A corporate treasurer at a mid-sized manufacturing firm needs to pay a supplier in the Philippines. $500,000 USD equivalent. The transfer goes out Monday through the company’s bank. It lands Wednesday. $45 disappears somewhere in the fee chain, and the exchange rate applied is not the one anyone saw on Google that morning. Three banks touch the payment on its way through. None of them can tell the treasurer exactly where the money sat at any given hour.

Every payments professional has watched a version of this play out. It is the daily reality of cross-border payments for millions of businesses, and it is the exact problem that stablecoins were built to solve.

Stablecoins have moved out of crypto forums and into the boardrooms of central banks, card networks, and tier-one banks. Whether you have been building payment engines for two decades or joined the industry last quarter, stablecoins are no longer optional reading. This is the first article in a five-part series that takes you from zero to stablecoin-fluent. Here, you get exactly what a stablecoin is, why it exists, how it differs from Bitcoin and from ordinary bank money, and what the three underlying models look like. No prior crypto background needed.

Why Should Payments Professionals Care About Stablecoins Right Now?

Because the infrastructure conversation has already moved on without waiting for permission. Central banks are piloting stablecoin settlement frameworks. Card networks are building stablecoin rails alongside their existing ones. Regulators in the US, EU, and UK have all published or are actively drafting stablecoin-specific rulebooks. If you sit anywhere near payment architecture, product, compliance, or operations, this is now a domain-knowledge gap you cannot afford, the same way ISO 20022 stopped being optional once SWIFT set its migration deadlines.

What Problem Are Stablecoins Actually Solving?

Understand the problem before you evaluate the solution. Stablecoins were not invented to chase a crypto trend. They exist to fix two separate, well-documented failures in how money moves.

Problem 1: Correspondent Banking Is Slow, Expensive, and Opaque

Global payments infrastructure was largely built in the 1970s. SWIFT was founded in 1973, and correspondent banking, where banks route international payments through intermediary banks holding nostro and vostro accounts with each other, has been the dominant model ever since.

The model works. It is also expensive, slow, and opaque by design. A payment from the UK to the Philippines typically passes through three to five banks, takes one to three business days, costs $25 to $50 in fees, and loses visibility the moment it leaves the originating bank. Scale that friction across a $190 trillion annual cross-border payments market and you are looking at hundreds of billions in wasted cost and trapped liquidity.

Problem 2: Existing Cryptocurrencies Are Too Volatile for Commerce

Bitcoin arrived in 2009 with a genuinely radical premise: a peer-to-peer electronic cash system with no banks, no borders, no intermediaries. On paper, it looked like the cross-border payments fix the industry needed.

In practice, it had a fatal flaw for commercial use. Invoice a client for $10,000 worth of goods, get paid in Bitcoin on Monday, and by the time you convert it Thursday the price has moved 15% in either direction. Move against you and your margin is gone. Move in your favour and your supplier, expecting exactly $10,000 in their local currency, is now carrying your currency risk. Bitcoin can swing 10 to 30% in a single day. That is not a payment mechanism. That is speculation wearing a payment mechanism’s clothes.

Stablecoins set out to fix both problems at once: keep the speed, the programmability, and the borderless settlement of cryptocurrency, and strip out the price volatility.

So What Exactly Is a Stablecoin?

A stablecoin is a cryptocurrency whose value is pegged to a reference asset, most commonly a fiat currency like the US Dollar or Euro, occasionally a commodity like gold.

The most common peg is 1:1 with the US Dollar:

- 1 USDC (USD Coin) = $1.00

- 1 USDT (Tether) = $1.00

- 1 EURC (Euro Coin) = €1.00

Where Bitcoin’s price floats entirely on market supply and demand, a stablecoin’s value is held in place by a stabilisation mechanism, typically a reserve of real-world assets backing every token in circulation.

Think of a stablecoin as a digital dollar (or euro, or pound) that lives on a blockchain.

It moves at cryptocurrency speed, settling in seconds, 24 hours a day, 7 days a week, at minimal cost. It holds value like fiat currency. That combination is what makes it genuinely useful as a payment instrument rather than a speculative asset.

