions, FX swap transactions

This was the first time multiple central banks had successfully settled real cross-currency transactions on a shared CBDC platform. It was a landmark moment in the history of payment infrastructure.

Phase 3 — Minimum Viable Product / MVP (2024)

In June 2024, the BIS announced that mBridge had reached Minimum Viable Product (MVP) stage — the most significant milestone in the platform’s development. MVP means the platform is sufficiently stable, functional, and governed for real commercial use at scale by participating institutions.

At MVP stage:

- The platform is open to new central bank members and commercial bank participants

- Saudi Arabia’s SAMA joined as a full central bank participant

- The governance framework was formalised

- Commercial banks from the four original jurisdictions began operating on the platform in earnest

The MVP announcement was accompanied by a critical statement from the BIS: mBridge would not become a tool for sanctions circumvention, and the BIS would maintain governance standards aligned with international AML/CFT frameworks. This was a direct acknowledgment of the geopolitical sensitivities around the platform.

Ongoing Development (2025)

As of 2025, mBridge is in production operation with a growing participant base. The BIS Innovation Hub continues to publish technical updates. New central bank observers are joining regularly.

Section 7: mBridge vs SWIFT — A Direct Comparison

For payments professionals, this is the comparison that matters most. mBridge is not trying to compete with SWIFT on every dimension — but on the specific dimension of cross-border settlement, the contrast is stark.

| Dimension | SWIFT (Correspondent Banking) | mBridge |

| What it carries | Payment instructions (messages) — not money itself | Sovereign digital money (CBDC) — actual settlement asset |

| Settlement model | Indirect — instructions flow through correspondent accounts | Direct — CBDC transfers between commercial bank wallets |

| Settlement time | 1–3 business days (typical cross-border) | Seconds |

| Settlement finality | Delayed — final only when all correspondent legs complete | Immediate — deterministic on mBL confirmation |

| Operating hours | Business hours, cut-off times apply | 24/7/365 |

| FX conversion | Embedded in correspondent chain (opaque margin) | Explicit atomic swap at agreed rate (transparent) |

| Counterparty risk | Herstatt risk exists between settlement legs | Eliminated — atomic swap, both legs simultaneous |

| Nostro/Vostro prefunding | Required — trillions in idle capital globally | Dramatically reduced — just-in-time liquidity possible |

| Correspondent banks required | Yes — typically 2–5 per cross-border payment | None — direct bank-to-bank settlement |

| Cost per transaction | $25–$75+ (correspondent fees + FX margin) | Near zero (platform fees, no correspondent markup) |

| Transparency | Limited — originator loses visibility at each hop | Full — all participants see transaction on shared ledger |

| Network participants | 11,000+ financial institutions globally | Currently: 5 central banks + supervised commercial banks |

| Currencies supported | 140+ currencies | HKD, CNY, AED, THB, SAR (growing) |

| Regulatory framework | SWIFT rulebook + national regulation | mBridge governance framework + national central bank oversight |

| Established since | 1973 | 2021 (pilot), 2024 (MVP) |

| Geographic reach | Global | Asia-Middle East corridors (expanding) |

The comparison reveals mBridge’s fundamental architectural superiority for settlement efficiency — and its current limitations in reach and maturity.

SWIFT’s advantage is its 50 years of network effects, global reach, regulatory embedding, and the operational trust that 11,000 institutions place in it daily. A bank in the Netherlands paying a supplier in Brazil is not waiting for mBridge. That transaction will use SWIFT correspondent rails for the foreseeable future.

mBridge’s advantage is in the specific corridors it covers: Asia-Middle East-Southeast Asia cross-currency trade settlement. In those corridors, for participating institutions, mBridge offers a settlement capability that SWIFT’s correspondent model structurally cannot match.

Section 8: Programmability — What mBridge Can Do That SWIFT Cannot

Beyond speed and cost, mBridge’s programmable ledger enables capabilities that are structurally impossible on SWIFT’s messaging model.

Conditional Payments and Smart Contract Settlement

Because mBridge is a programmable ledger, payment execution can be conditional — tied to the occurrence of an external event confirmed on the ledger.

