Ask anyone in cross-border payments to explain the difference between a correspondent bank and an intermediary bank. Most will give you a confident answer. Push a little harder and the confidence starts to crack.

Both terms appear in the same payment chain. Both can refer to the same bank. Neither is wrong in the right context. The problem is that practitioners use them without distinguishing which context they are in: the relationship context or the transaction context. Juniors pick up the loose usage and carry it forward. Confusion compounds.

These are not the same thing. They are also not two different banks. The truth sits in the middle, and once you see it, you will not confuse these terms again.

Why Does This Confusion Exist?

Both terms appear in the same payment chain, and in most cross-border payments they can refer to the same bank. That overlap is real. The confusion starts when practitioners treat the overlap as the whole picture.

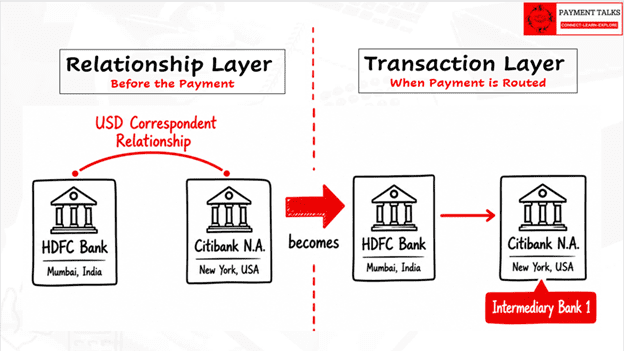

Correspondent banking describes a standing arrangement between two financial institutions. It is infrastructure built before any payment moves. Intermediary banking describes a role a bank plays in a specific payment. It is a layer that activates only when a payment is routed.

One term describes what you built. The other describes what the payment uses. The bank in question is often the same. The lens is completely different.

What Is a Correspondent Bank?

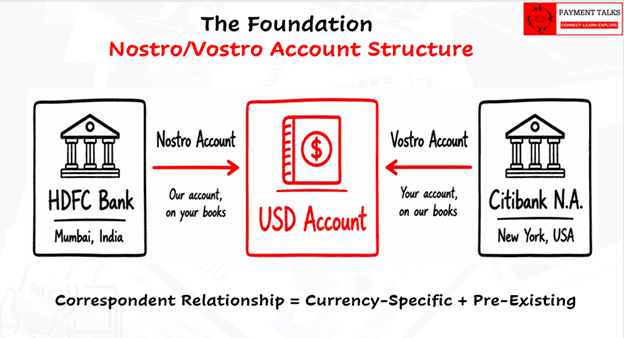

A correspondent bank is a financial institution that holds an account on behalf of another financial institution — its respondent — to provide access to a currency, market, or payment system the respondent cannot reach directly.

The foundation of this relationship is the Nostro and Vostro account structure. From the respondent bank’s perspective, the account held at the correspondent is the Nostro: our account, on your books. From the correspondent’s perspective, the same account is a Vostro: your account, on our books. Two names, one account, two perspectives on the same relationship.

The Nostro/Vostro account is the foundation of every correspondent banking relationship.

One point that gets missed in most explanations: correspondent banking relationships are currency-specific. Bank A can be Bank B’s EUR correspondent without being their USD or GBP correspondent. These are separate formal agreements, each denominated in a specific currency, maintained independently.

When routing a payment, the currency of the transaction determines which correspondent relationship is relevant. A bank holding only a USD correspondent relationship cannot serve as intermediary for a EUR payment. The currency filter applies at every step of the chain.

This relationship exists before any payment is initiated. It is banking infrastructure, not a transaction concept.

What Is an Intermediary Bank?

An intermediary bank is any bank placed between the Debtor Agent and the Creditor Agent in the routing chain of a specific payment. It is a role, not a relationship.

The defining characteristic: the intermediary bank has a dedicated placeholder in the ISO 20022 payment message. Routing must be explicitly instructed per transaction. The choice of which bank fills that role is currency-driven. Only a bank holding the relevant currency correspondent relationship can route that payment onward.