How Is a Stablecoin Different From Bitcoin and Ether?

This is one of the most common points of confusion in the market. People hear “stablecoin,” assume it is just another flavour of Bitcoin, and stop there. The two are fundamentally different products.

| Feature | Bitcoin / Ether | Stablecoin (e.g. USDC) |

| Price | Volatile, can swing 10-30% daily | Stable, pegged to reference asset |

| Primary use | Store of value, speculation, investment | Payments, settlement, treasury management |

| Who controls supply | Decentralised protocol, no issuer | Usually a centralised issuer (e.g. Circle) |

| What backs it | Market confidence and scarcity | Fiat reserves, assets, or algorithms |

| Reversibility | Irreversible on-chain | Irreversible on-chain (same) |

| Settlement speed | Minutes to hours (Bitcoin) | Seconds (Solana), seconds to minutes (Ethereum) |

| Regulatory status | Property/commodity in most jurisdictions | Increasingly regulated as e-money or payment instrument |

The distinction that matters for architects: Bitcoin was designed as a store of value and a speculative asset. Stablecoins are designed as a payment instrument. Different products, solving different problems, evaluated against different criteria.

How Is a Stablecoin Different From Money Sitting in a Bank Account?

The other comparison that actually matters. If a stablecoin is pegged 1:1 to the dollar, why not just move dollars through a bank directly? Fair question, and the practical answer is in the operating mechanics, not the peg.

| Feature | Bank Transfer (e.g. SWIFT wire) | Stablecoin Transfer |

| Settlement time | 1-3 business days | Seconds |

| Operating hours | Business hours, weekdays | 24/7/365 |

| Cross-border fees | $25-$50+ per transaction | Under $1, often under $0.01 |

| Programmability | Limited, instructions only | High, smart contract automation |

| Transparency | Opaque once in the correspondent chain | Full on-chain visibility |

| Counterparty | Bank intermediaries required | Direct wallet-to-wallet possible |

| Minimum amount | Often $1,000+ economical | Fractions of a cent |

| Reversibility | Possible, with difficulty | Generally irreversible |

Stablecoins are not a bank account replacement. For specific use cases, particularly cross-border payments, treasury sweeps, and 24/7 settlement, they offer capabilities correspondent banking simply cannot match on current rails.

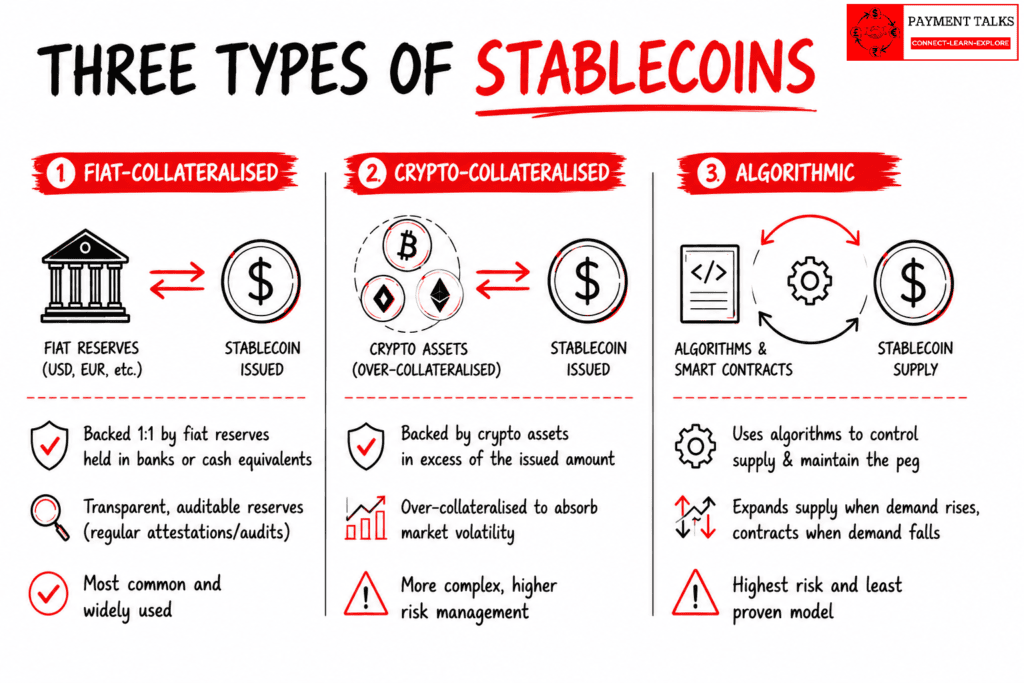

What Are the Three Types of Stablecoins?

