A Tale of Two Payments

It is Monday morning. Two corporate treasury teams each initiate the same $500,000 cross-border payment from the United Kingdom to a supplier in the Philippines. Same origin, same destination, same amount. What happens next is where the theory ends and the real difference between payment rails shows up.

Treasury Team A goes through their bank. The payment instruction routes through a US correspondent, then a Philippines correspondent, then finally lands at the beneficiary’s local bank. The money arrives Wednesday. Net received: $499,215. $785 is gone in fees and FX margin, spread across a chain the treasury team cannot see into and cannot track in real time.

Treasury Team B uses a stablecoin payment service. GBP converts to USDC through a licensed exchange. A blockchain transfer executes on Solana. The counterparty’s exchange converts USDC to PHP. The supplier is paid in under 60 seconds. Fee: under $1.

Same payment. Two completely different journeys. That gap is the entire reason this series exists.

In Part 1 we covered what a stablecoin actually is. In Part 2 we covered how it is minted and burned. This is where it stops being theory. Part 3 walks the real payment flow end to end, and gives you a straight, unhyped answer to where stablecoin rails beat SWIFT and SEPA, and where they still lose.

How Do Traditional Cross-Border Payment Rails Actually Work?

You cannot judge a new rail against an old one you only half understand. If you live in payments daily, most of this section is a refresher, but the framing matters for everything that follows, so do not skip it.

What Is the Correspondent Banking Model?

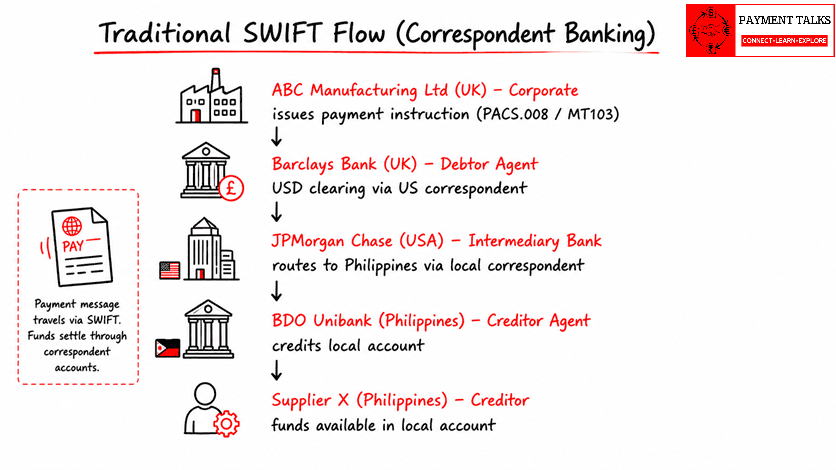

When a bank sends a cross-border payment, it almost never sends it directly. It routes through a chain of correspondent banks, institutions that hold accounts with each other and act as intermediaries. For a GBP-to-PHP payment, that chain typically runs originating bank, US dollar correspondent, Philippines correspondent, beneficiary bank.

[VISUAL 1: Diagram showing the correspondent banking chain for a GBP-to-PHP cross-border payment, from originating bank through US and Philippines correspondents to the beneficiary bank]

Every hop in that chain does three things at once:

- Charges a fee, typically $5 to $20 per hop

- Applies an FX margin, typically 0.5% to 2%

- Adds processing time, since every bank has its own cut-off windows

For the full mechanics of how these accounts are structured, see Nostro, Mirror Nostro, Vostro, and Loro Accounts and Understanding Correspondent Banking.

SWIFT carries the payment instructions, the messages. It does not move the money. The actual funds settle through the bilateral correspondent account relationships underneath. That is precisely why a SWIFT message can arrive in seconds while the funds settlement behind it takes days. Confusing the message layer with the settlement layer is one of the most common misreadings of how correspondent banking works.

What Do ISO 20022 and SWIFT MT Messages Actually Carry?