No direct standing agreement is required between the originating bank and the intermediary. What matters is the bank’s position in the chain for that specific transaction.

Correspondent Bank vs Intermediary Bank at a Glance

| Dimension | Correspondent Bank | Intermediary Bank |

| Nature | Standing relationship | Transaction role |

| Defined by | Bilateral agreement + Nostro/Vostro account | Position in a specific payment chain |

| Currency link | Currency-specific. One relationship per currency. | Driven by payment currency. Currency must match. |

| Duration | Ongoing, pre-existing | Per-transaction |

| In ISO 20022 | Implicit. Not a named message field. | IntrmyAgt1/2/3 in pacs.008 |

How Does a Correspondent Bank Become an Intermediary Bank?

This is where the concept clicks.

When a Debtor Agent initiates a cross-border payment, it needs to build a path from its side to the Creditor Agent. It does this in two steps:

- It selects its own currency correspondent — the bank where it holds an account in the payment currency — as the first routing hop.

- It consults SSI reference files to identify the Creditor Agent’s currency correspondent and places that bank as the next hop in the chain.

The moment both correspondent banks are placed into the payment chain, they become intermediary banks for that transaction.

The correspondent relationship is the reason a bank is chosen. The intermediary role is the expression of that choice in the payment message.

The correspondent relationship is the reason a bank is chosen. The currency match is the filter. The intermediary role is the expression of that choice in the payment message.

Same bank. Two lenses.

What Are SSI Files and How Are They Used?

SSI stands for Standard Settlement Instructions. These are reference data files containing the currency correspondents of financial institutions worldwide, structured by currency.

For each financial institution in the file, SSI records which bank is their USD correspondent, their EUR correspondent, their GBP correspondent — across every currency they operate in. These banks are called currency correspondents precisely because the relationship is always tied to a specific currency.

SSI files are maintained by two global institutions. SWIFT publishes the SWIFT Ref database. LexisNexis maintains Acuity. The responsibility for accuracy and timely updates lies with these institutions. Banks consume the data as reference input when constructing payment chains.

When a Debtor Agent needs to route a payment, it queries the SSI file to find the Creditor Agent’s currency correspondent for the payment currency. That correspondent is placed in the chain as the second intermediary hop.

Note: Full payment chain construction from SSI data is a specialist discipline involving field-by-field interpretation, currency matching, and routing logic. That subject deserves its own treatment and is covered in a dedicated PaymentTalks article later.

What Happens in a Real Cross-Border Payment?

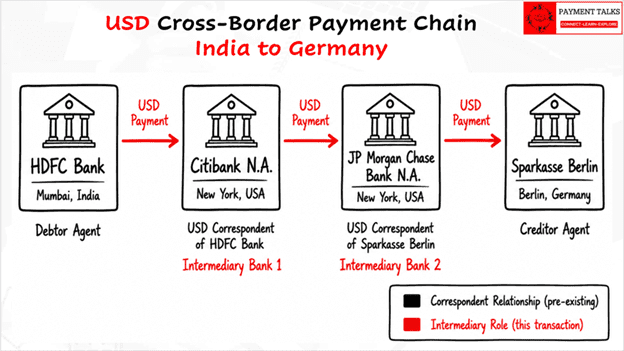

Here is a concrete example. A corporate client in India wants to pay a supplier in Germany. The payment currency is USD.

The Parties

- Debtor: Indian corporate client

- Debtor Agent: HDFC Bank, Mumbai

- Payment currency: USD

- Creditor Agent: Sparkasse Berlin, Germany

- Creditor: German supplier

Building the Payment Chain

- HDFC Bank identifies its USD correspondent. HDFC Bank holds a USD account with Citibank N.A., New York. That is the established correspondent relationship for USD.

