Here is something I noticed after working across SEPA in Europe, Fedwire and ACH in the USA, NEFT and RTGS in India, and SARIE in Saudi Arabia: every time I moved to a new rail, I was not really learning something new. I was recognising the same model with a different name. That realisation changed how I approach every new market.

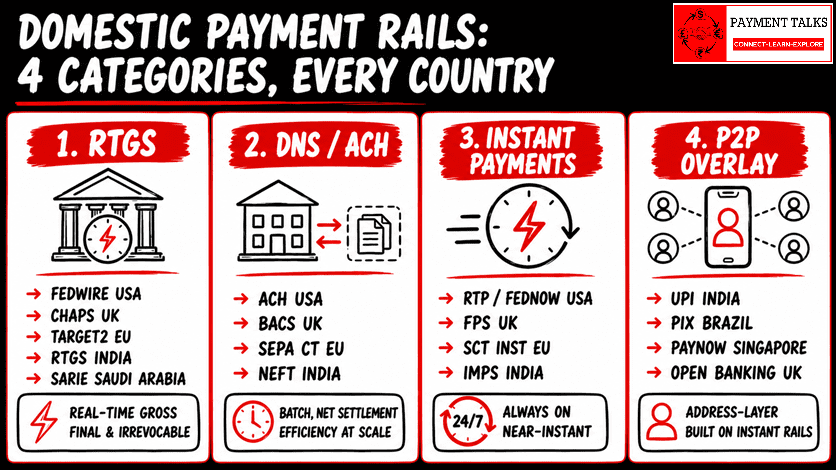

Every country’s domestic payment infrastructure is built on the same three core models. 1) RTGS. 2) DNS, also called ACH or bulk clearing and 3) Instant Payments. A fourth category is now emerging: P2P overlay rails. These four models exist across every major economy. The names change. The underlying settlement logic does not.

This article gives you the framework. Learn it once and you can map any domestic payment landscape anywhere in the world. To first understand what a payment is at its core, see the foundational article on what a payment is.

What ‘Domestic’ Actually Means in Payments

Domestic payments operate within a single financial jurisdiction. One central bank manages the clearing and settlement infrastructure. That jurisdiction can be a country or a monetary union. SEPA covers 36 countries in Europe, but every payment within SEPA operates under one rulebook, settles in euro, and runs through shared clearing infrastructure. A transfer from Munich to Milan via SEPA Credit Transfer is a domestic payment by this definition.

The defining characteristic of domestic payments is that the central bank sits at the centre of the settlement process. It is the central bank that runs or oversees the RTGS system, mandates participation in clearing schemes, and manages the settlement accounts that commercial banks use to fund their payment obligations to each other. Settle within one central bank’s domain and you are on domestic rails.

Once a payment crosses into a different central bank’s domain, you enter correspondent banking territory — a different set of rails entirely.

Three Core Rail Categories — and One Emerging

Strip away the branding. Underneath every domestic payment system in the world, you find the same settlement logic. Here are the four categories:

- RTGS — Real-Time Gross Settlement: High-value, time-critical payments. Each payment settles individually and immediately. Final and irrevocable.

- DNS — Deferred Net Settlement: Also called ACH or bulk clearing. Payments batch within a defined window. Bank positions net against each other. Only the net amounts settle.

- Instant Payments: 24/7, low-to-medium value, near-immediate settlement. The always-on consumer and business rail.

- P2P Overlay Rails: Address-based payment layer sitting on top of instant rails. The newest category — not yet present in every market, but spreading fast.

Every major economy has the first three. The fourth is emerging. The direction is clear.

4-Category Framework Diagram

RTGS — The High-Value Rail Where Every Payment Is Final

RTGS is the system where large-value, time-sensitive payments settle. Each payment is processed individually, in real time, on a gross basis. No batching, no netting. The moment an RTGS payment settles, it is final and irrevocable. There is no unwinding it. That finality is what makes RTGS the system of choice for transactions where certainty of settlement is non-negotiable.

