Here is the most important thing about pacs.008 initiation: by the time a pacs.008 exists, the hard work is already done. This is not a warm-up statement. It is the foundational principle of the entire pacs.008 lifecycle. If you start learning pacs.008 at the XML, you are starting at the wrong end of the story.

The pacs.008 is not where a payment begins. It is where a payment instruction, enriched, validated, and approved, becomes a network message. Understanding pacs.008 initiation means understanding everything the bank does before the first XML element is written.

This is Part 1 of the PaymentTalks pacs.008 Masterclass Series. We follow Claudia, a corporate treasurer at a Munich manufacturing firm, as she initiates a EUR 50,000 payment to her Italian supplier. The full payment lifecycle spans eight parts. Part 1 covers everything that happens before any message exists.

Claudia’s payment:

- Amount: EUR 50,000

- Creditor: Acme Engineering S.r.l., Milan

- IBAN: IT60 X054 2811 1010 0000 0123 456

- Purpose: INV-2024-08821

- Value date: Today

She hits submit. What happens next has nothing to do with XML.

What actually triggers a pacs.008?

Every pacs.008 begins with a human decision: someone wants to move money. That person might be a corporate treasurer, a business owner, or an automated system running on their behalf. The bank’s role at initiation is to receive that intent, validate it, and normalise it into an internal working record. The pacs.008 is the output of that process. Not the input. Not the starting gun. The conclusion.

This distinction matters more than it seems. Teams that build payment engines treating the pacs.008 as the starting artifact consistently build fragile systems. They generate messages before compliance clears. They assign UETRs at intake. They write enrichment data into fields that should be immutable. All of these patterns come from the same root misunderstanding: that the pacs.008 is where payment processing begins.

Claudia submitted through a corporate banking portal. At the point of submission, the bank has received her intent. It has not done enrichment, compliance screening, routing, UETR assignment, or message generation. None of that exists yet. What exists is an instruction that needs to be processed.

What elements of customer intent must the bank capture and preserve?

Every payment instruction contains elements of customer intent. Once captured, the bank’s obligation is to carry them unchanged through the entire payment lifecycle. These elements are not fields to enrich or modify. They are the instruction itself.

The list below covers the most operationally significant elements. It is not a closed list, and not all elements are mandatory for every payment type. What is mandatory is the principle: whatever the customer provides as intent, the bank does not change it.

- Debtor identity: the legal entity initiating the payment. This includes the debtor’s legal name, their account number at their bank, and the bank itself (identified by BIC). The bank cannot substitute a different debtor account or entity.

- Creditor identity: the beneficiary of the payment. This includes the creditor’s legal name, their account details (IBAN where applicable, or account number and bank code otherwise), and their bank (BIC or national identifier if provided). Claudia provided an IBAN for Acme Engineering, from which the bank will identify the creditor’s bank.

- Amount (InstructedAmount): EUR 50,000. Not EUR 49,995. Not EUR 50,007. EUR 50,000 exactly. This is the legal record of what the customer instructed. Any system that modifies this value, for any reason, has introduced a bug.

- Currency: EUR. The customer chose this. The bank cannot silently convert to another currency without explicit customer authorisation.

- Pre-agreed exchange rate (if applicable): if the customer has locked an FX rate before submitting the instruction, that rate is customer intent. It cannot be overridden by the bank’s processing systems. The exchange rate the customer agreed to is what they expect to be applied.

- Value date (ReqdExctnDt): Claudia wants this paid today. The bank’s actual settlement date is a derived field. ReqdExctnDt is the customer’s expectation and is immutable.

- Purpose (when provided): a payment purpose code indicates the reason for the payment. When the customer provides this, it is customer intent and must be preserved. It is not mandatory for all payment types.

- Remittance information (when provided): INV-2024-08821. This is what Acme Engineering needs to reconcile their accounts receivable. When provided, it is customer intent and must be preserved end to end. It is not mandatory for every payment, but losing it when provided causes real operational damage on the beneficiary’s side.

- Urgency and priority (when provided): the customer may specify normal, urgent, or scheduled processing. When specified, this is customer intent. It is not always a mandatory field. Some payment channels do not surface it.

This list covers the most significant elements of customer intent. It is illustrative, not exhaustive. The specific fields present and which are mandatory vary by payment type, channel, scheme, and jurisdiction. The underlying principle holds regardless: the bank captures customer intent and preserves it unchanged.

How does the payment instruction reach the bank?

Customer intent arrives through multiple initiation channels. The channel determines the format of delivery. The intent itself does not change across channels.

| Channel | Native Format | Structure |

| Corporate Treasury System | pain.001 XML | ISO 20022 pain.001 |

| Open Banking / REST API | JSON or XML | pain.001-aligned or proprietary |

| ERP Systems (SAP, Oracle, Kyriba) | Proprietary + pain.001 export | Proprietary or ISO 20022 |

| Mobile / Web Portal | HTML form submission | Non-standard, bank-specific |

| E-Forms / Web Application Forms | Form POST / JSON | Bank-defined, mapped to canonical |

| Excel / Spreadsheet Upload | XLS, XLSX, CSV | Bank-defined column mapping |

| Host-to-Host | MT, CSV, fixed-width, EDIFACT | SWIFT FIN or legacy |

| Branch System | Teller form entry | Core banking native |

| Legacy SWIFT MT103 | SWIFT FIN MT103 | SWIFT pre-ISO format |

Common initiation channels with their typical delivery formats and logical structures. This list is illustrative, not exhaustive.