Not every stablecoin works the same way underneath. There are three fundamental models, and the difference between them is not academic. The model determines the risk profile, the regulatory treatment, and whether it belongs anywhere near an enterprise payment system.

Type 1: Fiat-Collateralised Stablecoins

The simplest and most widely used model. For every stablecoin in circulation, the issuer holds an equivalent amount of real-world fiat currency in a regulated bank account, or close equivalents like short-dated government bonds.

How it works: a company deposits $1 million with the issuer. The issuer mints 1 million tokens. The company spends those tokens. When it wants dollars back, it redeems the tokens, the issuer burns them, and releases the $1 million. The backing never leaves. One token, one dollar in reserve, always.

- Examples: USDC (Circle), USDT (Tether), EURC (Circle), FDUSD (First Digital)

- Strengths: simplest model to understand, most transparent, most widely accepted by regulators, easiest to integrate into an enterprise payment stack.

- Weaknesses: centralised. The issuer can freeze addresses, sits exposed to regulatory pressure, and the model requires trust in the issuer’s reserve management. If the issuer fails, the peg fails with it.

- Best for: enterprise payments, cross-border B2B, treasury operations, regulated financial use cases.

Type 2: Crypto-Collateralised Stablecoins

Backed by other cryptocurrencies instead of fiat. Because crypto collateral is itself volatile, these systems require over-collateralisation: you lock up more value than you mint.

How it works: to mint $100 of DAI, a user locks $150 of ETH into a smart contract. If ETH drops, the system automatically liquidates collateral to protect the peg. If ETH drops fast enough that collateral cannot cover it, additional backstops kick in. The 150%-plus over-collateralisation is the buffer that absorbs crypto volatility without the stablecoin itself moving.

- Examples: DAI (MakerDAO), LUSD (Liquity)

- Strengths: decentralised, no single point of failure, no central party that can freeze an address, fully verifiable on-chain.

- Weaknesses: capital-inefficient, since $150 is tied up to release $100. Complex, and vulnerable in a fast crash where collateral value falls faster than liquidation mechanisms can respond.

- Best for: DeFi applications and protocols that structurally cannot rely on a centralised issuer.

Type 3: Algorithmic Stablecoins

An attempt to hold the peg with no collateral at all, fiat or crypto. An algorithm expands or contracts token supply to control price instead.

How it works: price rises above $1.00, the algorithm mints more tokens to push it back down. Price falls below $1.00, the algorithm burns tokens to push it back up. Some designs use a companion token to absorb volatility, minting it to buy back the stablecoin when confidence wobbles. Elegant in theory. Catastrophic in practice, more than once.

The TerraUST collapse, May 2022: TerraUST (UST) was the largest algorithmic stablecoin by market capitalisation, worth over $18 billion at its peak, held up by a companion token called LUNA. Coordinated selling pressure broke the peg. The algorithm minted enormous quantities of LUNA to defend it. LUNA’s price crashed as supply exploded. Confidence collapsed. UST went to near zero. Over $40 billion in value was wiped out in roughly 72 hours.

TerraUST remains the reference event for stablecoin risk. It proved that algorithmic mechanisms without real collateral can unwind under coordinated attack or a simple loss of confidence, with no floor underneath.

- Examples: TerraUST (collapsed), FRAX (partially collateralised hybrid)

- Regulatory direction: the US, EU, and UK are all restricting or prohibiting pure algorithmic stablecoins for payment use. The GENIUS Act in the US imposed a two-year study moratorium. MiCA in the EU carries strict conditions. Do not recommend an algorithmic stablecoin for any regulated payment system. That is not caution, that is the current regulatory reality.