In the SWIFT world, the payment instruction from Bank A to Bank B travels in a standardised message:

- MT103: single customer credit transfer, the legacy format

- PACS.008: the ISO 20022 equivalent, FI-to-FI customer credit transfer

- PAIN.001: the corporate-to-bank payment initiation message, upstream of the inter-bank leg

These messages carry structured fields, debtor, creditor, amount, currency, purpose, remittance information. The problem is that as a payment hops through correspondents, that structured data gets truncated or reformatted along the way. That data loss is one of the core reasons behind the ISO 20022 migration. For the full field-level breakdown, see Fundamentals of ISO 20022.

For stablecoin architects, this is not a solved problem you can skip past. Blockchain transfers are even leaner on native metadata than an MT103. We cover exactly how to bolt structured remittance data onto a stablecoin rail in Part 5.

How Does a Stablecoin Payment Flow End to End?

Now walk the stablecoin equivalent of that same $500,000 GBP-to-PHP payment.

The Scenario

Debtor: ABC Manufacturing Ltd, Birmingham, UK, holding a GBP account at Barclays.

Creditor: Global Parts Inc, Manila, Philippines, holding a PHP account at BDO Unibank.

Amount: $500,000 USD equivalent.

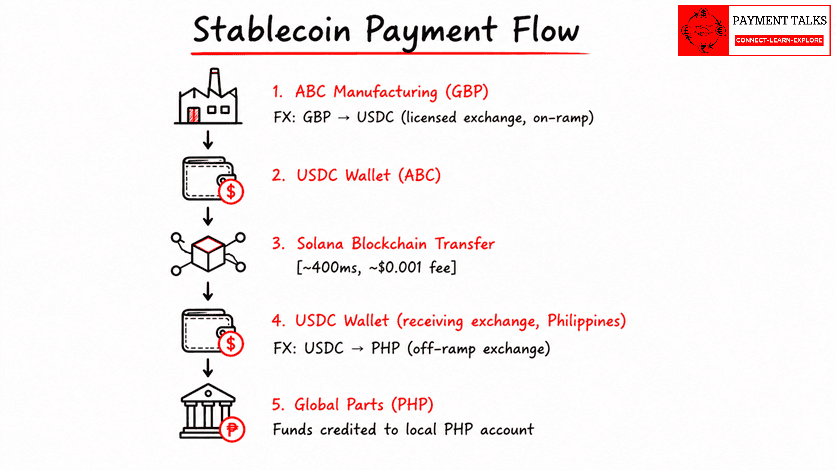

The architecture: “fiat at the edges, stablecoin in the middle.” This is the on-ramp / off-ramp model, the most common enterprise stablecoin payment pattern. The client only ever touches fiat. The stablecoin handles the cross-border middle mile.

- Initiation. ABC Manufacturing instructs its payment platform to send $500,000 to Global Parts’ wallet address. To the treasury team, it looks like any other payment instruction, debtor, creditor, amount, purpose. The stablecoin engine handles everything underneath.

- On-ramp: GBP to USDC. The platform converts GBP to USDC at the prevailing rate through a licensed exchange (Coinbase Prime, Bitstamp, B2C2 are common names here). The exchange sells USDC from its liquidity pool and debits ABC Manufacturing’s account. ABC now holds roughly $500,000 in USDC.

- The blockchain transfer. The platform sends USDC on Solana from ABC’s wallet to the receiving exchange’s wallet in the Philippines. Solana validates and finalises the transaction in around 400 milliseconds. It is permanently recorded on-chain, visible and auditable by both sides.

- Off-ramp: USDC to PHP. The receiving exchange (Coins.ph or PDAX are typical) takes the USDC, sells it from its pool, and converts to PHP at the prevailing rate. PHP lands in Global Parts’ BDO Unibank account.

- Confirmation. ABC sees the blockchain transaction hash. Global Parts sees the PHP credit. Both sides have an independently verifiable record of the same event.