These are the most commonly implemented channels. The list is not closed. Banks continue to add new channels as technology evolves, and each new channel requires only an input adapter to the canonical layer, not a change to the payment engine.

Claudia uses a corporate banking portal. Her intent is captured in an HTML form. The submission is an HTTP POST. There is no pain.001 XML at this stage. But the bank’s intake layer maps her form fields to the logical structure of a pain.001 in the canonical processing layer.

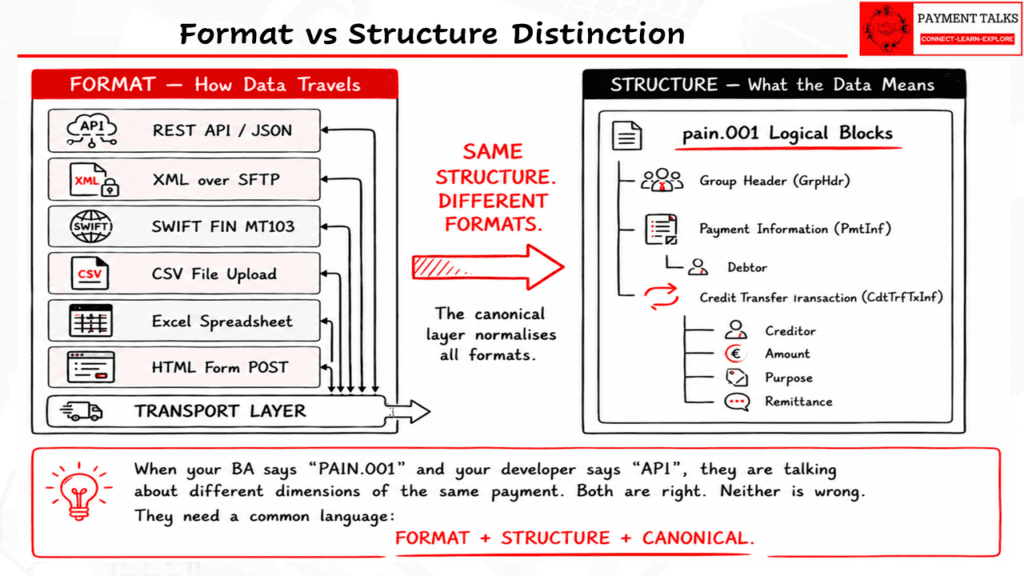

What is the real confusion between format and structure?

This is where many payments professionals, including experienced BAs, have a fundamental gap that prevents them from reasoning clearly about payment system architecture.

Here is the conversation that happens constantly in project teams. A BA says: we process PAIN.001. Their technical colleague says: we use an API. Both are describing the same payment. Both are correct. And both are completely confused about what the other is saying.

The BA is talking about structure. PAIN.001 is an ISO 20022 message structure: a logical organisation of customer payment data into group headers, payment information blocks, and credit transfer transaction information. It defines what the data means.

The technical colleague is talking about format. An API is a transport mechanism. It delivers data, in this case likely JSON, via HTTP. The fact that it is an API says nothing about the structure of the data it carries.

The resolution, which many teams never explicitly articulate: we use a REST API (format) that delivers PAIN.001-structured data (structure) in JSON (format). Three words. Three different dimensions. All simultaneously true.

Format is the transport layer: JSON, XML, CSV, SWIFT FIN MT, an HTML form POST, a fixed-width file from a mainframe, an Excel upload. Format determines how bytes travel from one system to another.

Structure is the semantic layer: the ISO 20022 pain.001 logical blocks, group header, payment information, credit transfer transaction information. Structure determines what the data means and how it relates to other data.

When this distinction is not made explicit, it cascades. Teams build parsers for a specific format thinking they are building for the structure. When a new format arrives, say a mobile app that submits JSON instead of XML, the team discovers the parser is hardcoded. The validator fails. The canonical mapping breaks. A channel that should have been additive becomes a rebuild exercise.

Visual 1: The format-structure distinction: multiple delivery formats, one logical structure, one canonical layer.

Watch the full walkthrough on YouTube

Prefer video? Full walkthrough on the PaymentTalks YouTube channel. Link above.

Why not map pain.001 directly to pacs.008? The case for a canonical instruction

This is the question every BA asks within the first few weeks on a payment project. The ISO standards even publish pain.001-to-pacs.008 mapping specifications. The fields are mapped. The logic is documented. The question is: why add the canonical layer in between?