Example — Trade Finance:

An importer in China and an exporter in the UAE agree to a documentary trade transaction. The exporter ships goods. The shipping company confirms delivery on the mBridge ledger (or via an oracle connected to it). At the moment of confirmed delivery, the payment — pre-committed in an escrow smart contract on the mBL — automatically releases to the exporter’s wallet.

No bank staff manually reviewing documents. No delay between document acceptance and payment release. No dispute about whether payment was made before or after delivery. The smart contract executes atomically — delivery confirmation and payment simultaneous.

This is a form of Delivery versus Payment (DvP) that removes the operational risk and manual processing that currently characterises trade finance. It is the application to commercial trade of the same principle that atomic swaps provide to FX settlement.

Liquidity Management Across Central Banks

mBridge’s shared ledger allows central banks to observe aggregate liquidity positions across the platform — something that is invisible in the correspondent banking model, where each bank’s position is known only to its correspondent.

This visibility enables more sophisticated liquidity management: central banks can offer intraday credit facilities on the mBL, commercial banks can optimise their CBDC holdings across currencies in real time, and the platform can support dynamic multilateral netting — where offsetting payments between multiple participants are netted before settlement, dramatically reducing the gross volume of CBDC that needs to change hands.

Cross-Border Securities Settlement

mBridge’s roadmap includes cross-border securities settlement — the ability to settle the purchase of a financial asset (tokenised bond, tokenised equity) against payment in CBDC, simultaneously, on the same platform. This is Delivery versus Payment (DvP) at the cross-border level — eliminating settlement risk in cross-border securities transactions in the same way atomic swaps eliminate it in FX.

Project Jura (a related BIS project) demonstrated this concept between France and Switzerland using tokenised financial instruments and wholesale CBDCs. As mBridge matures, integration of tokenised asset settlement is a natural extension.

Section 9: The Governance Model — Who Controls mBridge?

Governance is one of the most important and most underappreciated aspects of mBridge. A payment platform is only as trustworthy as its governance structure.

The BIS’s Role

The BIS provides the neutral, multilateral governance backbone. It is the convenor, the technical standard-setter, and the dispute arbitration reference point. No single country controls mBridge. No single commercial interest controls it. The BIS’s institutional neutrality — it is owned by 63 central banks — gives mBridge a legitimacy that a privately developed platform could not achieve.

Central Bank Governance Rights

Each participating central bank retains full sovereignty over its own CBDC on the platform. The HKMA decides how HKD CBDC is issued, redeemed, and governed. The PBoC decides the same for CNY CBDC. No central bank is forced to accept or process transactions it does not approve.

Each central bank also operates its own validation nodes on the mBL — meaning no single central bank can unilaterally alter the ledger. Changes to the mBridge protocol require consensus among participating central banks.

AML/CFT Compliance

This is an area of intense external scrutiny. Any platform that allows cross-border payments between China, the UAE, Saudi Arabia, and others without routing through SWIFT will attract questions about whether it can be used to circumvent sanctions.

The BIS has addressed this directly: mBridge operates with AML/CFT compliance as a foundational design requirement, not an afterthought. Each participating central bank enforces its own AML/CFT standards on the commercial banks in its jurisdiction using the platform. The platform’s shared ledger provides greater transaction visibility than the correspondent banking model — it is architecturally more transparent, not less.

Commercial banks participating in mBridge must be regulated and supervised by their national central bank. They must onboard their corporate clients with full KYC/AML due diligence. They must comply with sanctions obligations applicable in their jurisdiction.

The platform does not route around sanctions — it simply routes around correspondent banks. Those are not the same thing.

What Happens When Countries Disagree?

This is a legitimate architectural and governance concern. If a payment between a Chinese bank and a UAE bank involves a counterparty that one jurisdiction considers sanctioned and the other does not — what does the platform do?

The mBridge design gives each central bank a supervisory window into transactions touching their jurisdiction. A central bank can reject or block a transaction that violates its national regulatory obligations. The protocol does not force any central bank to process a transaction it considers non-compliant.

The detailed dispute resolution and cross-jurisdictional conflict protocol has not been fully publicly disclosed.

Section 10: Criticisms and Open Challenges

mBridge is one of the most promising cross-border payment infrastructure projects in decades. It also has real challenges — and a payments professional who does not understand them cannot fairly assess it.