Visual 1: Three Types of Stablecoins compared

Which Stablecoins Will You Actually See in Payments Work?

Strip away the long tail and enterprise payments work concentrates around a short list.

| Stablecoin | Full Name | Issuer | Peg | Primary Backing | Key Markets |

| USDC | USD Coin | Circle (+ Coinbase) | 1:1 USD | Cash + US T-Bills | Global, preferred for regulated use |

| USDT | Tether | Tether Ltd | 1:1 USD | Mixed reserves | Global, highest volume |

| EURC | Euro Coin | Circle | 1:1 EUR | Cash + Euro reserves | European corridors |

| DAI | DAI | MakerDAO | ~1:1 USD | Over-collateralised crypto | DeFi, decentralised platforms |

| FDUSD | First Digital USD | First Digital | 1:1 USD | Cash + T-Bills | Asia-Pacific |

| PYUSD | PayPal USD | PayPal / Paxos | 1:1 USD | Cash + T-Bills | Consumer payments |

For regulated enterprise use, USDC is generally the benchmark: the clearest reserve structure, the most rigorous attestation process, and the deepest regulatory engagement globally of any fiat-backed stablecoin on the market today.

A Simple Mental Model: The Traveller’s Cheque, Rebuilt for the Blockchain

If you want one image to anchor this, picture a stablecoin as a modern, programmable traveller’s cheque, one that works everywhere, costs almost nothing to use, and clears in seconds instead of days.

Buy a traveller’s cheque in 1995 and you hand American Express your dollars. They hand you a paper instrument representing those dollars, redeemable anywhere in the world. The dollar sits behind it the whole time. The instrument is just a portable, usable form of it.

A stablecoin runs on the same logic. Hand Circle your dollars, they hand you USDC, a digital instrument representing those dollars, redeemable on demand. Swap paper for blockchain, and swap days at a foreign bank counter for seconds, anywhere in the world. The traveller’s cheque solved a 1990s problem: carrying cash across a border safely. The stablecoin solves a 2020s problem: moving value across a border quickly, cheaply, and programmably.

How Do Stablecoins Fit Into the ISO 20022 World?

Here is the piece most crypto-native explainers skip entirely, and the piece that matters most if you actually build payment systems for a living. Stablecoins do not exist in a parallel universe from ISO 20022. The messaging standard the industry has spent a decade migrating onto for SWIFT, SEPA, and domestic RTGS systems is increasingly the same standard being used to originate and reconcile stablecoin-based flows at the banking layer.

A corporate still originates a payment instruction the same way, often still a PAIN.001 message. What changes is what happens after the instruction leaves the originating institution: instead of a chain of correspondent banks passing PACS.008 messages hand to hand, a stablecoin rail can settle the value leg on-chain in seconds while ISO 20022 messaging still carries the structured remittance, compliance, and reconciliation data around it. The rail changes. The data discipline does not.

This is worth its own deep dive, and gets one: see Stablecoins & ISO 20022: The New Architecture of Cross-Border Payments for the full mapping between the two worlds.

What Do Payments Professionals Get Wrong About Stablecoins?

“Stablecoins are just crypto, too risky for real finance.”

Fiat-backed stablecoins like USDC are regulated, attested, and backed 1:1 by cash and government securities. The European Central Bank, the US Federal Reserve, and the Bank of England are all actively studying or piloting stablecoin frameworks. The risk profile of USDC has nothing in common with Bitcoin, and even less in common with TerraUST.

“If it’s digital money, isn’t it the same as a bank deposit?”

Not quite, and this is where a lot of risk teams stumble. Bank deposits are liabilities of the bank, covered by deposit insurance schemes such as FDIC in the US or FSCS in the UK, up to defined limits. Stablecoins are liabilities of the issuer, for example Circle, and the regulatory treatment of that liability differs by jurisdiction. The protection mechanisms are not interchangeable. This distinction also separates stablecoins from CBDCs, which are direct central bank liabilities rather than issuer liabilities. Getting this wrong in a risk-weighting model is a real, recurring mistake.