- HDFC Bank queries the SSI reference file for Sparkasse Berlin’s USD correspondent. The file returns JP Morgan Chase Bank N.A., New York.

- HDFC Bank constructs the payment chain: HDFC Bank to Citibank N.A., New York to JP Morgan Chase Bank N.A., New York to Sparkasse Berlin.

Both Lenses Applied

- Citibank N.A. is HDFC Bank’s USD correspondent (relationship lens) and the first intermediary bank in this payment (transaction lens).

- JP Morgan Chase Bank N.A. is Sparkasse Berlin’s USD correspondent (relationship lens) and the second intermediary bank in this payment (transaction lens).

Neither HDFC Bank nor Sparkasse Berlin had a direct account relationship with each other. The correspondent networks of both banks bridged the gap, and in doing so became the intermediary banks for this payment.

The correspondent banks of the Debtor Agent and Creditor Agent fill the intermediary roles when placed in the payment chain.

How Does This Appear in an ISO 20022 pacs.008 Message?

For a full breakdown of every agent and party field in ISO 20022 messages, refer to the PaymentTalks article on Agents and Parties. This section focuses on how the correspondent-to-intermediary relationship shows up specifically in the message structure.

Static vs Dynamic Fields

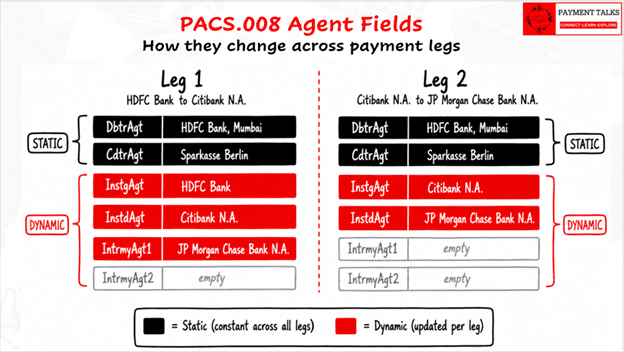

The pacs.008 message has two categories of agent fields.

Static fields remain unchanged across every leg of the payment:

- DbtrAgt (Debtor Agent): HDFC Bank, Mumbai. Constant throughout all legs.

- CdtrAgt (Creditor Agent): Sparkasse Berlin. Constant throughout all legs.

Dynamic fields are updated per leg as the payment moves through the chain:

- InstgAgt (Instructing Agent): the sender of that specific leg.

- InstdAgt (Instructed Agent): the receiver of that specific leg.

- IntrmyAgt1/2/3 (Intermediary Agents): the remaining forward-looking hops in the chain, progressively removed as each hop is consumed.

The Fields Across Each Leg

| Field | Leg 1: HDFC Bank to Citibank N.A. | Leg 2: Citibank N.A. to JP Morgan Chase Bank N.A. |

| DbtrAgt (static) | HDFC Bank, Mumbai | HDFC Bank, Mumbai |

| CdtrAgt (static) | Sparkasse Berlin | Sparkasse Berlin |

| InstgAgt (dynamic) | HDFC Bank, Mumbai | Citibank N.A., New York |

| InstdAgt (dynamic) | Citibank N.A., New York | JP Morgan Chase Bank N.A., New York |

| IntrmyAgt1 (dynamic) | JP Morgan Chase Bank N.A., New York | (empty — next stop is CdtrAgt) |

| IntrmyAgt2 | (empty) | (empty) |

The correspondent banks fill the IntrmyAgt fields. As the payment moves through each leg, those fields are updated to show only the hops still ahead. By Leg 2, there are no more intermediary agents. The next stop is the Creditor Agent itself.

IntrmyAgt fields are dynamic. They reflect only the remaining forward hops in each payment leg, not the full original chain.

