What Actually Happens When You Send a Stablecoin?

Send 1 USDC to someone. They send it to someone else. That person sends it to a third party. Where did the original dollar go?

Most payments professionals cannot answer that in one sentence on the spot. I could not either the first time I mapped it out. The answer is mechanical, not mysterious, but it breaks almost every instinct built over a career in correspondent banking.

In Part 1 of this series, we defined what a stablecoin is and why it exists. This article goes one level deeper: how a stablecoin is minted, how it behaves while it circulates, how it is destroyed, what actually sits behind it, which blockchain it settles on, and how institutions hold it without losing it.

By the end of this article, you will be able to trace a single stablecoin from the moment it is created to the moment it ceases to exist. No gaps.

Why Does Every Stablecoin Have a Birth and a Death?

Physical cash circulates indefinitely until someone physically destroys it. A stablecoin does not work that way. Every token in circulation today was minted at a specific moment against a specific deposit. Every token that has ever been redeemed was permanently destroyed in the process.

This is the minting and burning lifecycle. It is not a side feature of stablecoins. It is the mechanical heartbeat that keeps the peg intact, and if you cannot trace it, you cannot properly assess the risk of any stablecoin you are building on.

How Is a Stablecoin Minted, Step by Step?

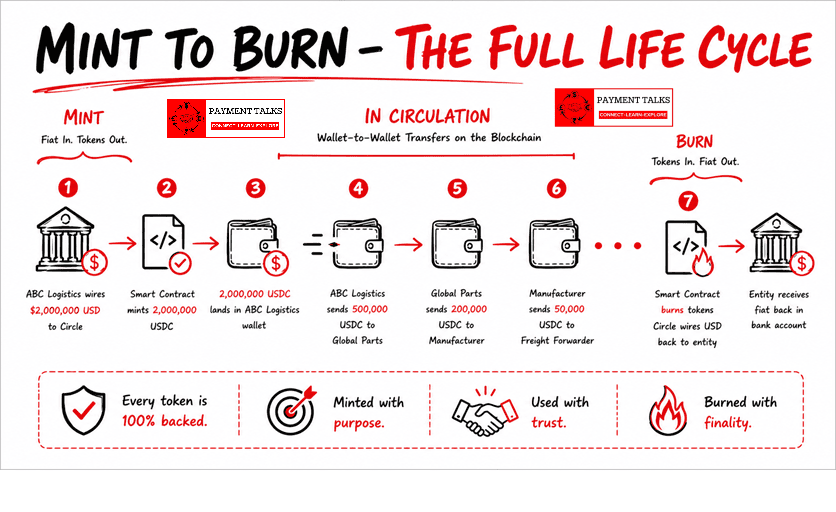

Minting is the process of creating new stablecoin tokens. It always, without exception, requires that an equivalent amount of real-world value be deposited with the issuer first.

Take a real-shaped scenario. ABC Logistics Ltd is a UK-based freight company. Their treasury team wants to hold USDC for cross-border supplier payments across Asia. They convert $2,000,000 USD into USDC.

The Minting Process, Step by Step

- ABC Logistics wires $2,000,000 USD from their corporate bank account to Circle’s designated bank account. Standard fiat wire, standard banking channels.

- Circle receives the funds and, before anything touches the blockchain, confirms settlement, verifies ABC Logistics’ KYC profile, runs AML checks on the source of funds, and screens against sanctions lists.

- Circle’s systems instruct the USDC smart contract deployed on the relevant chain: create 2,000,000 new USDC tokens and deposit them to ABC Logistics’ wallet address.

- The smart contract executes. 2,000,000 USDC tokens are created. They did not exist a second ago. The creation event is permanently recorded on the blockchain, visible and verifiable by anyone.

- The freshly minted tokens land in ABC Logistics’ wallet. Their balance rises by exactly 2,000,000 USDC. The $2,000,000 now sits in Circle’s bank account, backing every one of those tokens.