What breaks without a canonical

Without a canonical, the bank builds a direct pain.001-to-pacs.008 mapper for CBPR+ cross-border payments. It works. Then SEPA SCT is added. Different charge bearer logic. Different settlement method. Different field constraints. The team adds conditional logic to the mapper. Then a domestic RTGS scheme. More conditionals. Then an instant payment scheme. The mapper becomes a maze of conditions, handling multiple schemes simultaneously, with no clean separation between what the customer said and what the bank determined.

Every new scheme means another set of conditionals in the core mapper. Every regulatory change in one scheme risks breaking the logic for another. Now multiply this by the channel problem: the bank also needs to accept JSON from an API, CSV from an ERP, and Excel uploads from SME customers. Without a canonical layer, each format variation adds more branching to an already fragile mapper.

Debugging this in production, where multiple schemes and multiple channels are live simultaneously, is genuinely expensive. The failure mode is not dramatic. It is slow and invisible: payments that almost work, fields that almost populate correctly, scheme rule violations that appear only in edge cases.

What the canonical gives you

The canonical instruction solves this by separating concerns. Customer data is sealed in Layer 1. Bank enrichment populates Layer 2. Scheme-specific rules operate on Layer 2. A new scheme means a new set of enrichment rules for Layer 2. It does not require touching the engine that reads the canonical and generates the pacs.008.

When we built the CBPR+ canonical at Volpay, the architectural decision was to design it as a superset of every field any scheme could require. When the time came to add SEPA SCT, the canonical already had the fields. The SEPA adapter populated them differently, but the payment engine did not change. One engine, one canonical structure, multiple scheme adapters. The PAIN.001 Fields article covers which customer-level fields belong in Layer 1.

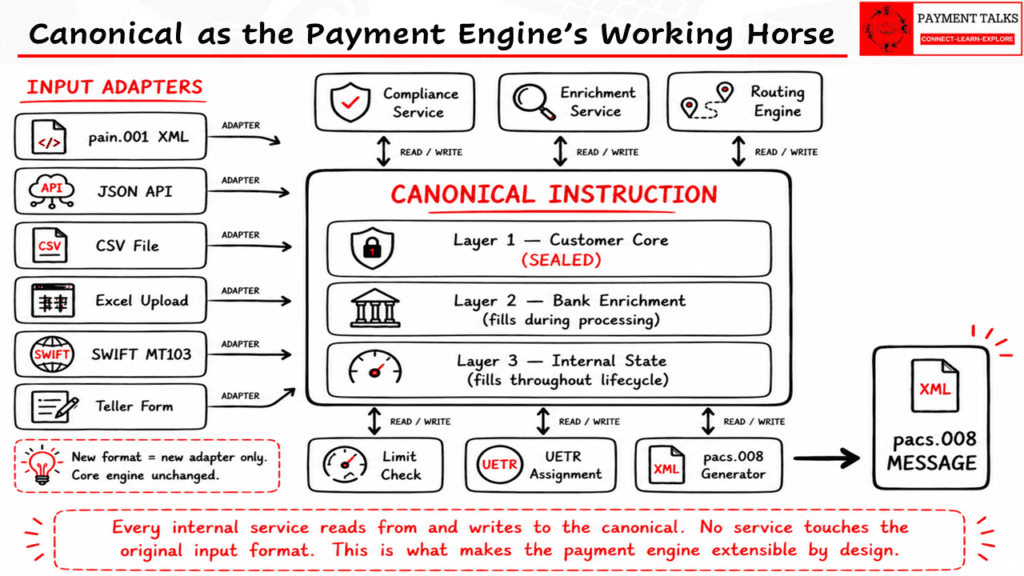

The canonical instruction: the payment engine’s working horse

The canonical is not just a data format or a storage structure. It is the operational backbone of the entire payment engine. Understanding this distinction changes how you design, extend, and debug payment systems.

Every internal process works on the canonical

Every internal processing service, compliance screening, enrichment, routing, limit checking, UETR assignment, reads from the canonical and writes its result back to the canonical. No service receives the original PAIN.001 as input. No service touches a half-built pacs.008. Every service, at every stage, operates on the canonical and only the canonical.

When compliance screening completes, it writes its clearance status to Layer 3 of the canonical. When the routing engine selects a correspondent and determines the settlement method, it writes those values to Layer 2 of the canonical. When UETR assignment runs, it writes the generated UUID4 to Layer 2. The pacs.008 generator reads the completed canonical and produces the message from what is there.

No service needs to know what format the original instruction arrived in. The compliance service does not know or care whether the payment came from an XML upload, a JSON API, or an Excel file. It reads the canonical. That is the only input it receives.

Adding a new format means adding one adapter, nothing else

This is the architectural consequence that matters most in practice.

When a bank wants to support a new initiation channel, say a mobile app that submits payment instructions as JSON in a proprietary format, only one thing needs to be built: an input adapter that maps the incoming JSON to the canonical structure. The compliance service does not change. The routing engine does not change. The enrichment service does not change. The pacs.008 generator does not change.

Add a new format: add one adapter. The core payment engine is untouched.

