The Question Every Payments Professional Is Asking

A colleague stops you in the corridor. “We just got a briefing from the central bank. They want us to assess readiness for a retail CBDC pilot.” You nod confidently. But on the way back to your desk, the question surfaces: is a CBDC just a stablecoin issued by a government? What is actually different?

You are not alone. The confusion between Central Bank Digital Currencies (CBDCs) and stablecoins is one of the most common conceptual blurs in the payments industry right now. Both are digital. Both are pegged to fiat currencies. Both live on some form of distributed or centralised ledger. On the surface, they look similar.

Underneath, they are fundamentally different — in who issues them, who bears the risk, how they are settled, and what role they play in the monetary system. Getting this distinction wrong has real consequences. It affects how you design payment architectures, how you advise clients, how you assess regulatory obligations, and how you communicate with central banks, commercial banks, and corporate treasurers.

This article gives you the complete picture. By the end, you will understand what CBDCs are, how they work at a technical and operational level, and exactly where they converge with and diverge from stablecoins — backed by real-world examples, live projects, and a practical comparison that you can use immediately.

Section 1: What Is a CBDC?

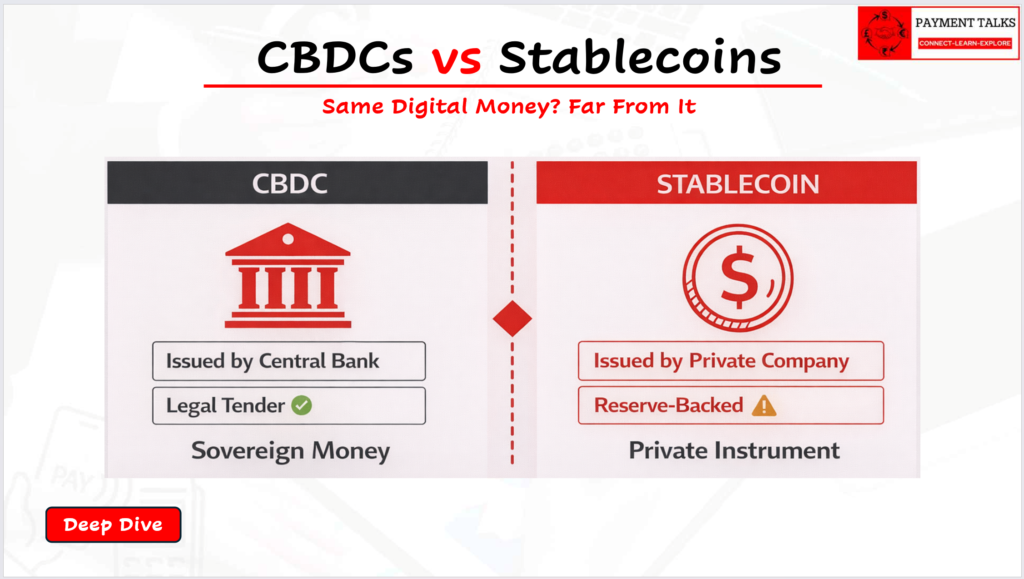

A Central Bank Digital Currency (CBDC) is a digital form of a country’s sovereign currency, issued and backed directly by the country’s central bank.

Let that definition settle for a moment, because every word in it matters.

Digital form: It is not physical cash. It is a digital representation of money — but unlike the digital money that already exists in your bank account, it has specific properties that make it structurally different.

Sovereign currency: It carries the same legal tender status as banknotes and coins. If a country has a retail CBDC, a shop that accepts cash is legally required to accept the CBDC as well — because it is the same money in a different form.

Issued and backed directly by the central bank: This is the defining characteristic. A CBDC is a direct liability of the central bank — not a commercial bank, not a private issuer, not an algorithm. The same institution that issues banknotes issues the CBDC.

The simplest analogy: a CBDC is a digital banknote. Just as a physical £20 note is a direct claim on the Bank of England, a digital £20 CBDC is a direct claim on the Bank of England. The trust anchor is the sovereign state — the same entity that controls monetary policy, manages the money supply, and acts as the lender of last resort.