Challenge 1: Limited Geographic Reach

mBridge currently covers four currency corridors: HKD, CNY, AED, and THB — with SAR now added. For the Asia-Middle East trade corridor, this is significant. For global payments, it is a narrow slice. A payment from Germany to Brazil, from the UK to Nigeria, or from the US to India does not benefit from mBridge in its current form.

Expanding to additional jurisdictions requires each new central bank to build CBDC infrastructure compatible with the mBL, establish governance relationships with existing participants, and navigate their own domestic regulatory approval for CBDC issuance. This is a multi-year process per jurisdiction.

Challenge 2: Commercial Bank Readiness

Participating in mBridge is not just about the central bank — the commercial banks that actually process trade payments need to build new technical capabilities. They need mBridge API integrations, CBDC wallet management infrastructure, real-time liquidity management tooling, and staff trained to operate in a CBDC settlement environment.

For large commercial banks with strong technology teams (HSBC, Emirates NBD, Bank of China), this is achievable. For smaller regional banks, the investment required may be a barrier.

Challenge 3: Liquidity Management in Multiple CBDCs

A commercial bank participating in mBridge must manage liquidity positions across multiple CBDCs simultaneously. If Bank A needs to process AED payments but its mBridge wallet is running low on AED CBDC, it needs a mechanism to acquire more — either by redeeming a CBDC with the issuing central bank (which takes time) or by conducting an FX swap on the platform (which requires a counterparty).

Intraday liquidity management across multiple CBDC positions is a new operational discipline. Banks have highly refined skills for managing nostro account liquidity. The equivalent CBDC liquidity management tools and practices are still being developed.

Challenge 4: Interoperability With Other CBDC Platforms

mBridge is not the only multi-CBDC project in development. Project Agorá (BIS, seven central banks including the US Federal Reserve, Bank of England, ECB) is exploring tokenised commercial bank deposits and wholesale CBDCs on a different model. Jasper-Ubin (Canada-Singapore) piloted a bilateral CBDC arrangement. Various bilateral CBDC experiments are in progress globally.

The risk is a fragmented landscape of incompatible CBDC platforms — each covering different corridors, using different technical standards, requiring separate integration from commercial banks. The BIS is working on interoperability standards, but the question of how mBridge connects to other emerging CBDC infrastructure is unresolved.

Challenge 5: Geopolitical Risk to the Platform Itself

The presence of the People’s Bank of China as a founding participant creates political complexity — particularly in the context of US-China tensions. Some Western banks and central banks have expressed hesitation about joining mBridge precisely because of the PBoC’s involvement. The platform’s perception in Washington, Brussels, and London matters to the commercial banks that operate under those regulators’ supervision.

The BIS has emphasised mBridge’s technical and multilateral nature. Whether that framing is sufficient to enable broad Western participation in the platform remains to be seen.

Section 11: What mBridge Means for Payments Professionals

For Payments Freshers — Understanding the Landscape

mBridge is the most important live example of what wholesale CBDC infrastructure looks like in practice. Understanding it gives you a concrete reference point for every discussion about “the future of cross-border payments.” When someone says “CBDC bridge” or “atomic settlement” or “nostro reduction,” you now have a real project to anchor those concepts to.

For Mid-Level Payments Professionals — The Practical Implications

If your bank operates in any of the mBridge currency corridors — HKD, CNY, AED, THB, SAR — the question of whether your institution will participate in mBridge, and when, is a live strategic question. The answers affect your correspondent banking relationships, your nostro management practices, and your client-facing cross-border payment capabilities.

If you work on payment operations, understand that mBridge settlement does not generate the traditional SWIFT confirmation messages your reconciliation systems are designed to process. It generates on-ledger transaction records. The reconciliation and operations workflow is fundamentally different — and your systems need to evolve.

For Solution Architects — The Design Implications

If you are architecting payment infrastructure for a bank in an mBridge-adjacent jurisdiction, consider three questions:

Question 1: Should this bank participate in mBridge?

Assess the bank’s exposure to the covered corridors. If a meaningful portion of their cross-border payment volume is in HKD, CNY, AED, THB, or SAR, the economics of mBridge participation — reduced correspondent fees, faster settlement, nostro efficiency — likely justify the investment in building the technical integration.