ABC Logistics (USD 2M) → Circle (KYC + AML check) → Smart Contract (mints 2M USDC) → ABC Logistics Wallet

This compliance gate is non-negotiable. USDC cannot be minted for any entity that has not cleared Circle’s onboarding. That is the point architects most often miss: USDC is not anonymous fiat. Every minting event is tied to a verified entity.

What Happens Once a Stablecoin Is Circulating?

ABC Logistics now holds 2,000,000 USDC. They send $500,000 USDC to a supplier in Singapore, Global Parts Pvt Ltd. That is a blockchain transaction. The tokens move from ABC’s wallet to Global Parts’ wallet. Circle is not involved. No bank is involved. It settles peer-to-peer in seconds.

Global Parts might then send $200,000 USDC to their component manufacturer in Taiwan. That manufacturer might use $50,000 USDC to pay a freight forwarder. Each hop is a blockchain transaction: fast, cheap, borderless.

Here is how I put it on the whiteboard: draw two lines. One line is the dollar, sitting completely still inside Circle’s bank account. The other line is the token, moving constantly across a blockchain. The two are permanently linked, but only one of them is actually moving when a payment happens. The fiat only moves again when someone redeems, meaning burns, their stablecoins.

It is a similar discipline to double-entry accounting in payments: two sides of value that must always reconcile back to the same total, except here one side sits on a bank ledger and the other moves on a public chain.

How Is a Stablecoin Burned, Step by Step?

Burning is the process of destroying stablecoin tokens in exchange for fiat currency. When an entity wants to exit the stablecoin ecosystem and receive real dollars back, they initiate a redemption, and that redemption triggers a burn.

Global Parts has accumulated 800,000 USDC through payments from ABC Logistics and other customers. They want it back as Singapore Dollars to pay local expenses. The USDC-to-SGD conversion itself runs through a licensed exchange, which we cover when comparing stablecoin rails to SWIFT and SEPA in Part 3. For now, follow the burn of USDC back to USD.

The Burning Process, Step by Step

- Global Parts transfers 800,000 USDC to Circle’s official redemption wallet address. Standard blockchain transaction.

- Circle confirms receipt in the redemption wallet and verifies Global Parts’ identity and compliance status.

- Circle instructs the smart contract to burn the 800,000 tokens. They are permanently destroyed. Not archived, not moved. Total USDC supply drops by exactly 800,000.

- Circle wires $800,000 USD from their bank account to Global Parts’ designated bank account.

Global Parts (800K USDC) → Circle Redemption Wallet → Smart Contract (burns 800K USDC) → Circle Bank → Global Parts (USD 800K)

The elegant result: total USDC in circulation always equals total USD, and equivalent assets, sitting in Circle’s reserves. The system is self-balancing by design.

What Actually Backs a Stablecoin?

The reserve is the single most important concept in stablecoin trust. The entire credibility of a fiat-backed stablecoin rests on the quality, liquidity, and transparency of what sits behind it.

What Counts as a Reserve?

Reserves are not all the same. Here is the spectrum, most trusted to least trusted.

| Reserve Asset | Description | Liquidity | Risk Level |

| Cash in regulated banks | Direct USD deposits at US banks | Highest, immediately available | Low (bank failure risk) |

| US Treasury Bills | Short-term US government debt (90 days or less) | Very high, near-cash | Very low |

| Money Market Funds | Pools of short-term, high-quality instruments | High | Low |

| Reverse Repos | Short-term secured lending to banks | High | Low to medium |

| Corporate Bonds | Debt issued by corporations | Medium | Medium |

| Commercial Paper | Short-term unsecured corporate debt | Medium | Medium-high |

| Other crypto assets | Bitcoin, Ether, and similar | Variable | High |

The further down that table you go, the less stable and transparent the reserve becomes. That is precisely why USDT faced years of criticism: its reserve composition historically included commercial paper and other less liquid instruments, with limited transparency.

How Circle Manages USDC Reserves

Circle publishes monthly attestation reports prepared by Grant Thornton LLP. As of the most recent published attestations, USDC reserves consist of cash held at regulated US financial institutions and US Treasury obligations, meaning T-Bills and reverse repo agreements backed by US Treasuries.