Section 2: Why Are Central Banks Building CBDCs?

Central banks do not move quickly. When over 130 central banks — representing more than 98% of global GDP — are actively researching or developing CBDCs, something significant is driving it. There are five core motivations.

Motivation 1: The Declining Use of Cash

Physical cash is in structural decline in most developed economies. In Sweden, cash now accounts for less than 10% of transactions. In the UK, contactless payments overtook cash payments for the first time in 2022. In China, digital wallets handle the vast majority of consumer transactions.

If cash disappears entirely, citizens lose direct access to central bank money. Every digital payment would be intermediated by a commercial bank — subject to that bank’s solvency, policies, and fees. A retail CBDC preserves the public’s access to a risk-free, government-backed form of money in a cashless world.

Motivation 2: Financial Inclusion

Globally, approximately 1.4 billion adults remain unbanked — they have no access to a bank account. Many of them live in jurisdictions where mobile phones are ubiquitous but banking infrastructure is thin. A CBDC accessible via a smartphone app (or even an offline card) could give these individuals access to safe, government-backed money without requiring a bank account.

This is a central motivation for CBDCs in Sub-Saharan Africa, Southeast Asia, and parts of Latin America. Nigeria’s eNaira was explicitly designed with financial inclusion as a primary objective.

Motivation 3: Payment System Efficiency and Competition

Commercial banks and private payment networks have historically controlled the payments infrastructure. A CBDC can introduce competition, reduce fees, improve interoperability, and enable innovation — all while the central bank retains oversight of systemic risk.

For cross-border payments specifically, bilateral or multilateral CBDC arrangements (like mBridge, which we introduced in the Stablecoins Series already and will cover separately) can eliminate correspondent banking chains — reducing cost and settlement time dramatically.

Motivation 4: Monetary Policy Transmission

CBDCs open new possibilities for monetary policy. A central bank could, in theory, apply programmable interest rates directly to CBDC holdings — stimulating spending by applying negative rates on idle balances, or encouraging saving by applying positive rates. It could implement targeted fiscal stimulus — distributing digital money directly to citizens’ CBDC wallets without the friction of banking infrastructure.

These capabilities are theoretically possible. Whether they should be implemented raises significant economic and privacy debates. But they are part of why central banks are interested.

Motivation 5: Countering Private Digital Currencies and Foreign CBDCs

Meta’s Libra project (2019) — a global stablecoin backed by a basket of fiat currencies — alarmed central banks worldwide. The prospect of a private company issuing a global digital currency that could compete with sovereign money accelerated CBDC development significantly. Similarly, China’s digital yuan (e-CNY) has created strategic urgency in the US, EU, and UK to develop competing state-backed digital currency infrastructure.

Section 3: The Two Types of CBDC — Retail and Wholesale

This is the most important structural distinction in the CBDC landscape. Retail and wholesale CBDCs serve completely different purposes, involve different participants, and have different architectural implications.

Retail CBDC

A retail CBDC is a digital currency available directly to the general public — individuals and businesses. It is the digital equivalent of banknotes in your wallet.

Who holds it: Every citizen, every business. The end consumer.

How it works: A citizen opens a CBDC wallet (via the central bank’s app, or through a licensed commercial bank acting as a distribution intermediary). They can receive wages in CBDC, pay at shops, transfer to other citizens, and hold CBDC as a savings instrument.

Who it replaces (or supplements): Physical cash. Potentially also commercial bank deposits, though most central banks are designing holding limits to prevent this (more on this later).

Live examples:

- Digital Yuan / e-CNY (China): The most advanced retail CBDC deployment globally. Live in over 26 cities. Used for retail payments, government subsidies, and event payments (2022 Beijing Winter Olympics). Processed over ¥1.8 trillion (~$250 billion) in transactions as of 2023.

- eNaira (Nigeria): Africa’s first CBDC. Launched October 2021. Designed for financial inclusion — targeting the unbanked population.

- DCash (Eastern Caribbean Currency Union): A retail CBDC serving eight island nations. One of the first multi-country retail CBDCs.