Question 2: How does mBridge integrate with the existing payment engine?

The payment engine receives ISO 20022 payment instructions from corporate clients (PAIN.001) and routes them for processing. For mBridge-eligible payments, the routing logic needs to identify eligible transactions (currency, counterparty bank participation status, transaction type) and route them to the mBridge API layer rather than the SWIFT gateway.

The settlement confirmation from mBridge (an on-ledger event) must be translated back into a PACS.002-equivalent status report for the upstream client notification. This translation layer — mBridge ledger event to ISO 20022 status message — is a key integration design challenge.

Question 3: How does CBDC liquidity management integrate with treasury systems?

The bank’s treasury management system (TMS) needs to track CBDC wallet balances across currencies in real time — exactly as it currently tracks nostro account balances. The difference: nostro balances are reported through account statements and SWIFT balance messages (CAMT.052, CAMT.053). mBridge CBDC balances are on-ledger — queryable in real time via API. The TMS integration requires new data feeds and potentially new liquidity optimisation models.

Section 12: The Bigger Picture — mBridge in the Architecture of Tomorrow

mBridge does not exist in isolation. It is the most advanced instantiation of a broader movement toward tokenised settlement infrastructure — where the assets being settled are not account entries on a correspondent’s ledger, but programmable tokens on a shared distributed platform.

The BIS’s Finternet vision — articulated by BIS General Manager Agustín Carstens — describes a future financial system of interconnected ledgers, each settling in tokenised central bank money, with atomic cross-ledger transactions enabling real-time, risk-free settlement of financial assets globally.

mBridge is the first real step toward that vision. It is not the destination — it is the proof of concept that the destination is buildable.

For payments professionals, the implication is clear: the skills that matter in this next era are not just ISO 20022 message mapping and SWIFT connectivity. They include understanding tokenised settlement mechanics, CBDC architecture, smart contract design, and the governance frameworks that enable sovereign institutions to share infrastructure.

The architects who understand both the traditional world — SWIFT, ISO 20022, correspondent banking, RTGS — and the emerging world — CBDC, atomic settlement, programmable money, DLT — will be the ones designing the infrastructure that handles the next fifty years of global trade.

Key Takeaways

- mBridge is a multi-central-bank digital currency settlement platform developed by the BIS Innovation Hub with the HKMA, PBoC, CBUAE, and Bank of Thailand — now including Saudi Arabia’s SAMA. It enables real-time, peer-to-peer cross-border payment and FX settlement using wholesale CBDCs.

- The platform eliminates the correspondent banking chain for covered corridors — removing the fees, delays, opacity, and pre-funded nostro requirements that make traditional cross-border settlement expensive and slow.

- Atomic swaps on the mBridge Ledger eliminate Herstatt risk at the protocol level — both legs of an FX transaction settle simultaneously, with zero window of counterparty default exposure.

- mBridge reached Minimum Viable Product (MVP) stage in June 2024 and is in production operation. The pilot phase settled over HKD 22 million in real transactions across 160+ trades.

- Governance is multilateral and BIS-anchored. Each central bank retains sovereignty over its own CBDC. AML/CFT compliance is a design requirement, not an afterthought.

- The challenges are real: limited geographic reach, commercial bank readiness requirements, multi-CBDC liquidity management complexity, interoperability with other CBDC platforms, and geopolitical perception.

- For solution architects: mBridge integration requires a routing layer in the payment engine (to identify mBridge-eligible transactions), an ISO 20022-to-mBL translation layer, and a new CBDC liquidity management integration with treasury systems.

- mBridge is not the end state — it is the first production proof that sovereign atomic settlement on shared distributed infrastructure works. The trajectory points toward a global network of interconnected tokenised settlement platforms.

Further Reading

For primary sources on mBridge, the BIS publishes comprehensive technical reports and progress updates at bis.org/mbridge. The BIS Annual Economic Report chapters on CBDCs and tokenised settlement provide the broader context in which mBridge sits. For the specific technical architecture of the mBridge Ledger, the BIS Innovation Hub’s working papers are the authoritative source.

For the adjacent landscape, the PaymentTalks articles on CBDCs and the Stablecoins Series provide the foundational context that makes mBridge’s significance fully legible.