Contrast this with a direct pain.001-to-pacs.008 architecture. Adding a new input format means touching the mapper, the validator, and potentially the generator, because all three were built with assumptions about the input format baked in.

The canonical is what makes a payment engine extensible by design rather than extensible by effort. This distinction shows up most visibly when a bank is in year two or three of a payment modernisation programme, adding the fourth or fifth scheme or channel. Teams that built on a canonical add new channels in weeks. Teams that did not are still in redesign.

Visual 2: The canonical as the payment engine’s working horse: all processes operate on it, all formats normalise to it.

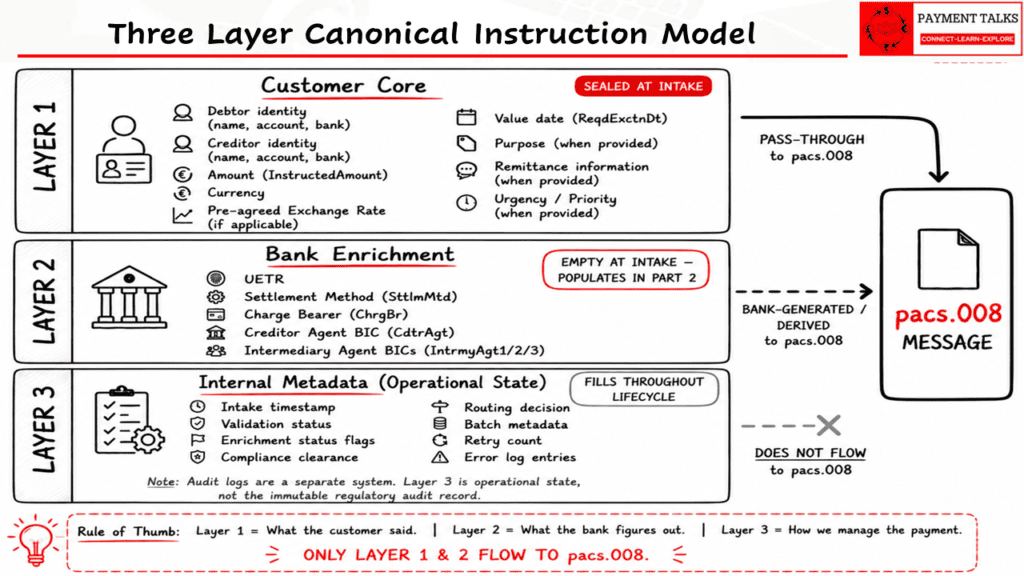

What are the three layers of a canonical instruction?

The canonical instruction has three layers. Each has a distinct owner, a distinct lifecycle, and a distinct relationship to the pacs.008 that will eventually be generated.

Visual 3: The three-layer canonical instruction: Layer 1 sealed at intake, Layer 2 empty until enrichment, Layer 3 tracking operational state throughout the lifecycle.

Layer 1: Customer Core

Layer 1 is the customer instruction, captured exactly as submitted, then sealed. No bank process writes to Layer 1 after intake. It holds all elements of customer intent: debtor and creditor identities (with their banks and accounts), amount, currency, pre-agreed exchange rate if applicable, value date, purpose, and remittance information. These are pain.001-aligned fields. When the pacs.008 is generated, Layer 1 values flow into it as PASS-THROUGH fields, unmodified.

Layer 2: Bank Enrichment

Layer 2 is empty at the end of Part 1. It holds pacs.008-aligned fields that the bank determines: UETR, settlement method, charge bearer, creditor agent BIC, intermediary agent BICs. None of these come from the customer. They are the output of enrichment, compliance, routing, and decisioning processes. Layer 2 fills in during Part 2. At this stage: empty.

Layer 3: Internal Metadata

Layer 3 is the payment engine’s operational state. Enrichment status flags. Compliance clearance status. Routing decision records. Batch metadata: batch_id, batch_sequence, batch_total. Processing timestamps. Retry counters. Error log entries.

One important distinction: Layer 3 is operational state, not the audit log. The audit log is a separate system, maintaining immutable records of every state transition for every payment, retained for regulatory compliance. Layer 3 and the audit log serve different purposes, are different systems, and should not be conflated in your architecture. Layer 3 is the engine’s working memory. The audit log is the permanent, tamper-proof record of what happened.

At the end of Part 1, Layer 3 contains one entry: the intake timestamp and validation status. Everything else is pending.

What fields are immutable and what can the bank change?

The clearest illustration of immutability is through charges, because charges are where many teams make their first mistake with InstructedAmount.

Claudia submits EUR 50,000. Her bank charges EUR 5 for processing. The beneficiary bank charges EUR 2.50. What happens to the EUR 50,000?

Nothing. The InstructedAmount does not change.