- Sand Dollar (Bahamas): The world’s first nationally deployed retail CBDC. Live since October 2020.

Wholesale CBDC

A wholesale CBDC is a digital currency available only to financial institutions — commercial banks, central banks, clearing houses, and other regulated entities. It is not accessible to the general public.

Who holds it: Banks and financial institutions only.

How it works: Commercial banks hold accounts at the central bank (called reserve accounts). Currently, these accounts are digital — but they operate on centralised, proprietary central bank ledger systems. A wholesale CBDC moves this infrastructure to a programmable, distributed ledger — enabling atomic settlement, smart contract automation, and interoperability with tokenised asset markets.

Who it replaces: Existing wholesale settlement systems — Fedwire (US), CHAPS (UK), TARGET2 (EU), RTGS systems globally.

Live examples and pilots:

- mBridge (BIS Innovation Hub, HKMA, PBoC, CBUAE, Bank of Thailand): Multi-CBDC platform for cross-border wholesale settlement. Entered Minimum Viable Product (MVP) stage in 2024 with real commercial transaction volumes.

- Project Jura (BIS, Banque de France, Swiss National Bank): Tested cross-border settlement of tokenised financial assets using wholesale CBDCs.

- Project Rosalind (BIS, Bank of England): Explored API architectures for a retail CBDC.

- Digital Euro (ECB): In preparation phase. Wholesale pilot running alongside retail design work.

- FedNow + Digital Dollar exploration (US Federal Reserve): While FedNow is an instant payment rail (not a CBDC), the Federal Reserve is separately researching a potential digital dollar. No formal commitment to launch as of 2025.

Section 4: How a CBDC Works — The Technical Architecture

CBDCs do not all work the same way. Central banks have significant design flexibility. Here are the key architectural decisions every payments professional needs to understand.

Design Decision 1: Centralised vs Distributed Ledger

A CBDC can run on a centralised ledger — a database managed directly by the central bank — or on a distributed ledger — a shared ledger maintained by multiple nodes, potentially using blockchain technology.

Centralised ledger: The central bank runs the database. It records all CBDC balances and transactions. Commercial banks and wallets interact with it via APIs. This is architecturally similar to how existing RTGS systems work — just modernised and made accessible to a broader set of participants. The Bank of England’s digital pound design leans toward this model.

Distributed ledger (DLT/blockchain): A permissioned blockchain shared between the central bank and selected participants (commercial banks, technology providers). The central bank retains authority over the ledger but shares validation with trusted nodes. China’s e-CNY uses a two-tier architecture with some distributed elements. The mBridge platform uses a permissioned blockchain purpose-built for multi-CBDC settlement.

Most retail CBDCs are trending toward centralised or hybrid architectures — prioritising scalability, transaction speed, and central bank control over the pure decentralisation philosophy of public blockchains.

Most wholesale CBDC projects are exploring permissioned DLT architectures — because the benefits of programmability, atomic settlement, and interoperability are more readily achievable on DLT, and the participant set is small and fully regulated.

Design Decision 2: Account-Based vs Token-Based

Account-based CBDC: The balance is held in an account linked to an identity. Spending is authenticated by proving you are the account holder (like a bank account with a PIN or biometrics). Transaction records reference the payer and payee directly.

Token-based CBDC: The balance is held in a cryptographic token. Possession of the token’s private key proves ownership. Transactions work by transferring the token. This is more analogous to physical cash — and enables greater privacy.

Most retail CBDC designs are account-based at the institutional level but may offer token-based functionality for offline or privacy-preserving use cases. The ECB’s digital euro design includes a privacy tier where small payments below a threshold are not individually traceable.

Design Decision 3: Direct vs Indirect (Two-Tier) Issuance

Direct model: The central bank issues CBDC directly to citizens. Citizens hold accounts at the central bank. The central bank handles onboarding, customer service, and transaction processing. Very few central banks are pursuing this — it would represent a massive operational undertaking and would disintermediate commercial banks entirely.