No commercial paper, no corporate bonds, no cryptocurrency. But there is a distinction worth holding onto: an attestation confirms that reserves existed at the point in time assessed. A full audit examines a company’s financial controls in depth. Regulators are pushing issuers to close that gap.

The SVB Moment: Why Reserve Composition Matters in a Crisis

In March 2023, Silicon Valley Bank collapsed, the second-largest bank failure in US history. Circle had roughly $3.3 billion of USDC reserves deposited at SVB.

USDC briefly de-pegged to about $0.87. Billions in redemptions were requested over a single weekend. Circle confirmed the exposure was contained and that other reserve assets would cover redemptions even in a worst case. The US government stepped in to guarantee SVB deposits, and the peg recovered to $1.00 within 48 hours.

The lesson for architects: even the best-managed fiat-backed stablecoin carries residual risk from the banking system underneath it. Reserve diversification across multiple banks and multiple asset types is a practice worth verifying, not assuming, when you select a stablecoin for enterprise use.

Common trap I see in early-stage evaluations: teams pick a blockchain purely on speed and cost, then never ask what actually backs the stablecoin they intend to settle in, or what the redemption terms look like under stress. Reserve quality deserves the same due diligence as counterparty risk on a correspondent banking relationship.

For the regulatory backdrop shaping reserve requirements under MiCA and the GENIUS Act, see Stablecoin Risks and Regulation, Part 4 of this series.

Which Blockchain Should a Stablecoin Actually Run On?

A stablecoin does not exist in one place. It exists as a record on a distributed ledger, a blockchain. That infrastructure is what lets stablecoins move without a central intermediary processing the transfer.

The blockchain choice determines transaction speed, cost, finality time, and ecosystem compatibility. That makes it an architecture decision, not a technical afterthought.

Key Blockchains for Stablecoin Payments

| Blockchain | Speed | Typical Cost | Time to Finality | Common Stablecoins |

| Ethereum | ~15 TPS | $2-$50 (variable gas) | ~15 sec (probabilistic) | USDC, USDT, DAI |

| Solana | ~65,000 TPS | < $0.001 | ~400 ms | USDC, USDT |

| Stellar | ~1,000 TPS | ~$0.00001 | 3-5 sec | USDC |

| Tron | ~2,000 TPS | ~$1 flat | ~3 sec | USDT (dominant) |

| Polygon | ~7,000 TPS | < $0.01 | ~2 sec | USDC, USDT |

| Base | ~2,000 TPS | < $0.01 | ~2 sec | USDC |

Ethereum is the most established and most widely supported chain, but variable gas fees can spike hard during network congestion, which rules it out for high-frequency, low-value payments. Solana has become the preferred chain for stablecoin payment applications that need both speed and near-zero cost, closer in feel to a traditional payment switch than anything else in crypto. Stellar was purpose-built for cross-border payments and remittance corridors. Tron carries more USDT volume than any other chain, concentrated in Asia and exchange-to-exchange flows, though it draws more regulatory scrutiny than Ethereum or Solana.

What Does Transaction Finality Actually Mean?

In traditional banking, finality is a legal and operational concept: a payment is final when it cannot be reversed or recalled. On a blockchain, finality is the point at which a transaction is irreversible and mathematically confirmed.

- Probabilistic finality (Ethereum): the transaction gets more secure with every new block added after it. After roughly 12 confirmations, about 3 minutes, reversal is practically impossible.

- Deterministic finality (Solana, Stellar): finality happens within a single confirmed block. No ambiguity.

For architects, finality time drives reconciliation design, confirmation workflows, and the risk window between initiation and irreversibility.

What Do Smart Contracts Actually Control?

If the blockchain is the railway, the smart contract is the rulebook governing every train on it. A smart contract is self-executing code deployed on-chain. For stablecoins, it defines and enforces the total token supply, who can mint, who can burn, transfer logic, and compliance controls including blacklisting.

The Blacklist Function: What Every Payments Professional Must Know

Circle’s USDC smart contract can blacklist any wallet address. A blacklisted address cannot send or receive USDC.