RTGS systems operate during central bank business hours. The sending bank must hold sufficient funds in its central bank settlement account at the exact moment the payment is submitted. This makes liquidity management critical — banks actively monitor their central bank positions throughout the day. Nostro accounts and central bank settlement mechanics are closely tied to how RTGS liquidity works in practice.

Here is what most practitioners get wrong early in their careers: they think Fedwire in the USA and RTGS in India are fundamentally different things. They are not. I have worked on both, and once you understand Fedwire, you understand RTGS India — and CHAPS, and TARGET2, and SARIE. Same logic, same finality, different jurisdiction, different name.

RTGS is the backbone for interbank settlements, large corporate treasury transfers, and securities settlements. These are the payments that cannot wait and cannot fail.

| Country / Region | RTGS System |

| USA | Fedwire (Federal Reserve) |

| UK | CHAPS (Bank of England) |

| Eurozone / SEPA | TARGET2 / T2 (European Central Bank) |

| India | RTGS (Reserve Bank of India) |

| Saudi Arabia | SARIE (Saudi Central Bank / SAMA) |

| Brazil | STR — Sistema de Transferencia de Reservas (Banco Central do Brasil) |

| Singapore | MEPS+ (Monetary Authority of Singapore) |

| Australia | RITS (Reserve Bank of Australia) |

DNS — The Batch Rail That Powers Payroll and Everyday Transactions

DNS stands for Deferred Net Settlement. Instead of settling each payment the moment it arrives, the system accumulates transactions across a defined time window, nets the positions between banks — offsetting debits against credits — and then settles only the net amounts at defined intervals. Typically once or several times per day.

This is how payroll runs. This is how bulk bill payments process. This is the rail for low-to-medium value, non-urgent transactions where real-time availability is not the primary requirement.

ACH in the USA has become such a dominant brand that practitioners outside the USA often treat it as a uniquely American construct. It is not. NEFT in India, BACS in the UK, SEPA Credit Transfer across 36 European countries — all are DNS systems. The underlying logic is identical: batch, net, settle the net. The same model that operations teams run in New York runs in Mumbai, London, and Frankfurt.

The efficiency advantage of DNS is significant. By netting bilateral positions before settlement, the actual liquidity required is a fraction of the gross transaction value being exchanged. This is why DNS carries the highest transaction volume in most economies — even though individual transaction amounts are smaller than RTGS. It is the workhorse rail of every financial system.

| Country / Region | DNS / ACH System |

| USA | ACH (NACHA — National Automated Clearing House Association) |

| UK | BACS (Bankers’ Automated Clearing Services) |

| Eurozone / SEPA | SEPA CT – STEP2 (EBA Clearing) |

| India | NEFT (National Electronic Funds Transfer — Reserve Bank of India) |

| Brazil | TED / DOC (being progressively replaced by PIX) |

| Singapore | GIRO (Association of Banks in Singapore) |

| Australia | BECS System |

Instant Payments — The 24/7, Always-On Rail

Instant payment systems deliver funds to the recipient within seconds, around the clock, every day of the year — weekends, public holidays, no exceptions. This is where consumer transfers, e-commerce settlements, and time-sensitive business payments flow when RTGS is unavailable (outside central bank hours) or when the transaction value does not warrant an RTGS payment.

One thing architects need to understand: the ‘instant’ label describes the user experience, not necessarily the settlement mechanism under the hood. Different instant payment systems settle differently. Some settle each payment individually in real time. Others net positions across very short intervals — every few minutes — and settle the net. The end result for the user is the same: funds available within seconds. But the system design and liquidity management implications differ by implementation.