Indirect (Two-Tier) model: The central bank issues CBDC to commercial banks. Commercial banks distribute CBDC to their customers and handle the customer-facing infrastructure. The central bank remains the issuer and the liability sits on its balance sheet — but the distribution and servicing is handled by the commercial banking layer. This is the model most central banks are pursuing, including the digital pound (UK), digital euro (EU), and e-CNY (China).

This two-tier model is critical for payments architects: it means commercial banks play a central role in CBDC distribution and need to build CBDC-compatible infrastructure — wallets, APIs, onboarding flows, and compliance controls.

Design Decision 4: Programmability

A CBDC on a programmable ledger can have smart contract logic embedded — rules that govern how the currency can be used.

Examples of programmability in CBDC design:

- Earmarking: Government stimulus money that can only be spent on food, rent, or utilities (used for pandemic relief in China)

- Expiry: CBDC balances that expire after a set period, forcing spending and stimulating economic activity

- Conditional release: Payment that only settles when a delivery condition is confirmed (useful for trade finance and supply chain payments)

- Interest accrual: Positive or negative interest rates applied automatically to CBDC holdings

Programmability is powerful — and controversial. Civil liberties advocates raise significant concerns about governments having the technical ability to control how citizens spend their money. Most Western central banks are moving cautiously, emphasising privacy and limiting programmability to specific use cases.

Section 5: Real-World CBDC Scenarios

Scenario 1 — Retail CBDC (Consumer Payment)

Location: China. Citizen: Zhang Wei, a retail worker in Shanghai.

Zhang Wei receives her monthly salary of ¥8,000 in e-CNY, transferred directly to her digital yuan wallet by her employer. She uses the PBOC-issued app to pay for groceries at a nearby supermarket — the merchant’s point-of-sale terminal accepts e-CNY via QR code. The transaction settles instantly. No bank intermediary is involved. The settlement is final on the central bank’s ledger.

She also transfers ¥2,000 to her mother in rural Shandong. The transfer is instant, free, and works even though her mother has no bank account — just a feature phone with the e-CNY app.

What this demonstrates:

- Peer-to-peer transfer without a commercial bank

- Financial inclusion for the unbanked

- Real-time, 24/7 settlement at zero cost

- Direct claim on the People’s Bank of China — not on a commercial bank

Scenario 2 — Wholesale CBDC (Cross-Border Interbank Settlement)

Participants: Emirates NBD (UAE) and Siam Commercial Bank (Thailand). Platform: mBridge.

Emirates NBD needs to send $10 million to Siam Commercial Bank in settlement of a trade finance transaction. Traditionally: SWIFT message, correspondent bank in USD, 1–2 day settlement, fees.

On mBridge:

- Emirates NBD submits the payment instruction to the mBridge platform

- The CBUAE (Central Bank of UAE) issues tokenised dirham (AED CBDC) onto the mBridge ledger equivalent to $10M

- An atomic swap executes on the mBridge DLT: AED CBDC is exchanged for Thai Baht CBDC simultaneously

- Siam Commercial Bank’s account on the mBridge ledger is credited with THB CBDC

- The Bank of Thailand’s systems register the settlement

- The entire transaction is final in seconds

No correspondent bank. No SWIFT message. No 1–2 day wait. Settlement certainty from the moment the atomic swap executes.

What this demonstrates:

- Wholesale CBDC eliminating the correspondent chain

- Atomic settlement removing Herstatt risk (counterparty default before settlement)

- Real-time cross-border settlement at institutional scale

Section 6: CBDCs vs Stablecoins — The Complete Comparison

This is where many professionals get confused. The table below maps every meaningful dimension of difference.