A note for teams migrating from SWIFT MT: a common mistake is treating IntrmyAgt as a static configuration field, populating it once for the full chain and leaving it unchanged. That breaks the payment chain. These fields are dynamic and must reflect only the remaining forward hops at each leg. This is one of the most frequent sources of incorrect test data in ISO 20022 implementations, particularly for teams that built expertise on MT messages and are now navigating ISO 20022 agent fields for the first time.

Why Does This Distinction Matter in Practice?

Correspondent selection and intermediary routing are two distinct operational responsibilities. They need to be managed separately.

Correspondent selection is a strategic decision. It involves relationship management, account opening, credit line negotiations, FX agreements, compliance assessments, and cost modelling. This sits with Treasury and Correspondent Banking teams.

Intermediary routing is an operational decision. It involves SSI data accuracy, currency matching, chain construction, and payment chain validation. This sits with Payment Operations and the payment engine.

Two specific failure modes trace directly back to this confusion:

- Currency mismatch: a bank that is your USD correspondent cannot serve as intermediary for a EUR payment. The relationship is currency-specific and so is the routing. Placing the wrong currency correspondent in the chain causes the payment to fail, return, or require costly manual repair.

- SSI data quality: SSI files must be current and accurate. Stale data places the wrong intermediary in the chain. One wrong field in the payment message can fail the entire transaction.

The two layers must be governed separately. Conflating them at the design or operational level creates risk on both sides.

The Complete Picture

Both terms are valid. Neither is wrong. What matters is knowing which lens you are looking through.

Correspondent bank describes the relationship you built: a bilateral, currency-specific account arrangement that exists before any payment moves. Intermediary bank describes the role that correspondent plays when placed in the chain to route a specific payment.

Same bank. One relationship lens. One transaction lens. The confusion ends when you stop asking which term is correct and start asking which context you are in.

Frequently Asked Questions

What is the difference between a correspondent bank and an intermediary bank?

A correspondent bank is a financial institution with which another bank holds a formal, currency-specific, account-based relationship. An intermediary bank is any bank placed between the Debtor Agent and Creditor Agent to route a specific payment. In most cross-border payments, the correspondent banks of both the Debtor Agent and Creditor Agent fill the intermediary roles for that transaction.

Can a bank be both a correspondent bank and an intermediary bank at the same time?

Yes. In most cross-border payments this is exactly what happens. When a bank is placed in the payment chain because of an existing correspondent relationship, it is simultaneously a correspondent bank by relationship and an intermediary bank by role in that transaction.

Why are correspondent banking relationships currency-specific?

Because they are built on Nostro/Vostro accounts denominated in a specific currency. A bank can hold USD accounts with one institution and EUR accounts with a different institution. Only the correspondent holding the relevant currency relationship can serve as intermediary for a payment in that currency.

What are SSI files used for in cross-border payments?

SSI (Standard Settlement Instructions) files contain the currency correspondents of financial institutions worldwide, structured by currency. Banks use SSI data to identify the Creditor Agent’s currency correspondent when constructing the payment chain. They are maintained by SWIFT (SWIFT Ref) and LexisNexis (Acuity).

How is an intermediary bank represented in an ISO 20022 pacs.008 message?

Intermediary banks are placed in the IntrmyAgt1, IntrmyAgt2, or IntrmyAgt3 fields. These are dynamic fields that are updated per payment leg. They hold only the remaining forward-looking hops. As each hop is consumed, the corresponding field is removed from subsequent legs.

What happens if the wrong intermediary bank is placed in a payment chain?

The payment will likely be returned, delayed, or require manual repair. This most commonly results from incorrect or stale SSI data, or from placing a correspondent with the wrong currency relationship in the chain for a given payment currency.

What is the difference between IntrmyAgt and InstgAgt/InstdAgt in pacs.008?

IntrmyAgt fields hold the remaining forward routing hops — the banks still ahead in the chain. InstgAgt and InstdAgt identify who is sending and receiving that specific leg right now. Both are dynamic, but serve different purposes: IntrmyAgt describes what is ahead; InstgAgt and InstdAgt describe who is transacting at this step.