- When law enforcement, including the FBI and DOJ, identifies wallets tied to sanctions violations, hacks, or criminal activity, Circle has blacklisted those addresses at government request.

- After the $620 million Ronin bridge hack in March 2022, Circle froze $750,000 in USDC held by the attacker’s addresses within hours.

This is a significant architectural fact: USDC is not censorship-resistant the way Bitcoin is. The issuer retains the ability to intervene. For most regulated payment use cases that is a feature, not a bug, it shows USDC operating within the legal system. Anyone building decentralized applications or privacy-sensitive systems needs to internalize that reality before, not after, they design around it.

Where Do Institutions Actually Hold Stablecoins?

Every stablecoin balance lives in a wallet. A wallet does not literally hold tokens, it holds the cryptographic keys that prove ownership and authorize transactions.

- Public Key (Wallet Address): like a bank account number. Share it freely, it lets others send you tokens. A typical Ethereum address looks like 0x742d35Cc6634C0532925a3b844Bc454e4438f44e.

- Private Key: like a PIN combined with a legal signature. Whoever holds it controls the wallet. Lost or stolen, the tokens are gone permanently.

Custodial vs Non-Custodial Wallets

This split is fundamental for enterprise payments architecture, and it maps closely onto a distinction payments professionals already know from correspondent banking and nostro and vostro account structures: who actually controls the asset, versus who merely has visibility over it.

| Feature | Custodial Wallet | Non-Custodial Wallet |

| Who holds the private key | Third-party custodian (Fireblocks, BitGo) | The wallet owner |

| Analogy | Like a bank account, custodian manages it | Like cash in a safe, you manage it |

| Recovery if key lost | Custodian can help restore access | Impossible, funds permanently lost |

| Compliance controls | Built in (KYC, AML, sanctions screening) | Must be self-implemented |

| Use case | Enterprise B2B, regulated financial services | DeFi, peer-to-peer, advanced users |

| Risk profile | Custodian insolvency or failure | Self-custody errors, key loss |

For enterprise payments, custodial wallets are almost always the right choice. They abstract private key complexity, integrate compliance workflows, provide institutional-grade security through Hardware Security Modules, and support multi-signature authorization for high-value transactions. Leading institutional custodians include Fireblocks, BitGo, Anchorage Digital, Copper, and increasingly traditional players like BNY Mellon and Fidelity Digital Assets.

Multi-Signature Wallets

For high-value institutional transfers, one private key is not enough from a controls standpoint. Multi-signature wallets require approval from multiple authorized parties before a transaction executes. A payment over $1,000,000 might need sign-off from both the treasury manager and the CFO’s key before it moves. That mirrors the dual-authorization, maker-checker controls already standard in traditional payment systems, and it belongs in any enterprise stablecoin architecture.

For the design patterns that turn these building blocks into a working enterprise system, see How to Architect a Stablecoin Payment System, Part 5.

What Does a Full Mint-to-Burn Lifecycle Look Like in Practice?

Trace the complete lifecycle in a single scenario.

- Monday, 9:00 AM: ABC Logistics deposits $5,000,000 with Circle. KYC clears. The smart contract mints 5,000,000 USDC. ABC Logistics’ wallet balance: 5,000,000 USDC.

- Monday, 9:45 AM: ABC sends 1,200,000 USDC to Supplier A in Singapore. Solana settles it in 400 milliseconds.

- Tuesday, 2:00 PM: Supplier A sends 400,000 USDC to their freight forwarder in Malaysia. Settled in seconds.

- Wednesday, 10:00 AM: ABC sends 800,000 USDC to Supplier B in Vietnam.

- Thursday, 3:00 PM: Supplier A converts 800,000 USDC to SGD via a licensed exchange. The exchange now holds the USDC, no burn yet, Supplier A receives SGD in their bank account.

- Friday, 5:00 PM: The exchange aggregates redemption requests and redeems 2,000,000 USDC from Circle. The smart contract burns 2,000,000 USDC. Circle wires $2,000,000 USD to the exchange’s bank account.