Charges are not deducted from the InstructedAmount. They are carried in separate charge fields governed by the charge bearer code (ChrgBr). The ChrgBr code determines who pays the charges. It does not modify the original instruction.

| ChrgBr | Debtor Debits | Creditor Receives | InstructedAmount |

| SLEV-SHAR / SHA | EUR 50,005.00 | EUR 49,997.50 | EUR 50,000 (UNCHANGED) |

| DEBT / OUR | EUR 50,007.50 | EUR 50,000.00 | EUR 50,000 (UNCHANGED) |

| CRED / BEN | EUR 50,000.00 | EUR 49,992.50 | EUR 50,000 (UNCHANGED) |

ChrgBr codes and their effect on debtor debit and creditor credit. InstructedAmount is EUR 50,000 in every scenario.

In every scenario, the InstructedAmount is EUR 50,000. What changes is the interbank settlement amount (IntrBkSttlmAmt), calculated separately. If any system modifies InstructedAmount to reflect charges, the audit trail is broken. It is always a bug. For a full explanation of how charge codes work in both MT and ISO 20022, the Understanding Charge Codes article covers OUR/DEBT, BEN/CRED, and SHA/SHAR with worked examples.

Immutable: customer controls

- Debtor account, legal entity name, and their bank

- Creditor name, account details, and their bank (as provided by the customer)

- Amount (InstructedAmount)

- Currency

- Pre-agreed exchange rate (if customer locked this before submission)

- Value date (ReqdExctnDt)

- Purpose code (when provided)

- Remittance reference (when provided)

- Urgency/priority flag (when provided)

This list covers the primary immutable elements. It is illustrative. In some payment types and jurisdictions, additional customer-provided fields may also be immutable. The principle: if the customer provided it as intent, the bank does not modify it.

Mutable: bank determines

- Creditor BIC, derived from IBAN or name-address lookup if not confirmed

- Routing path and intermediary banks

- Settlement type (INDA/INGA/CLRG/COVE), determined by the routing engine

- Charge bearer, which a scheme rule may override

- UETR, generated post-compliance

- Scheme applied

- Actual settlement date (IntrBkSttlmDt), derived from ReqdExctnDt plus calendar and cut-off rules

This list covers the primary mutable elements. The complete list of fields the bank determines varies by implementation, scheme, and jurisdiction.

What drives pacs.008 content from pain.001?

The same customer instruction can produce very different pacs.008 content depending on specific values in the pain.001. These are decision triggers, not field-to-field mappings. Field-level mapping lives in Part 4. The principle here: pain.001 values trigger decisions that determine what the pacs.008 will contain. The drivers below are the most significant, but they are not the complete list.

Driver 1: Payment Type Information (SvcLvl)

If the pain.001 carries SvcLvl/Cd = SEPA, the routing engine applies SEPA SCT rules: CLRG settlement, SHAR charge bearer, SEPA-reachable BIC for the creditor agent, 140-character remittance limit. No SEPA SvcLvl with a non-SEPA creditor means CBPR+ rules apply: INDA or INGA settlement, correspondent selection, different charge bearer logic. The same EUR 50,000 to the same Italian IBAN can produce a completely different pacs.008 depending entirely on SvcLvl. The Payment Type Information article explains this field and its downstream effects in full.

Driver 2: Currency combination (domestic vs cross-border determination)

The currency of the instructed amount relative to the debtor’s account currency and the creditor’s account currency is a significant routing driver. If the instructed currency, the debtor account currency, and the creditor account currency are all the same domestic currency, the payment is likely domestic and will follow domestic RTGS or clearing rules. If currencies differ, or if the creditor’s bank is in a different country, cross-border rules apply. Currency drives the initial routing decision tree and determines which scheme rulebook governs the pacs.008 content.

Driver 3: Creditor Account (IBAN present or absent)

IBAN present means the bank can extract the creditor agent BIC directly from the IBAN. Fast path. For Claudia’s payment, the IBAN IT60 X054 2811 1010 0000 0123 456 identifies the Italian bank. IBAN absent means name-and-address lookup. Slower, and it may require manual intervention. This path is more common in production than many teams expect, particularly for payments to new beneficiaries.

Driver 4: Regulatory Reporting (RgltryRptg)

If the pain.001 carries regulatory reporting data, it is preserved and passed through into the pacs.008. If regulatory data is absent but the destination jurisdiction requires it, the bank flags REGULATORY_DATA_REQUIRED. The payment may be challenged back to the customer before pacs.008 can be created.

These four drivers illustrate the most significant decision triggers. The full set includes many more: the scheme of the creditor bank, value date relative to cut-off, account type, customer relationship classification, correspondent agreement coverage, and jurisdiction-specific regulatory rules. The point is not to enumerate all possible drivers but to internalise that the pacs.008 content is the output of decisions, not a mechanical field-by-field copy of pain.001.