| Dimension | CBDC | Stablecoin (Fiat-Backed, e.g. USDC) |

| Issuer | Central bank (sovereign institution) | Private company (e.g. Circle, Tether Ltd) |

| Liability of | Central bank — the state | Private issuer — a commercial entity |

| Backing | Full faith and credit of the sovereign state | Reserves (cash, T-Bills) held by private issuer |

| Legal tender status | Yes — legally mandated for acceptance | No — acceptance is contractual |

| Regulatory status | Sovereign money — above regulation | Regulated as e-money / payment instrument (MiCA, GENIUS Act) |

| Insolvency risk | Effectively zero (a state cannot default on its own currency) | Issuer insolvency risk exists (mitigated by reserve quality) |

| Who can hold it | Retail CBDC: general public. Wholesale CBDC: financial institutions | Anyone with a qualifying wallet and KYC approval |

| Peg mechanism | IS the sovereign currency — no peg mechanism needed | External mechanism: reserves + mint/burn cycle |

| De-peg risk | None (it is the reference currency itself) | Yes — reserve failure, bank run, issuer insolvency |

| Programmability | Possible (central bank decides) | Yes — smart contract logic (e.g. blacklisting) |

| Privacy | Determined by central bank design (major policy debate) | Pseudonymous on public chains; custodial platforms know user identity |

| Interest bearing | Possible by design (most current designs: non-interest bearing) | No inherent interest — yield only through DeFi lending |

| AML/KYC | Mandatory — embedded in CBDC architecture | Mandatory for regulated issuers and VASPs |

| Cross-border use | Limited — bilateral/multilateral arrangements required (mBridge) | Immediate — transferable to any wallet globally |

| Monetary policy tool | Yes — directly controlled by central bank | No — supply determined by commercial demand |

| Current availability | Live in ~11 jurisdictions, piloting in 60+ | Globally available in all jurisdictions permitting crypto |

| Settlement finality | On the central bank ledger — ultimate finality | Blockchain finality (varies by chain: seconds to minutes) |

| Interoperability | Limited — each CBDC is jurisdiction-specific | High — USDC operates on 10+ blockchains globally |

Section 7: The Trust Architecture — The Deepest Difference

The table above shows the surface differences. But the deepest difference between a CBDC and a stablecoin is the trust architecture — who you are ultimately trusting, and what happens when that trust is challenged.

Who Backs the Money?

When you hold USDC, you are trusting:

- Circle (the issuer) to hold genuine, fully reserved USD and T-Bills

- The banks holding those reserves to remain solvent

- The smart contract to execute correctly

- Regulators to enforce Circle’s compliance obligations

Every one of these trust dependencies is with a private actor. The US government does not guarantee USDC. If Circle failed, USDC holders would be creditors of a bankrupt company.

When you hold a retail CBDC (e.g. digital pound), you are trusting:

- The Bank of England — an institution that cannot go insolvent in its own currency, because it issues the currency itself

- No banks, no private issuers, no smart contracts for the core liability

The risk profile is categorically different. A CBDC is as safe as sovereign money — because it is sovereign money. A stablecoin is as safe as its private issuer and its reserves — which is substantially safe for USDC but not the same thing.

The March 2023 Illustration

When Silicon Valley Bank failed in March 2023, USDC briefly de-pegged to $0.87 because Circle held reserves there. In the same moment, central bank reserves held in the Federal Reserve were entirely unaffected. No CBDC would have de-pegged — because a CBDC’s value is not contingent on any commercial bank’s solvency.

This is not a criticism of USDC — it recovered fully and Circle’s reserve design has since been strengthened. It is an illustration of a structural difference in the trust architecture.

Section 8: Where CBDCs and Stablecoins Intersect

The relationship between CBDCs and stablecoins is not purely adversarial. In several important scenarios, they complement each other.

Intersection 1: CBDC as the Settlement Asset for Stablecoin Systems

In a mature digital money ecosystem, stablecoins could continue to operate as the programmable, consumer-facing layer — while wholesale CBDCs provide the interbank settlement infrastructure underneath. A stablecoin transfer between two major exchanges could settle net positions using wholesale CBDC at the end of the day — combining the flexibility of stablecoins with the finality of central bank money.

This is analogous to how commercial bank money (which most consumers use) settles on central bank reserves (which underpin the system). The layered model is well established in traditional finance.

Intersection 2: Regulated Stablecoins as CBDC Complements

Most central banks are not trying to replace all private digital money. The ECB’s digital euro is designed to coexist with bank deposits, payment applications, and stablecoins. The Bank of England has been explicit that the digital pound is not intended to replace commercial bank money — it is intended to complement it.