Total USDC in circulation from ABC Logistics’ original mint: now 3,000,000, backed by $3,000,000 in Circle’s reserve. Perfectly balanced, at every moment.

Visual : Full Mint-to-Burn Lifecycle

Common Questions About Stablecoin Mechanics

What happens if Circle goes bankrupt? Do I lose my USDC?

Circle holds reserves in bankruptcy-remote custodial arrangements, meaning the reserves are legally separate from Circle’s operating assets and cannot be claimed by Circle’s creditors in insolvency. That said, legal treatment of stablecoin holders in bankruptcy is still evolving in most jurisdictions. Under MiCA in the EU, e-money token holders have clear claims on reserves. In the US, clarity is emerging through the GENIUS Act. Assess issuer solvency risk as part of any enterprise deployment.

If I send USDC to the wrong wallet address, can I get it back?

No. A blockchain transaction to an incorrect address is irreversible. There is no equivalent of a SWIFT recall message or a SEPA return transaction. Pre-send address validation is a non-negotiable design requirement in any stablecoin payment system. Some platforms, including Circle’s payment APIs, include address confirmation flows. Treat those as a minimum baseline control, not a full safeguard.

Can USDC be used as collateral for loans?

Yes. Using stablecoins as collateral in lending protocols is one of the significant DeFi use cases. For enterprise treasury architects, that opens on-chain yield generation on idle USDC balances, a topic that goes beyond this article but is worth flagging for advanced stablecoin architecture discussions.

What is the difference between minting a stablecoin and buying one on an exchange?

Minting creates new tokens against a fresh fiat deposit with the issuer directly. Buying on an exchange moves existing tokens from one holder to another, no new supply is created and no smart contract mint function is called. Most day-to-day users only ever buy on exchanges. Minting and burning happen at the issuer level, usually institutional treasury desks and large market makers.

Why can’t a stablecoin issuer just print more supply without a deposit?

Because the smart contract’s mint function is permissioned and tied to Circle’s internal ledger of verified deposits, not an arbitrary decision. Printing supply without backing would break the 1:1 reserve promise instantly and would be visible on-chain to anyone auditing total supply against attested reserves. That transparency is precisely what fiat-backed stablecoins are designed to provide over unbacked alternatives.

How can I verify a stablecoin’s reserves without waiting for the monthly attestation?

Total token supply is public and verifiable on-chain in real time. Reserve composition and custody, however, are only as current as the issuer’s last attestation or audit. Some issuers now publish more frequent or near-real-time reserve dashboards.

Key Takeaways

- A fiat-backed stablecoin is minted only when equivalent fiat is deposited with the issuer, and burned when it is redeemed. The peg is maintained mechanically, not by trust alone.

- Reserve quality is the trust anchor. Cash and US Treasury Bills are the gold standard. Commercial paper and mixed assets introduce risk. Always check what actually backs the stablecoin you are designing around.

- Blockchain choice matters: Solana for speed and volume, Ethereum for ecosystem depth, Stellar for payments-native design, Tron for USDT flows. Each carries different cost, speed, and finality characteristics.

- Smart contracts govern stablecoin behavior, including compliance functions like address blacklisting. USDC is not censorship-resistant, and for regulated payments that is appropriate.

- For enterprise payments, custodial wallets with multi-signature controls are the correct architecture. Treat private key management with the same seriousness as master passwords in traditional banking systems.

What’s Next

You now understand the complete lifecycle of a stablecoin, from creation, through circulation, to destruction. You understand the blockchain layer, the reserve mechanics, and the wallet infrastructure.

But understanding stablecoin mechanics in isolation is only half the picture. The real question for payments professionals is how this actually plugs into real-world payment flows.

In Part 3 of this series, we compare stablecoin payment rails directly against SWIFT and SEPA using a real cross-border payment scenario. Same payment, two entirely different journeys.

For how these mechanics map onto ISO 20022 messaging, see Stablecoins & ISO 20022. For how stablecoins compare to central bank digital currencies, see CBDCs Explained.