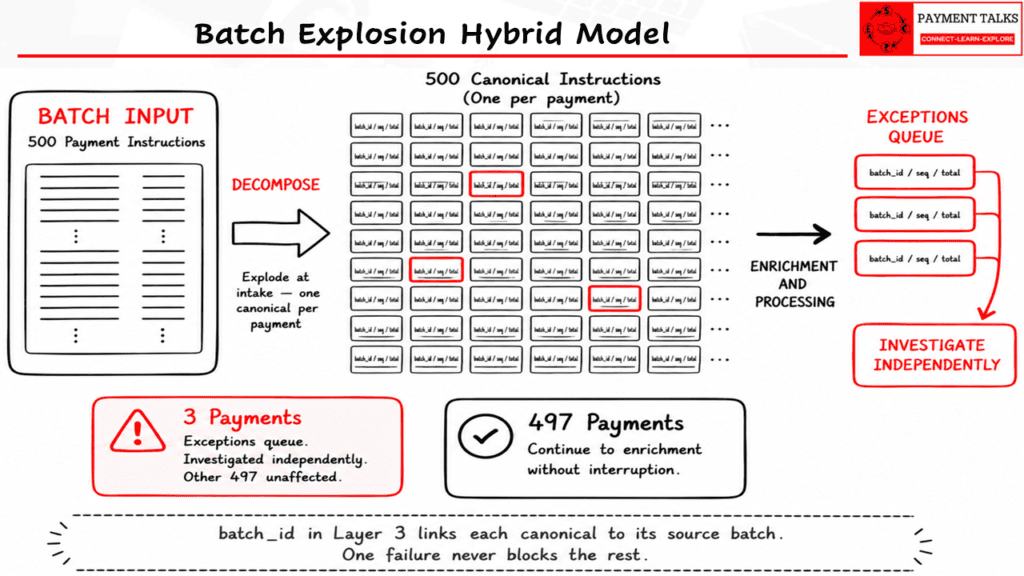

How should banks handle batch payments at initiation?

Claudia’s EUR 50,000 is a single payment. Banks also process payroll runs of 500 payments, bulk supplier batches, dividend distributions. The canonical instruction must handle both. Three approaches exist.

Approach 1: Immediate explosion

Receive the batch of 500. Decompose immediately into 500 individual canonical instructions. Each is independent, with its own lifecycle, compliance screening, routing decision, and processing state.

- Benefit: one failed payment never blocks the other 499. Parallel processing. Each payment progresses at its own pace.

- Risk: traceability back to the source batch requires careful metadata tagging, or it is lost.

Approach 2: Keep the batch as one unit

Receive 500 payments. Create one batch canonical instruction.

Do not use this in production. If one payment has an issue, all 500 are held. In payroll scenarios, 497 employees wait for their pay because 3 accounts have problems. The investigation might take hours. This is operationally unacceptable and in payroll scenarios a reputational risk for the bank.

Approach 3: Hybrid (the recommendation)

Explode into 500 individual canonical instructions. Tag each with batch metadata in Layer 3:

- batch_id: unique identifier for the source batch, e.g. SALARY-2026-05-MONTHLY

- batch_sequence: position within the batch, e.g. 47 of 500

- batch_total: 500

Each payment is processed independently. If 3 fail, those 3 go to the exceptions queue. The other 497 continue without interruption. The batch_id in Layer 3 links every one of the 500 canonical instructions back to the source batch for reporting and reconciliation. This recommendation comes from evaluating what actually breaks in production. The all-or-nothing approach fails visibly. The explode-without-tagging approach fails quietly: payments process but batch-level reporting is impossible without reconstructing relationships from external data.

Visual 4: The hybrid batch approach: individual payment autonomy with batch-level traceability preserved in Layer 3.

Where does the UETR come from at initiation?

The UETR (Unique End-to-End Transaction Reference) is a UUID4 value that tracks a payment across the entire correspondent chain. SWIFT’s gpi tracker uses it as its primary key. For a full breakdown of how payment identifiers work across the chain, that article covers the topic in detail.

Standard flow: bank-generated

The debtor bank generates the UETR. Specifically, the payment engine generates it AFTER compliance clearance and BEFORE pacs.008 creation. It is the last Layer 2 field to be populated before message generation. Assigning a UETR to a payment that is subsequently rejected creates an orphaned UETR in the gpi tracker, which raises regulatory audit questions. At the end of Part 1, Claudia’s payment has no UETR. That is correct.

Alternative: corporate-supplied

Sophisticated corporate treasury systems, SAP Treasury, Oracle Financials, Kyriba, FIS, can generate UETRs and include them in the pain.001. The bank then decides:

- Trust and use: record uetr_source = ‘corporate’. The corporate’s tracking system stays aligned with the gpi tracker.

- Discard and regenerate: record uetr_source = ‘bank’ AND original_corporate_uetr = [the corporate’s value]. Traceability is preserved even if the corporate UETR is not used.

Both paths are valid. Discarding a corporate UETR without recording the original value is not. If the corporate raises a query referencing their UETR, the bank must be able to link it to the internal payment record.