In this coexistence model, regulated stablecoins (USDC, EURC) serve the private sector innovation layer — programmable, globally portable, DeFi-compatible. Retail CBDCs serve the public layer — accessible to all citizens, no credit risk, legal tender. Both serve their domains.

Intersection 3: Stablecoins as CBDC On-Ramps

In jurisdictions where a retail CBDC does not yet exist, regulated stablecoins effectively perform a similar function for users already in the digital asset ecosystem. As CBDCs launch, regulated stablecoin issuers may position themselves as licensed distribution infrastructure — wallets and interfaces through which citizens access their CBDC.

Circle has explicitly signalled this direction, positioning USDC as CBDC-compatible infrastructure rather than a competitor.

Section 9: What CBDCs Mean for Payments Professionals

If you work in payments architecture, product, or operations, CBDCs will touch your work within the next five to ten years. Here is where the practical impact falls.

Impact on Commercial Banks

Commercial banks face a genuine structural challenge from retail CBDCs. If citizens can hold CBDC directly with the central bank, they may reduce their commercial bank deposits — particularly in times of financial stress, when a flight to the safety of CBDC could be very rapid.

This is why most central bank CBDC designs include holding limits — caps on how much CBDC an individual can hold. The Bank of England has proposed a limit of £10,000–£20,000 for the digital pound. The ECB has proposed €3,000 for the digital euro. These limits are explicitly designed to prevent disintermediation of commercial banks.

For banks: the CBDC creates both risk (deposit outflow) and opportunity (distribution infrastructure revenue, programmable product development on CBDC rails).

Impact on Payment Engines

Payment engines processing ISO 20022 messages need to evolve to handle CBDC payment instructions. The payment data — Debtor, Creditor, Amount, Purpose — remains consistent with ISO 20022 structure. But the settlement layer changes.

Instead of settling through a commercial bank’s nostro/vostro accounts on RTGS, a wholesale CBDC settlement instruction triggers a tokenised transfer on the CBDC platform. Payment engines must integrate with CBDC APIs — whether that is a central bank API layer (as Project Rosalind explored) or a DLT interface.

The ISO 20022 message standard is well-suited to CBDC contexts — its rich data structure carries everything needed to describe a CBDC payment instruction. SWIFT is actively exploring how its messaging infrastructure connects to CBDC platforms.

Impact on Correspondent Banking

Wholesale CBDCs are an existential challenge to the correspondent banking model for specific corridors. If mBridge (or its successors) scales to cover major trade corridors, banks in those corridors lose the fee income from correspondent services — but gain faster, cheaper settlement for their own cross-border needs.

The net effect for a bank depends heavily on which side of the correspondent relationship it sits. Smaller banks that depend on correspondents for international access benefit from CBDC-enabled direct access. Major correspondent banks face revenue compression in the corridors where CBDC arrangements emerge.

Impact on Corporate Treasurers

Retail and commercial CBDCs open new treasury management possibilities. If a corporate can hold CBDC directly — with no credit risk on the balance, instant settlement, and programmable disbursement — the appeal for cash management purposes is significant.

For multinationals operating in jurisdictions with live CBDCs, treasury architects need to assess:

- Can the corporate hold CBDC?

- Are holding limits an issue for large corporate balances?

- How does the CBDC integrate with the ERP and treasury management system?

- What happens to CBDC liquidity in a financial crisis — does it behave like cash or like a bank deposit?

Section 10: Common Misconceptions

“A CBDC is just the government’s version of a stablecoin.”

Not quite. A stablecoin is a private instrument that mimics sovereign currency. A CBDC is sovereign currency in a new form. The difference is not semantic. It is the difference between a photocopy of a banknote and the banknote itself.

“CBDCs will replace cash completely.”

Most central bank designs explicitly preserve cash as an alternative. The digital pound project documentation states that the Bank of England has no plans to abolish cash. CBDCs are designed to supplement, not replace, physical currency. The decision to use CBDC or cash remains with the individual.