[VISUAL 2: End-to-end flow diagram showing GBP entering at the on-ramp, converting to USDC, transferring on Solana, converting to PHP at the off-ramp, and landing in the beneficiary account]

Total time: under 60 seconds, excluding on/off-ramp FX settlement which varies by platform. Total cost: exchange FX margin (typically 0.1% to 0.5%) plus a blockchain fee under a cent. No correspondent bank fees anywhere in the chain.

This is not the only cross-border settlement architecture worth knowing. mBridge takes a different approach entirely, using multiple central bank digital currencies on a shared ledger instead of a commercial stablecoin. Worth understanding both if you are advising on corridor strategy.

What Are the Three Major Stablecoin Payment Use Cases?

Use Case 1: Cross-Border B2B Payments, Replacing the Correspondent Chain

This is the highest-impact use case for large businesses. The correspondent chain is expensive, slow, and opaque by design. Stablecoin rails, used as the settlement layer, remove hops, cut fees by 90% to 98%, and deliver same-minute settlement.

Real-world reference point: Ripple’s On-Demand Liquidity (ODL). Ripple’s network uses XRP, a cryptocurrency rather than a stablecoin, but the mechanism is identical in principle, as a bridge asset in cross-border corridors. Instead of pre-funding nostro accounts in every currency pair, the originating bank converts fiat to XRP, sends it across the network, and the receiving side converts to local fiat in seconds.

The same architecture runs on USDC as the bridge asset. Bitso in Mexico, SBI Remit in Japan, and Tranglo in Southeast Asia all operate stablecoin corridors carrying hundreds of millions of dollars daily. 🚩 Verify current daily volume figures for Bitso, SBI Remit, and Tranglo before publishing, these move fast.

The practical implication for architects: correspondent banking forces banks to hold pre-funded nostro accounts in every currency pair they support. That is capital-intensive. Stablecoin rails allow just-in-time liquidity, converting fiat to stablecoin only when a specific payment needs it. That is a real balance sheet efficiency gain, not a marketing line.

Use Case 2: Remittances, the Use Case With a Human Face

The global remittance market moves over $800 billion a year. The World Bank puts the average global cost of sending a remittance at roughly 6.3% of the amount sent. In parts of Africa and Southeast Asia, 8% to 12% is not unusual.

Picture a construction worker in Saudi Arabia earning SAR 3,000 a month, sending SAR 2,000, about $533, home to family in the Philippines.

Traditional route (Western Union-style): fee around $25 (about 4.7%), FX margin around 1.5%, arrival same day if lucky, more often next day. Net received: roughly $495.

Stablecoin route via a licensed remittance app using USDC: worker loads SAR into the app’s local liquidity pool, app converts to USDC, USDC moves to a Philippines partner exchange, partner converts to PHP and delivers to the family’s e-wallet or bank account. Fee: around $2 to $3 (about 0.5%). Time: minutes. Net received: roughly $527.

That $32 difference does not sound large in isolation. Multiply it across 200-plus million migrant workers sending money home every month and the aggregate impact runs into billions. This is the use case where the rail choice is not an efficiency debate, it is a household budget line.

Strike (Lightning Network plus stablecoins), Tempo (Europe-to-Africa corridors), and a growing list of Philippines-US and Philippines-Middle East players are actively running this model in production.

Use Case 3: Corporate Treasury, Eliminating Trapped Liquidity

This is the use case generating the most CFO and treasurer-level interest right now.

The problem: a multinational with subsidiaries in 15 countries holds working capital in 15 local currencies at 15 different banks. Moving money between subsidiaries means cross-border wires, fees, delay, FX conversion, every time. Capital sits idle locally instead of being deployed where it is needed globally. That is trapped liquidity.