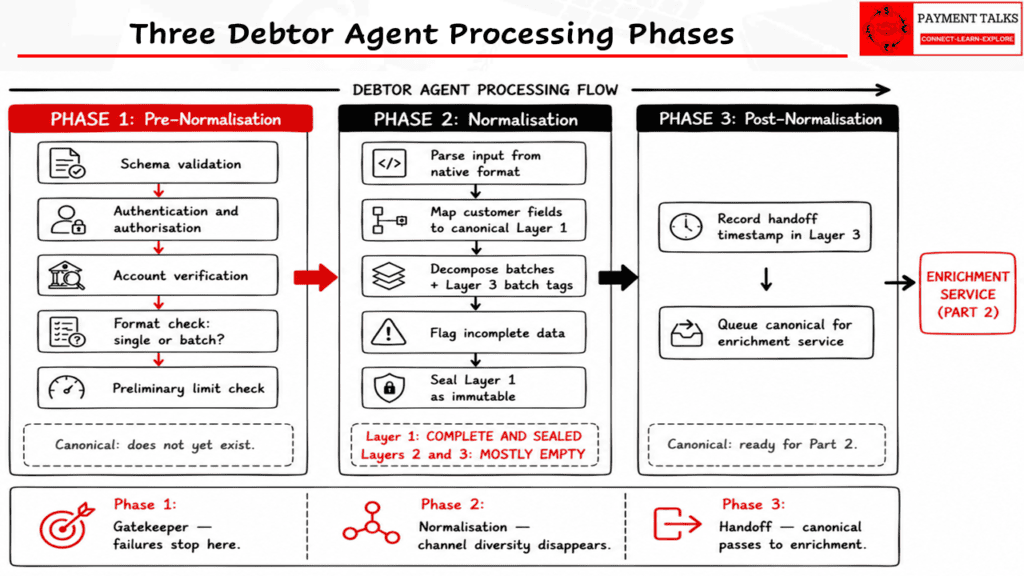

What are the three debtor agent processing phases?

From Claudia’s portal submission to a canonical instruction ready for enrichment, the debtor agent runs through three phases. These phases are the design specification for the intake layer of a payment engine.

Visual 5: Three debtor agent processing phases: from channel submission to enrichment-ready canonical instruction.

Phase 1: Pre-Normalisation (Intake and Validation)

The payment arrives in whatever format the channel delivers. Phase 1 tasks: schema validation, authentication and authorisation, account verification, basic format check (single or batch), and preliminary limit check. Phase 1 is the gatekeeper. Nothing that fails here enters the canonical system.

Phase 2: Normalisation (Canonical Instruction Creation)

Phase 2 is where channel diversity stops mattering. The portal JSON, the corporate XML, the Excel upload, and the teller form entry all emerge from Phase 2 as identical canonical instructions. Tasks: parse the input from its native format, map all customer fields to Layer 1, decompose batches into individual canonical instructions with batch metadata in Layer 3, flag incomplete data, and seal Layer 1 as immutable. At the end of Phase 2, Layer 1 is complete and sealed. Layers 2 and 3 are mostly empty.

Phase 3: Post-Normalisation (Handoff to Enrichment)

Phase 3 is the handoff. The canonical instruction is queued for the enrichment service. Phase 3 records the handoff timestamp in Layer 3, the validation status, and any flags the enrichment service needs: incomplete IBAN, missing regulatory data, corporate UETR pending decision. Phase 3 ends. Part 1 ends. The canonical is ready. That is Part 2.

What does NOT exist at the end of pacs.008 initiation?

This is worth stating explicitly. Teams that assume any of the following exist at intake build on incorrect foundations.

For Claudia’s EUR 50,000 payment, at the end of Part 1:

- UETR: does not exist. Will be assigned after compliance clearance in Part 2.

- Routing decision: does not exist. No correspondent selected. No route determined.

- Settlement type: does not exist. INDA, INGA, CLRG, COVE: the routing engine determines this in Part 2.

- Intermediary banks: not identified. The chain between Claudia’s bank and Acme’s bank is completely unknown.

- Charge bearer: not finalised. Customer preference may exist. Scheme rule may override. Not settled until enrichment.

- pacs.008: does not exist. Not one field populated.

What exists: a canonical instruction with Layer 1 complete and Layers 2 and 3 mostly empty. That is the correct state. That is what Part 2 picks up.

What are the five implementation mistakes teams make at initiation?

Mistake 1: Confusing format with structure

A BA says we process PAIN.001. A developer says we use an API. Neither can resolve the confusion because they are talking about different dimensions of the same system. When this distinction is never made explicit, teams build parsers hardcoded to a specific format. When a new format arrives, the parser fails. The validator throws errors. The canonical mapping breaks. A new channel that should take two weeks becomes a rebuild that takes two months.

Mistake 2: Enrichment touching immutable data

Enrichment logic modifies InstructedAmount to account for FX rates or rounding. If Claudia submitted EUR 50,000 and the system records EUR 49,997.50 as InstructedAmount after an FX adjustment, there is no longer a reliable record of the original instruction. Compliance, dispute resolution, and regulatory enquiries all depend on the customer instruction being preserved exactly.

⚠ InstructedAmount is immutable. Charges are separate fields. Pre-agreed exchange rates are customer intent. If your enrichment logic writes to InstructedAmount, that is a bug with no exceptions.

Mistake 3: All-or-nothing batch processing

One bad payment holds all the good ones. In payroll scenarios, this is a reputational risk as well as an operational one. The hybrid approach, explode plus batch_id tag, is not more complex to implement. The discipline pays for itself the first time an operations team processes 497 payments while investigating 3 exceptions, rather than holding 500 until the 3 are resolved.