“Stablecoins are anonymous, they can’t meet AML requirements.”

A common misconception, particularly among compliance teams evaluating this for the first time. Fiat-backed stablecoins issued by regulated entities carry mandatory KYC/AML onboarding for institutional access. USDC, for instance, can only be minted through Circle’s regulated onboarding flow. The FATF Travel Rule applies to Virtual Asset Service Providers handling stablecoins, requiring originator and beneficiary data to travel with the transaction, structurally not far off how SWIFT messaging already carries that data today.

“The stablecoin peg is guaranteed.”

No peg is mathematically guaranteed forever. A fiat-backed stablecoin is only as stable as its reserve management and its issuer’s solvency. USDC briefly traded at $0.87 in March 2023 when Silicon Valley Bank, where a portion of USDC’s reserves sat, failed. It recovered within 48 hours once Circle confirmed the exposure was limited. Design for peg monitoring and contingency routing as a first-class requirement, not an afterthought bolted on after an incident.

Key Takeaways

- A stablecoin is a cryptocurrency pegged to a reference asset, most commonly the US Dollar, combining blockchain speed and programmability with fiat-level price stability.

- Stablecoins exist to solve two problems: the volatility of existing cryptocurrencies and the slowness and cost of correspondent banking rails.

- There are three models: fiat-collateralised (most trusted for payments), crypto-collateralised (decentralised, capital-intensive), and algorithmic (high-risk, headed toward regulatory prohibition for payment use).

- USDC, USDT, and DAI are the three you will encounter most. For regulated enterprise payments, USDC is the current benchmark.

- A stablecoin is not a bank deposit, not Bitcoin, and not permanently guaranteed. The distinctions matter directly for compliance, risk, and architecture decisions.

- Regulators are actively building frameworks around this, not against it: MiCA in the EU, the GENIUS Act in the US, FCA regulation in the UK. Stablecoins are becoming part of the regulated financial system, not an escape hatch from it.

Frequently Asked Questions

Q: Is a stablecoin the same thing as a CBDC?

A: No. A stablecoin is issued by a private company (e.g. Circle, Tether) and is a liability of that issuer. A CBDC (Central Bank Digital Currency) is issued directly by a central bank and is a direct central bank liability. This article covers the full comparison.

Q: Which stablecoin should an enterprise payment system use by default?

A: For most regulated, enterprise cross-border use cases, USDC is currently the benchmark on reserve transparency and regulatory engagement. USDT carries the highest volume globally but a less transparent reserve mix.

Q: Can stablecoins meet AML and KYC requirements?

A: Yes, for regulated fiat-backed stablecoins. Minting requires institutional KYC/AML onboarding through the issuer, and the FATF Travel Rule requires originator and beneficiary data to travel with the transaction.

Q: What happens if a stablecoin de-pegs?

A: It depends on the model. Fiat-collateralised stablecoins have historically recovered from short de-peg events once reserve exposure was clarified, as USDC did in March 2023. Algorithmic stablecoins have no such backstop, as TerraUST demonstrated in 2022.

Q: Do stablecoins replace correspondent banking?

A: Not outright. They offer faster, cheaper settlement for specific corridors and use cases, but correspondent banking still handles the bulk of regulated, high-value cross-border flows today. This comparison breaks down where each model currently wins.

Q: Why does the ISO 20022 messaging standard still matter if stablecoins settle on-chain?

A: Because settlement and messaging are two different layers. Stablecoin rails can move the value leg on-chain while ISO 20022 messages such as PAIN.001 still carry the structured originator, beneficiary, and remittance data around that transfer.

What’s Next in This Series

You now understand what a stablecoin is and why it exists. Knowing what it is tells you nothing about how it actually works under the hood.

In Part 2: How Stablecoins Are Created and Destroyed, we go inside the engine room: how stablecoins are minted and burned, what actually sits inside the reserve, which blockchains carry stablecoin flows and why that choice matters, and the difference between custodial and non-custodial wallets.

From there, Part 3: Stablecoins vs Traditional Payment Rails walks the same payment down both rails side by side.

If you are serious about payments architecture, the next article is where theory becomes mechanics.