GlobalTech Corp runs operations in the US, UK, Singapore, UAE, and Brazil. Instead of holding working capital in local currency everywhere, it runs a USDC treasury model:

- Each subsidiary converts idle local currency into USDC daily or weekly

- USDC pools into a central treasury wallet, or distributed wallets with an aggregated view

- When a subsidiary needs to pay a local supplier, treasury releases USDC to it

- The subsidiary’s local exchange converts USDC to local currency and pays the supplier

The payoff: global treasury can net payables and receivables across subsidiaries before a single dollar moves externally. Intercompany transfers that took two days now take seconds, at effectively zero transfer fee, with FX conversion timed to whatever rate suits treasury rather than whatever the correspondent chain happens to offer that day.

Coinbase, Circle, and Fireblocks have all published Fortune 500 case studies on this model. PayPal runs its own PYUSD stablecoin for exactly this kind of internal treasury use.

SWIFT vs SEPA vs Stablecoin Rails: How Do They Compare Head to Head?

Here is the full picture for anyone making an actual rail selection decision, not a marketing comparison.

| Dimension | SWIFT (MT103 / PACS.008) | SEPA Credit Transfer | Stablecoin Rails |

| Settlement time | 1–3 business days | D+1 (next business day) | Seconds to minutes |

| Cross-border fees | $25–$75+ per transaction | < €0.50 (SEPA only) | < $1 (often < $0.01) |

| Operating hours | Business hours, weekdays | Business hours, weekdays | 24/7/365 |

| Currency coverage | 140+ currencies | Euro zone only | USD/EUR dominant, growing |

| Reversibility | Possible (recalls, R-transactions) | Possible (8-week window) | Generally irreversible |

| Data richness | ISO 20022 rich / MT limited | ISO 20022 rich | Minimal native metadata |

| Regulatory clarity | Fully established | Fully established | Evolving rapidly |

| AML/KYC framework | Mature (FATF, CBPR+) | Mature (EPC) | Maturing (FATF VASP rules) |

| Dispute resolution | Established process | Established process | Limited, largely manual |

| Network reach | 11,000+ institutions | 36 SEPA countries | Growing institutional adoption |

| Transparency | Limited (correspondent hops) | Limited | Full on-chain visibility |

| Minimum viable amount | Typically $1,000+ economical | Any amount | Any amount, even micro-payments |

Where Do Stablecoin Rails Win, and Where Do They Fall Short?

Being honest about this matters. Recommending the trendy rail over the right one helps nobody, least of all the client who has to live with the architecture.

Where stablecoins have a clear edge:

- High-fee corridors. Anywhere correspondent banking charges $30 to $75-plus per transaction, a rail costing $0.01 is transformational, especially for mid-market businesses paying frequently.

- 24/7 settlement requirements. SWIFT has cut-off times. SEPA processes overnight. A supplier who needs paying at 2am on a Sunday in a different time zone cannot be served by traditional rails. Stablecoins do not know what a cut-off time is.

- High-volume, low-value payments. Sending $5 by SWIFT makes no economic sense. On Solana it costs a fraction of a cent, opening the door to micro-payments and per-use billing models that traditional rails simply cannot price for.

- Emerging market corridors. The Philippines, Nigeria, Kenya, Indonesia, and similar markets have historically been expensive and unreliable for SWIFT. Stablecoin corridors exist specifically because that gap was left wide open.

- Intra-company treasury movements. There is no consumer protection argument for routing intercompany transfers through correspondent banks. Speed and cost win outright here.

Where traditional rails still hold the line:

- Reversibility and dispute resolution. A SWIFT payment can be recalled with effort. A SEPA payment can be returned within an 8-week window. A blockchain transaction is final the moment it confirms. For consumer payments, B2C e-commerce, or any scenario needing fraud recall, traditional rails still offer protections stablecoin rails cannot currently match.

- Domestic retail payments. SEPA Instant, UK Faster Payments, and India’s IMPS already deliver stablecoin-level speed domestically, with full regulatory protection and consumer trust baked in. Stablecoins offer no real advantage here.

- High-value, regulated settlements. Above roughly $10 million, Fedwire and CHAPS deliver same-day finality with a central bank backstop behind them. Exchange liquidity depth for a single transaction of that size can become the limiting factor on a stablecoin rail.