FPS in the UK, SEPA Instant Credit Transfer in Europe, IMPS in India, RTP and FedNow in the USA — different names, same category. To understand how a payment moves through the full settlement chain on one of these rails, the payment life cycle article walks through it step by step.

| Country / Region | Instant Payment System |

| USA | RTP (The Clearing House) / FedNow (Federal Reserve — launched 2023) |

| UK | Faster Payments Service (FPS — Pay.UK) |

| Eurozone / SEPA | SEPA Instant Credit Transfer (SCT Inst) |

| India | IMPS (Immediate Payment Service — NPCI) |

| Saudi Arabia | Instant payment rail branding within the SARIE framework |

| Brazil | PIX (Banco Central do Brasil — launched November 2020) |

| Singapore | FAST (Fast And Secure Transfers — MAS) |

| Australia | NPP (New Payments Platform — NPPA) |

P2P Overlay Rails — The Emerging Fourth Category

P2P overlay rails are not a separate clearing and settlement network. They sit on top of an instant payment rail and add one critical layer: addressability. Instead of entering a bank account number and sort code, you pay using a phone number, email address, or national ID. The overlay system resolves that address to the correct bank account behind the scenes and initiates the payment on the underlying instant rail.

The pioneer — and still the benchmark — is India’s UPI (Unified Payments Interface), built and operated by NPCI (National Payments Corporation of India) on top of IMPS. What UPI demonstrated, at a scale running into billions of transactions per month, is that removing the need to know a bank account number removes the biggest friction in consumer payments. When payment is as simple as sharing a phone number, adoption is transformational.

Brazil took a different architectural approach with PIX, launched by Banco Central do Brasil in November 2020. PIX functions both as the instant payment rail and as the P2P overlay simultaneously — the central bank built the address layer into the core infrastructure. The result: mass adoption within two years of launch.

The UK built Open Banking-based payment initiation on top of FPS. Singapore has PayNow on FAST. Australia has PayID and Osko on NPP. The USA has Zelle, which operates across multiple banks on top of RTP and ACH. Europe is building overlay capabilities through Open Banking regulation (PSD2). The Middle East is developing rapidly — driven by national digital payment strategies across the region.

I will cover UPI and the mechanics of P2P overlay rails in depth in a dedicated article. Here, the architectural point is what matters: this is a distinct fourth category that you need to account for when mapping any country’s domestic payment landscape.

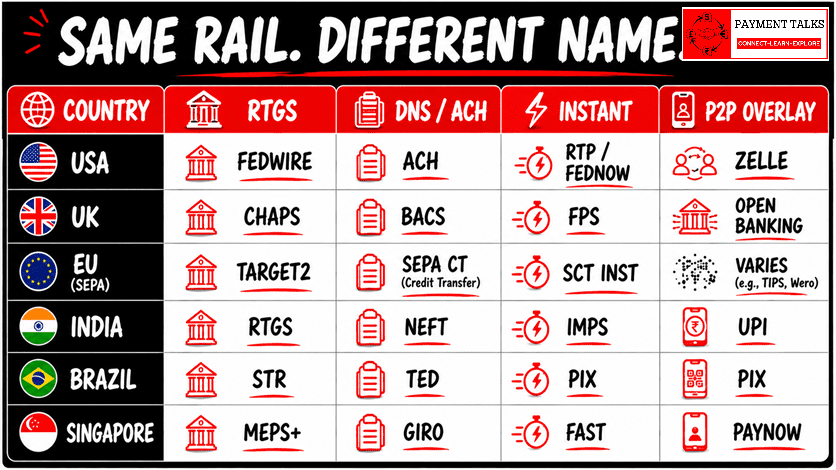

Every Country’s Rails in One View

Here is the practical output of the framework. The same three categories, mapped across major economies.

Global Rail Comparison Table

| Country | RTGS | DNS / ACH | Instant |

| USA | Fedwire | ACH (NACHA) | RTP / FedNow |

| UK | CHAPS | BACS | FPS |

| EU / SEPA | TARGET2 / T2 | SEPA CT | SCT Inst |

| India | RTGS | NEFT | IMPS |

| Saudi Arabia | SARIE | -NA- | IPS |

| Brazil | STR | TED | PIX |

| Singapore | MEPS+ | GIRO | FAST |

| Australia | RITS | BECS | NPP |

Read across any row. Look at India: RTGS maps directly to Fedwire. NEFT maps directly to ACH. IMPS maps to FPS or RTP. UPI is the most advanced P2P overlay in the world, ahead of what most developed markets have built. Working knowledge of any single country row gives you the framework to understand every other. The model is universal.