Mistake 4: Sparse canonical design

The canonical is built to handle the current scheme only. When the next scheme is onboarded, the required fields are not in the canonical. Every downstream service needs simultaneous schema updates. The canonical should be a superset from day one. Even if most fields are empty at intake, they exist in the schema. Each new scheme populates them differently. The engine does not change.

Mistake 5: Generating pacs.008 too early

The pacs.008 is generated before all processing gates have cleared. Compliance has not confirmed. Routing is still in progress. The message is built and submitted. If compliance subsequently rejects the payment, the UETR is orphaned in the gpi tracker and the MsgId is wasted.

⚠ Generate pacs.008 only when all five conditions are simultaneously true: compliance cleared, limits passed, decision approved, routing confirmed with cut-off met, UETR assigned. Not before.

Frequently Asked Questions

Q: What triggers the creation of a pacs.008?

A pacs.008 is created only after all processing gates clear: compliance screening passed, transaction limits approved, routing confirmed, and UETR assigned. The trigger is not the customer’s payment submission. It is the completion of all enrichment and decisioning steps.

Q: Is there a fixed list of customer intent elements that every payment must have?

No. The elements of customer intent that must be captured vary by payment type, channel, scheme, and jurisdiction. Debtor identity, creditor identity, amount, and currency are present in every payment. Purpose, remittance information, urgency, and pre-agreed exchange rate are customer intent when provided but are not mandatory for every payment to process. The principle is fixed: whatever the customer provides as intent, the bank preserves unchanged.

Q: Why does a bank need a canonical instruction instead of mapping pain.001 directly to pacs.008?

Direct mapping works for a single scheme and a single input format. It becomes unmaintainable when multiple schemes and multiple channels are in play. The canonical instruction separates customer data from scheme-specific logic and normalises all input formats into one structure. Adding a new scheme means adding a new adapter. The engine does not change.

Q: What is the difference between format and structure in payment initiation?

Format is the transport layer: JSON, XML, CSV, SWIFT FIN, Excel. Structure is the semantic layer: the ISO 20022 pain.001 logical blocks and field organisation. A bank can receive pain.001 structure in JSON format, XML format, or CSV format. These are different technical implementations of the same logical structure. A BA saying we use PAIN.001 and a developer saying we use an API are both correct and both talking about different dimensions of the same system.

Q: What is the canonical instruction and why is it called the working horse of the payment engine?

The canonical instruction is the bank’s internal representation of a payment, serving as the single source of truth throughout the lifecycle. Every internal processing service reads from and writes to the canonical. No service processes the original input format. No service processes a half-built pacs.008. Adding a new input format means building one input adapter to the canonical. The core engine is untouched.

Q: When is the UETR assigned?

After compliance clearance and before pacs.008 creation. Assigning it earlier creates orphaned UETRs in the SWIFT gpi tracker when payments are subsequently rejected. The UETR must never be assigned at intake.

Q: What is the difference between Layer 3 of the canonical and the audit log?

Layer 3 is the payment engine’s operational state: enrichment flags, routing decisions, batch metadata, retry counts. It is updated throughout the payment lifecycle as the engine progresses through stages. The audit log is a separate system, maintaining immutable records of every state transition, retained for regulatory compliance. Layer 3 is working memory. The audit log is the permanent, tamper-proof record.

Q: How should banks process batch payments at initiation?

Explode into individual canonical instructions immediately, one per payment. Tag each with batch metadata in Layer 3 (batch_id, batch_sequence, batch_total). This allows independent processing of each payment while preserving traceability back to the source batch.

Q: What does not exist at the end of payment initiation?

UETR, routing decision, settlement type, intermediary banks, final charge bearer decision, and the pacs.008 message itself. Only the canonical instruction with Layer 1 complete exists at this stage.

Summary: what happens before the pacs.008 exists

By the time a pacs.008 exists, the hard work is already done. Part 1 is the story of that hard work.

Customer intent arrives through multiple channels in multiple formats. The bank captures it, normalises it into a canonical instruction, and seals the customer intent elements in Layer 1. Format and structure are separated at intake. Batches are exploded and tagged. The canonical becomes the working horse: every internal service reads from it and writes to it, and any new format addition requires only one adapter, not an engine change.

What does not exist at the end of Part 1: UETR, routing decision, settlement type, intermediary banks, final charge bearer, and the pacs.008 itself.

Part 2 picks up here. The canonical instruction is handed to the enrichment service. The five-stage creation pipeline begins: enrichment, decisioning, routing, UETR assignment, and pacs.008 generation. That is where the message is born.

Watch the full walkthrough on YouTube

Prefer video? Full walkthrough on the PaymentTalks YouTube channel. Link above.

This is Part 1 of the PaymentTalks pacs.008 Masterclass Series. Part 2 covers the five-stage creation pipeline: how the debtor agent transforms a canonical instruction into a pacs.008.