- Jurisdictions with unclear or hostile crypto regulation. China, an evolving India, and several GCC markets restrict or prohibit stablecoin payments domestically. Building an architecture that assumes stablecoin rails in these jurisdictions is a regulatory landmine, not an efficiency play.

What Is the Architect’s Rail Selection Framework?

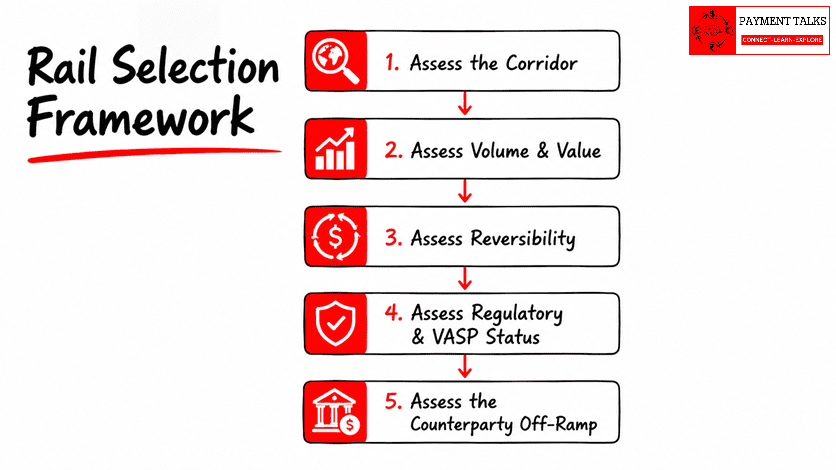

When you are asked whether stablecoin rails fit a given payment flow, run it through five checks, in order.

[VISUAL 3 : Five-step decision flow diagram for rail selection, Corridor Cost and Speed to Volume and Value to Reversibility Requirement to Regulatory and VASP Status to Counterparty Off-Ramp Readiness]

- Assess the corridor. Is it expensive, over $10 in fees? Slow, over a day? Unreliable or unavailable through traditional rails? A yes to any of these means stablecoin rails are worth evaluating seriously.

- Assess volume and value. High frequency, low value is a strong stablecoin case. Very high value, above roughly $5 million in a single transaction, means you need to check exchange liquidity depth carefully before committing, not after.

- Assess reversibility requirements. Does the scenario need recall capability, fraud dispute resolution, or regulatory consumer protection? If yes, traditional rails are required, or you need a hybrid model. This is the mistake I see most often, teams get excited about the speed and quietly skip asking whether the payment ever needs to be unwound.

- Assess the regulatory environment. Is stablecoin payment activity licensed and compliant in both the originating and receiving jurisdiction? Do both parties hold the necessary VASP registration? This is the second recurring mistake, architects assume a corridor is clear because the technology works, without checking whether either side actually holds a valid licence. If the answer is unclear, do not proceed until it is resolved.

- Assess the counterparty. Does the receiving party have a working stablecoin wallet and a reliable off-ramp to their local currency? This is the third mistake, and the most common one in practice: the on-ramp gets all the design attention and the off-ramp gets none, even though it is usually the weakest and least liquid link in the entire chain.

Those three, skipping reversibility checks, skipping regulatory and VASP verification, and under-designing the off-ramp, account for most of the stablecoin payment failures I hear about after the fact. None of them are exotic risks. They are just the ones that get skipped when a rail feels fast enough to stop asking questions.

What Are the Biggest Misconceptions About Stablecoin Payment Flows?

Misconception: Stablecoins Eliminate FX Entirely

They do not. Stablecoins eliminate the FX friction inside the payment chain, the multiple conversions layered through correspondent relationships. If you are paying a supplier in Philippine Pesos, somebody still converts from USD-pegged stablecoin to PHP. That conversion just happens once, at a transparent and competitive point, the off-ramp exchange, instead of being buried inside opaque correspondent margins across several hops.