What This Means When You Work Across Markets

The first question on any new payment implementation should always be: which rail is this transaction going to flow over? That question determines everything that follows — settlement timing, finality, liquidity requirements, message format, and risk profile. The payment life cycle article walks through how this plays out in practice.

ISO 20022 is now the converging message standard across all these rails globally. Fedwire has migrated to ISO 20022. T2 (TARGET2) in Europe runs on it. CHAPS in the UK runs on it. SARIE in Saudi Arabia runs on it. The message layer is standardising even as the rail names remain local. If you want to understand ISO 20022 and why every payments professional needs to know it, start with the fundamentals article.

The takeaway is straightforward: there is no need to treat each country’s payment infrastructure as a separate discipline. Learn the four categories. Understand what drives the design choice between them — value, urgency, finality, availability hours. Then apply that knowledge in any jurisdiction. The branding will change. The architecture will not.

Frequently Asked Questions

What is the difference between RTGS and instant payments?

RTGS settles high-value payments individually and in real time but operates during central bank business hours only. The sending bank must hold funds in its central bank settlement account at the moment of payment. Instant payments operate 24/7, target low-to-medium value transactions, and deliver funds within seconds — but serve different transaction types and operate under different availability and liquidity models.

Is ACH the same as SEPA Credit Transfer?

Functionally yes. Both are Deferred Net Settlement (DNS) systems. Payments batch in a defined window, bank positions net against each other, and only the net amounts settle at defined intervals. The names differ, the jurisdictions differ, but the underlying clearing and settlement model is identical.

What is RTGS?

Real-Time Gross Settlement. A payment system where each transaction settles individually, in real time, on a gross basis — no netting, no batching. Settlement is immediate and irrevocable. Central banks operate RTGS systems. Examples: Fedwire (USA), CHAPS (UK), TARGET2/T2 (Eurozone), SARIE (Saudi Arabia), RTGS (India).

What is SARIE in Saudi Arabia?

SARIE (Saudi Arabian Riyal Interbank Express) is Saudi Arabia’s RTGS system, operated by SAMA (Saudi Central Bank). It is the direct equivalent of Fedwire in the USA or CHAPS in the UK — the high-value, real-time gross settlement system for interbank transfers in Saudi riyal.

Is SEPA a domestic or cross-border payment system?

Domestic. SEPA (Single Euro Payments Area) covers 36 countries but operates as a single financial jurisdiction for euro-denominated payments. A payment between Germany and France via SEPA Credit Transfer or SEPA Instant is a domestic payment — not cross-border — because both countries operate under the same rulebook and shared settlement infrastructure.

Is UPI a payment rail?

No. UPI (Unified Payments Interface) is a P2P overlay layer, not a separate clearing and settlement rail. It sits on top of IMPS (India’s instant payment rail) and adds address-based routing — you pay using a phone number or Virtual Payment Address (VPA) rather than a bank account number. The actual clearing and settlement happen through IMPS underneath.

How many domestic payment rail categories are there?

Three foundational categories — RTGS, DNS (ACH / bulk clearing), and Instant Payments — exist in every major economy. A fourth category, P2P overlay rails (UPI in India, PIX in Brazil, PayNow in Singapore, Open Banking payments in the UK), is emerging globally but not yet universal.

Why does the DNS model carry the highest transaction volume if it settles later than RTGS?

DNS handles the highest volume because it serves everyday, non-urgent payments at scale — payroll, bill payments, recurring transfers — where real-time availability is not the priority. Its netting mechanism also means the actual liquidity required for settlement is a fraction of the total value exchanged. Most economies see the vast majority of payment volume by count flowing through DNS and instant rails, with RTGS handling a small number of very high-value individual transfers.