“CBDCs are just cryptocurrency with government backing.”

Most retail CBDC designs do not use public blockchain technology. They run on centralised or permissioned ledgers controlled by the central bank. They are not “crypto” in the way Bitcoin or Ethereum is — there is no mining, no public anonymity, no open participation in block validation.

“Stablecoins will become obsolete when CBDCs launch.”

Unlikely in the near term. Stablecoins offer global portability, DeFi compatibility, and private sector programmability that most CBDC designs deliberately do not replicate. They serve different use cases in a complementary ecosystem. The more likely outcome is regulatory clarity that positions regulated stablecoins as licensed private complements to public CBDCs.

“Holding a CBDC is risk-free.”

The monetary value is risk-free — the central bank cannot default on its own currency. But there are other risks: technology risks (wallet hacks, platform outages), programmability risks (government-imposed spending restrictions), and privacy risks (transaction surveillance). Risk-free in terms of credit does not mean risk-free in all dimensions.

Section 11: The Global CBDC Landscape — Where We Are Today

| Jurisdiction | CBDC Project | Type | Status (2025) |

| China | e-CNY (Digital Yuan) | Retail | Live — 26+ cities, ¥1.8T+ transacted |

| Bahamas | Sand Dollar | Retail | Live since 2020 |

| Nigeria | eNaira | Retail | Live since 2021 — low adoption challenges |

| Eastern Caribbean | DCash | Retail | Live across 8 island nations |

| Jamaica | JAM-DEX | Retail | Live since 2022 |

| European Union | Digital Euro | Retail + Wholesale | Preparation phase; legislation in progress |

| United Kingdom | Digital Pound (“Britcoin”) | Retail + Wholesale | Design phase; legislation pending |

| United States | Digital Dollar | Wholesale research | No formal commitment; FRB research ongoing |

| India | e-Rupee | Retail + Wholesale | Pilot since 2022 — scaling |

| UAE | Digital Dirham | Retail + Wholesale | Pilot (mBridge for wholesale) |

| Saudi Arabia | Project Aber | Wholesale | Pilot concluded; successor work ongoing |

| BIS / Multiple | mBridge | Wholesale (Multi-CBDC) | MVP stage — live commercial transactions |

| BIS / Multiple | Project Agorá | Wholesale tokenisation | Active pilot — 7 central banks |

Key Takeaways

- A CBDC is a digital form of sovereign currency issued directly by the central bank. It carries the same legal tender status as banknotes. Its liability rests on the sovereign state — not a private company.

- Retail CBDCs target citizens and businesses. Wholesale CBDCs target financial institutions. The two are architecturally and operationally distinct, even when issued by the same central bank.

- The deepest difference from stablecoins is the trust architecture: CBDC = sovereign credit (risk-free in monetary terms). Stablecoin = private issuer credit, backed by reserves. Both can be safe. They are not the same.

- CBDC design involves five major architectural decisions: centralised vs distributed ledger, account-based vs token-based, direct vs two-tier issuance, degree of programmability, and privacy model. Each decision has significant implications for payments architects.

- CBDCs and stablecoins are not purely competitive. The most likely near-term outcome is a layered ecosystem: retail CBDCs for public access, wholesale CBDCs for interbank settlement, and regulated stablecoins for private sector programmability and global portability.

- As a payments professional, CBDCs will directly affect payment engine design, correspondent banking, corporate treasury management, and commercial bank deposit models — within your working lifetime, possibly within your current role.

What to Read Next

If you are new to stablecoins and want the foundational context for the comparisons in this article, the Stablecoins Series (Parts 1–5) covers the complete stablecoin landscape from first principles to solution architecture. The series is available on the PaymentTalks blog.

For deeper technical reading on CBDCs, the BIS publishes comprehensive research papers and project reports at bis.org — the BIS Annual Economic Report chapters on CBDCs are among the most rigorous publicly available analyses.

The conversation between sovereign money and private digital money is one of the defining questions of the coming decade in finance. Understanding both sides — deeply, precisely, and practically — is the foundation of that conversation.