Misconception: Stablecoin Rails Mean You Can Ignore SWIFT Entirely

Not yet, and maybe not ever in the way people assume. The overwhelming majority of global payment volume still runs on SWIFT. Most production stablecoin payment solutions run alongside SWIFT, using it for the data messaging layer and stablecoins for the settlement layer. SWIFT itself is piloting tokenised asset settlement. For how these two worlds are actually converging at the message level, see Stablecoins and ISO 20022. This is convergence, not replacement.

Misconception: Blockchain Transparency Means Payment Details Are Public

Partially true, and the part that is wrong matters. The blockchain records wallet addresses and amounts publicly, not the identity behind the wallet. On a public chain like Ethereum, anyone can see that address 0x742d sent 500,000 USDC to address 0x9b3c. Nobody can see that those addresses belong to ABC Manufacturing and Global Parts unless that link is published somewhere else. For institutional payments this is a compliance design question in its own right, since on-chain analytics firms can often de-anonymise large flows through exchange KYC data even without a public disclosure.

Key Takeaways

- Stablecoin payment rails run on a “fiat at the edges, stablecoin in the middle” architecture. Clients transact in local currency. The stablecoin carries the cross-border settlement layer in between.

- The on-ramp and off-ramp are the real integration points that matter. Their fee structure, liquidity depth, and regulatory status carry as much weight as the blockchain transfer itself.

- Stablecoins win decisively in corridors that are expensive, slow, or underserved, especially emerging market corridors and anything needing 24/7 settlement.

- Traditional rails still win on reversibility, consumer protection, high-value settlement, and jurisdictions with a clear regulatory framework for stablecoin activity.

- The three mistakes that break stablecoin payment projects are skipping the reversibility check, skipping VASP and regulatory verification, and under-designing the off-ramp.

- The right answer for most architects is not choosing one rail. It is designing for both, and knowing precisely which corridor, value, and risk profile sends a payment down which path.

Frequently Asked Questions

Q: Are stablecoin payments faster than SWIFT for every corridor?

A: Not universally. They are dramatically faster for cross-border corridors with correspondent hops, but domestic instant payment systems like SEPA Instant or UK Faster Payments already match stablecoin speed for local transfers.

Q: Can a stablecoin payment be reversed if sent to the wrong wallet?

A: Generally no. A confirmed blockchain transaction is final. This is the single biggest operational risk difference against SWIFT or SEPA, where a recall or return process, however slow, does exist.

Q: Do stablecoin rails eliminate correspondent banking fees completely?

A: They eliminate the multi-hop correspondent chain and its fees. You still pay an on-ramp and off-ramp FX margin, typically 0.1% to 0.5%, plus a near-zero blockchain fee.

Q: What is the biggest technical risk in a stablecoin payment corridor?

A: The off-ramp, not the blockchain transfer. The on-chain leg is fast and reliable. The receiving exchange’s liquidity and local currency conversion capability is usually the weakest and least tested part of the chain.

Q: Is SWIFT being replaced by stablecoin rails?

A: No, not in the current trajectory. SWIFT is piloting tokenised settlement and most production stablecoin corridors still use SWIFT-style messaging alongside blockchain settlement. The two are converging, not competing.

Q: What does VASP registration mean for a stablecoin payment corridor?

A: A Virtual Asset Service Provider registration is the regulatory licence required in most FATF-aligned jurisdictions to legally operate stablecoin on-ramp or off-ramp services. Missing VASP coverage on either side of a corridor is one of the most common reasons a stablecoin payment architecture stalls before launch.

What’s Next

You can now trace a stablecoin payment from originating corporate to beneficiary bank end to end, and you know when to recommend stablecoin rails over SWIFT, and when not to.

None of it holds up without the regulatory and risk picture behind it. Before you put stablecoins in front of a client or bake them into a payment architecture, you need the six risks that can break the model and the three regulatory frameworks reshaping what is legally permissible. That is Part 4, and it is the one I would make mandatory reading before any architect touches a production stablecoin system.